Artificial Intelligence: Is the ‘baby bubble’ ready to pop?

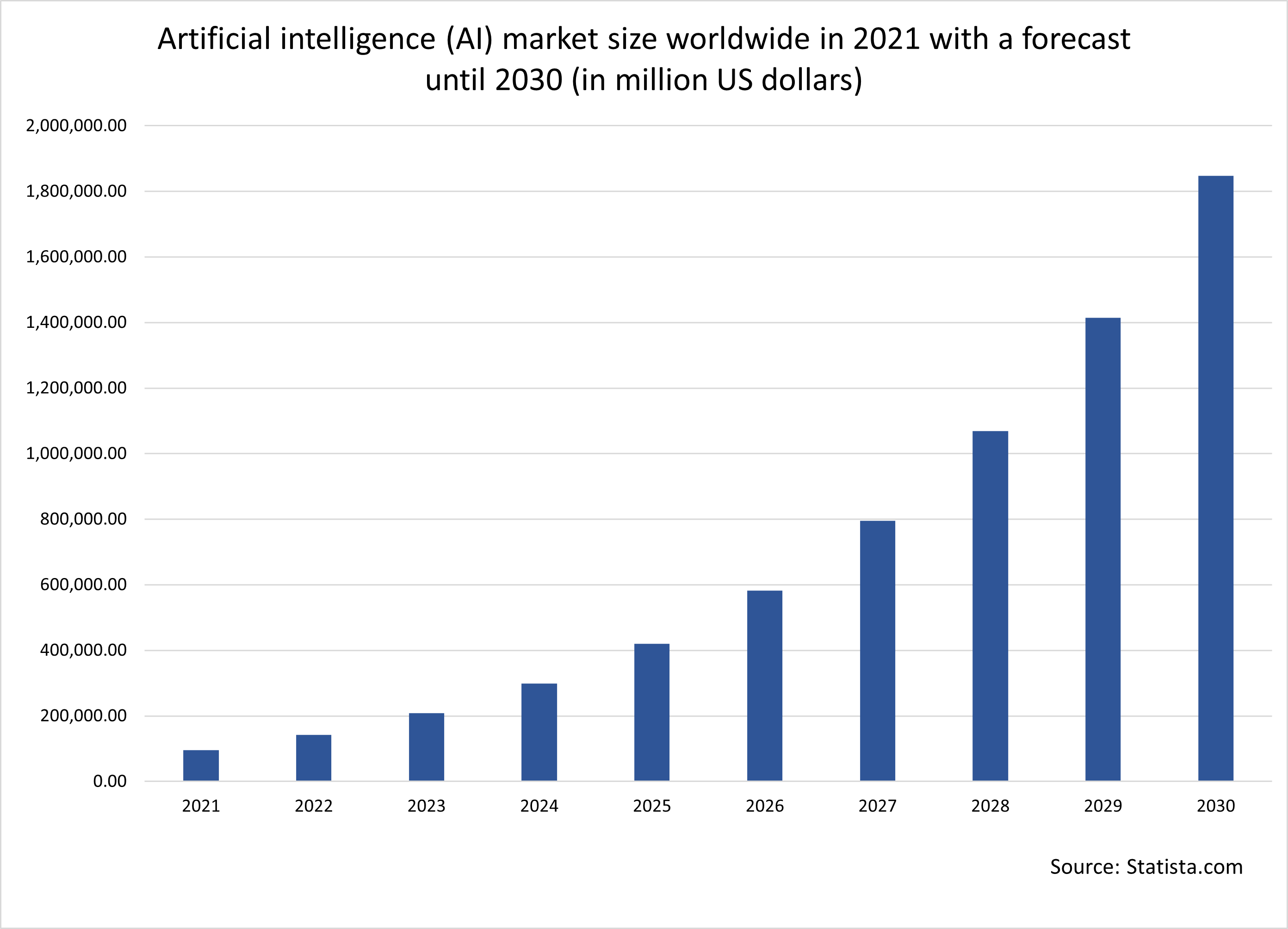

According to Statista, the AI market is expected to experience massive growth in the coming years, with its value of $100bn dollars in 2021 seen growing twentyfold by 2030, to around two trillion dollars. And what may have prompted many participants to jump into the AI bandwagon may have been the release of ChatGPT 3.0 in 2022, which opened the pandora box regarding the possibilities of generative AI.

