Meta Q3 earnings next on the agenda – Stock Markets

Meta to report strong earnings after market closes

Focus remains on AI & Metaverse outlook

Meta platforms, the parent company of Facebook and Instagram, will announce third-quarter earnings on Wednesday after the market closes. Forecasts point to notable growth, with the consensus recommendation from analysts polled by Refinitiv being a buy.

Total revenue is expected to show an annual growth of 21% to $33.5bln in the three months to September – double the 11% growth in the second quarter. The family of apps (Facebook, Messenger, Instagram, WhatsApp) has probably experienced a similar whopping expansion, with the advertising segment also rebounding by an equivalent solid percentage.

In other important financial metrics, earnings per share (EPS) are forecast to jump to $3.63 compared to $2.98 in the previous quarter and $1.64 in the same period a year ago. As regards its profitability, net income is expected to grow at the fastest pace in a couple of years – by more than 100%.

Having beat estimates over the past two quarters and with several institutional investors and hedge funds raising their Meta shareholdings and revising their target prices higher recently, the bar is set high for the social networking company.

Is Meta an attractive stock?The negative reaction to Tesla and Netflix as well as Alphabet's mixed results shows that investors are more sensitive to data misses this time, and is unable to repeat July's rally. Despite current uncertain market conditions and ongoing lawsuits, Meta platforms could still shine in the tech world and attract investors even if the stock price declines.

Engagement is a powerful tool for the giant social media company, making it hard for anyone to find any easy alternative to connect with friends and family and get updated on local and global news. It’s even more impressive to know that the planet has a population of nearly 7.9 billion and almost half of it is actively using its Facebook account on a monthly basis. That’s definitely a plus for developing its Metaverse world and incorporating its AI tools in everyone’s life at a faster pace than its peers.

The lack of alternative social media platforms could make charges difficult to avoid for those who don’t want to share their digital activity with the company. Note that Meta is planning to charge its European audience $14 monthly for ad-free Facebook and Instagram or $17 for both and on desktop. While this might cause some discomfort among members it could be a new source of revenue diversification for the company besides the monetization of Reels and advertising. On that front, it would be interesting to learn whether the company plans to expand its charges to other regions too.

Expenses could growOn the other hand, the ongoing transition to Metaverse and the expansion of AI will not come at a cheap cost as competition gets more intense. Meta aims to start training a new AI model, which will be a more advanced version than its open-source AI language model Llama 2 and be a serious competitor to chatGPT, as soon as in early 2024. Other exciting AI projects are also in the pipeline, including chatbots based on celebrities and features connected to Ray-ban glasses, while improvements on the virtual reality front are also on the way following the release of the new Quest 3 headset.

During its previous earnings release, Zuckerberg’s group of companies said that total expenses could increase to $88-91 billion by the end of 2023 and further grow in 2024 providing no specific number for the latter. Any guidance of expenses growing below $100bln or at least below revenue growth could be market positive amid elevated interest rates and wages and heightened geopolitical risks.