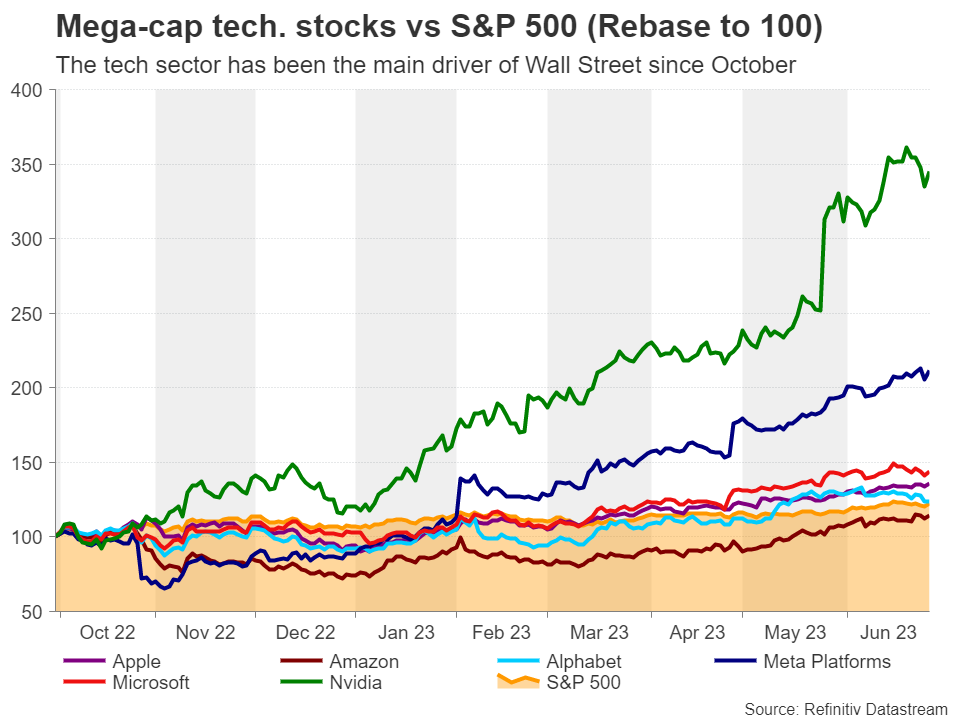

One way to bet on AI may be through chipmakers, as AI requires massive computer power and strong computing power means powerful microchips. The fact that Nvidia’s stock has surged more than 300% since its October lows is not an accident as this firm’s chips are the brains behind most of the AI chatbots we know, while the firm holds around 95% of the market share of machine learning chips. Other chipmakers, like AMD (Advanced Micro Devices) and Intel, also enjoyed massive gains, with the former surging by more than 100% since October and the latter around 50%.

But valuations suggest they are very expensiveSo, the bubble question is popping up on everyone’s mind and rightfully so. Looking at valuations, Nvidia is trading around 45 times the estimated earnings for next year, while just two weeks ago, that forward price-to-earnings (PE) ratio was almost at 60x. That’s well above the forward PE ratio of the S&P 500, which is at around 19x. So, the AI market can be considered overvalued and such numbers may discourage new investors from joining the action. Maybe that’s why there was a pullback in the stock market recently.

Geopolitics also constitute a risk

Geopolitics also constitute a riskOne other risk to the AI euphoria is geopolitics. For the construction of their chips, most chipmakers are reliant on one company in Taiwan, called TSMC (Taiwan Semiconductor Manufacturing Company). Thus, with China not recognizing Taiwan as a sovereign state, any tensions between the two countries could well affect the semiconductor market and thereby weigh on the AI bull market. Yes, due to those geopolitical risks, TSMC is trying to expand and diversify its business in other countries, including the US, but that’s not a plan that can be completed overnight.