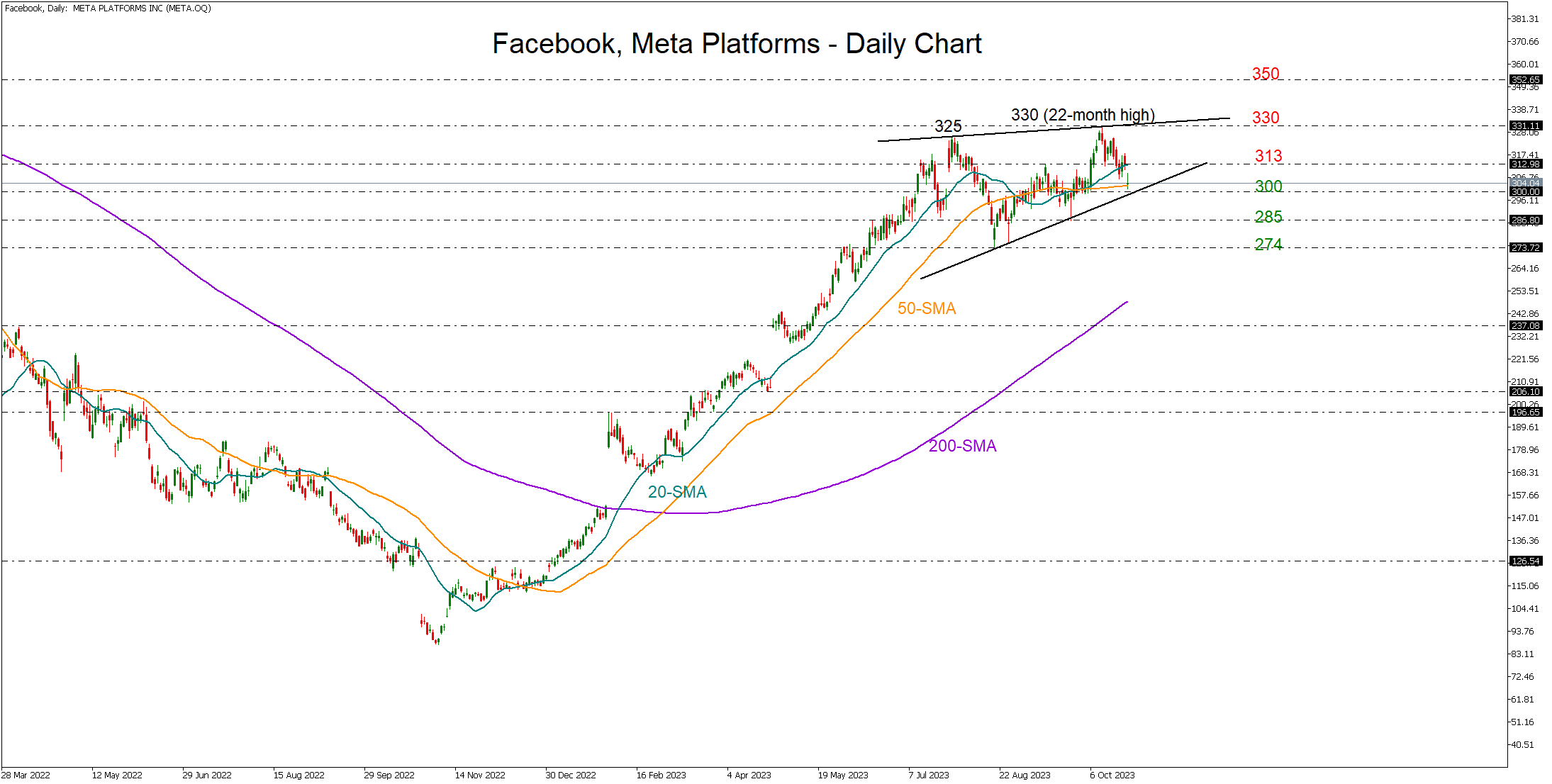

Levels to watchTurning to stock markets, Meta’s stock has been the second-best performer after NVIDIA in the S&P 500 space during 2023, trading 159% higher year-to-date compared to the index’s gain of 10%. Stronger-than-expected advertising revenues and a brighter outlook for the final quarter of 2023 could be good news for the stock as recession fears and geopolitical risks weigh on sentiment. Should the price bounce back above the 20-day simple moving average (SMA) at 312, the door would open again for the 2023 peak of 330. The 2021 resistance of 350 could be the next obstacle.

Alternatively, a miss in earnings and signals of more challenging years ahead could squeeze the stock below the 50-day SMA and the 300 level, shifting the attention to the 285 constraining zone and then to the August trough of 274.

免責聲明: XM Group提供線上交易平台的登入和執行服務,允許個人查看和/或使用網站所提供的內容,但不進行任何更改或擴展其服務和訪問權限,並受以下條款與條例約束:(i)條款與條例;(ii)風險提示;(iii)完全免責聲明。網站內部所提供的所有資訊,僅限於一般資訊用途。請注意,我們所有的線上交易平台內容並不構成,也不被視為進入金融市場交易的邀約或邀請 。金融市場交易會對您的投資帶來重大風險。

所有缐上交易平台所發佈的資料,僅適用於教育/資訊類用途,不包含也不應被視爲適用於金融、投資稅或交易相關諮詢和建議,或是交易價格紀錄,或是任何金融商品或非應邀途徑的金融相關優惠的交易邀約或邀請。

本網站的所有XM和第三方所提供的内容,包括意見、新聞、研究、分析、價格其他資訊和第三方網站鏈接,皆爲‘按原狀’,並作爲一般市場評論所提供,而非投資建議。請理解和接受,所有被歸類為投資研究範圍的相關内容,並非爲了促進投資研究獨立性,而根據法律要求所編寫,而是被視爲符合營銷傳播相關法律與法規所編寫的内容。請確保您已詳讀並完全理解我們的非獨立投資研究提示和風險提示資訊,相關詳情請點擊 這裡查看。