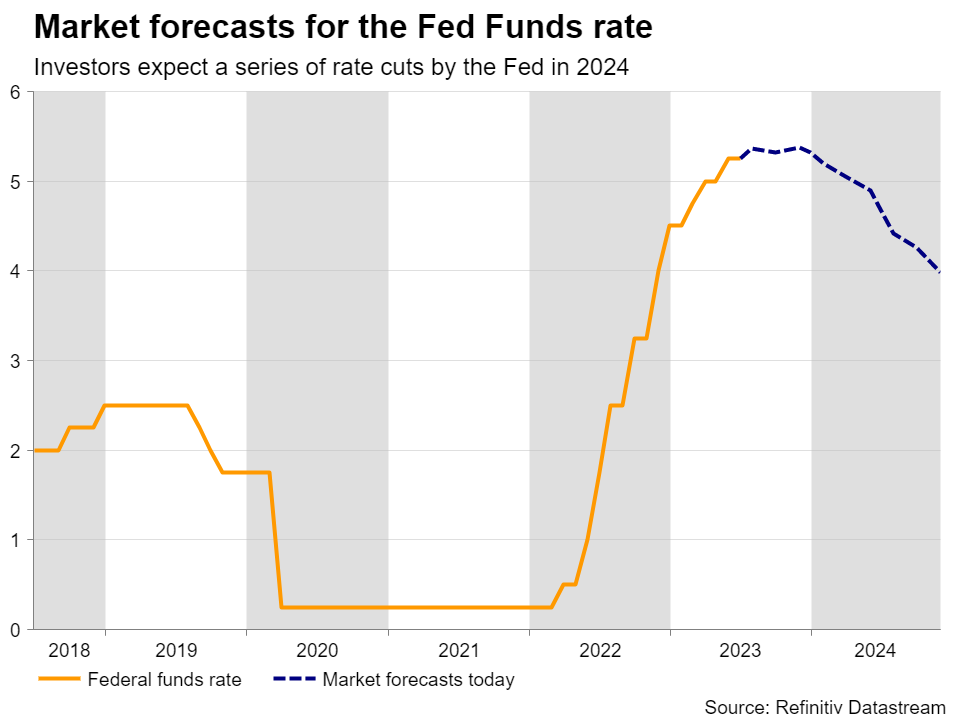

Expectations of growth and Fed cuts may keep losses limitedHaving said that though, even if there is a further pullback in the stock market, it could still be considered as a corrective phase rather than the beginning of a full-scale bear market. After all, most high-growth tech firms are valued by discounting expected cash flows for the quarters and years ahead. So, with Nvidia’s and other chipmakers’ cash-flow-per-share expected to continue accelerating in the foreseeable future, and also bearing in mind market expectations of several rate cuts by the Fed next year, present values have the potential to continue rising.

Even if geopolitical tensions rise and leave their mark, a potential episode of market risk-aversion could prompt AI investors to increase their exposure to mega-cap, more established, tech stocks, like Alphabet, Amazon, Apple, Meta, and Microsoft, which are also expanding their business in the AI field. Along with Nvidia, these giants are responsible for most of the gains in the S&P 500 since October.

For investors to start fleeing out of the stock market, not only does the Fed have to convince them that there are no rate cuts on the table for next year, but growth estimates for big tech firms in the upcoming earnings seasons may need to start disappointing. The Fed has already signaled that two more quarter-point hikes are on the table before it ends this tightening crusade and Fed Chair Powell said that rate reductions are ‘a couple of years out’. And yet, the market is penciling in only around 35bps worth of additional hikes, and several reductions in 2024. So, until the Fed or the data convince them to scale back those cut bets, investors may see the current retreat, or any near-term extensions of it, as an opportunity to buy at more attractive levels.

For investors to start fleeing out of the stock market, not only does the Fed have to convince them that there are no rate cuts on the table for next year, but growth estimates for big tech firms in the upcoming earnings seasons may need to start disappointing. The Fed has already signaled that two more quarter-point hikes are on the table before it ends this tightening crusade and Fed Chair Powell said that rate reductions are ‘a couple of years out’. And yet, the market is penciling in only around 35bps worth of additional hikes, and several reductions in 2024. So, until the Fed or the data convince them to scale back those cut bets, investors may see the current retreat, or any near-term extensions of it, as an opportunity to buy at more attractive levels.免責聲明: XM Group提供線上交易平台的登入和執行服務,允許個人查看和/或使用網站所提供的內容,但不進行任何更改或擴展其服務和訪問權限,並受以下條款與條例約束:(i)條款與條例;(ii)風險提示;(iii)完全免責聲明。網站內部所提供的所有資訊,僅限於一般資訊用途。請注意,我們所有的線上交易平台內容並不構成,也不被視為進入金融市場交易的邀約或邀請 。金融市場交易會對您的投資帶來重大風險。

所有缐上交易平台所發佈的資料,僅適用於教育/資訊類用途,不包含也不應被視爲適用於金融、投資稅或交易相關諮詢和建議,或是交易價格紀錄,或是任何金融商品或非應邀途徑的金融相關優惠的交易邀約或邀請。

本網站的所有XM和第三方所提供的内容,包括意見、新聞、研究、分析、價格其他資訊和第三方網站鏈接,皆爲‘按原狀’,並作爲一般市場評論所提供,而非投資建議。請理解和接受,所有被歸類為投資研究範圍的相關内容,並非爲了促進投資研究獨立性,而根據法律要求所編寫,而是被視爲符合營銷傳播相關法律與法規所編寫的内容。請確保您已詳讀並完全理解我們的非獨立投資研究提示和風險提示資訊,相關詳情請點擊 這裡查看。