Daily Comment – Fed delivers rate cut, stocks rally but dollar not impressed

- Fed cuts rates and keeps door open to a December move

- Powell appears confident about the inflation outlook

- Equities’ euphoria continues, strongest weekly rally of 2024

- Yen manages to gain against the US dollar

The Fed announces a rate cut

With the markets still digesting Trump’s win, the Fed announced the much-anticipated rate cut. Unswayed by concerns that Trump’s second term might lead to extreme protectionism and thus keep inflation high, the FOMC cut rates by 25bps, with Chairman Powell appearing content with the inflation outlook, despite the positive talk about growth.

The FOMC cut rates by 25bps, with Chairman Powell appearing content with the inflation outlook

The more hawkish statement, due to the removal of the phrase that “the Committee has gained greater confidence that inflation is moving sustainably toward 2%”, was successfully countered by the dovish press conference. Powell’s comment that “the baseline for next year is to gradually move rates towards the neutral rates” means that more cuts are on the agenda, and that the December meeting, with its updated dot plot, is likely to be a live one.

The market is convinced that another 25bps rate cut will be announced on December 19, as it is currently assigning a 92% probability to this outcome. Despite the strength of the US economy potentially hindering back-to-back rate cuts, some investment houses highlight that the Fed’s window of opportunity for further rate cuts might be shrinking fast, as Trump will officially take over on January 20.

The 10-year Treasury yield reacted favourably to Powell’s message, edging lower toward the 4.3% level. However, it remains elevated, around 60bps above the level recorded just ahead of the September Fed gathering that delivered the first rate cut. The current level of yields is offsetting the accommodation provided by the Fed, and thus keeping funding costs high for firms.

US stocks' post-election euphoria continues

Meanwhile, US stock indices, which benefited greatly from Trump’s return to the White House, got another boost yesterday, with the S&P 500 index climbing above the 6,000 level and recording a new all-time high. This is shaping up to be the best week for the world’s largest stock index since November 2023, when the market first realized that the rate hiking cycle concluded. Smaller capitalization stocks remain in demand, with the Russell 2000 index outperforming the other major US stock indices.

US stock indices got another boost yesterday, with the S&P 500 index climbing above the 6,000 level

Dollar remains strong, yen gets a tiny boost

The dollar was probably the least affected by the Fed’s rate cut. It gained slightly versus both the euro and the pound but weakened against the yen. The small downleg in dollar/yen is probably the result of the continued verbal intervention from Japanese officials, who have been alarmed by the recent pace of the yen’s underperformance.

The small downleg in dollar/yen is probably the result of the continued verbal intervention from Japanese officials

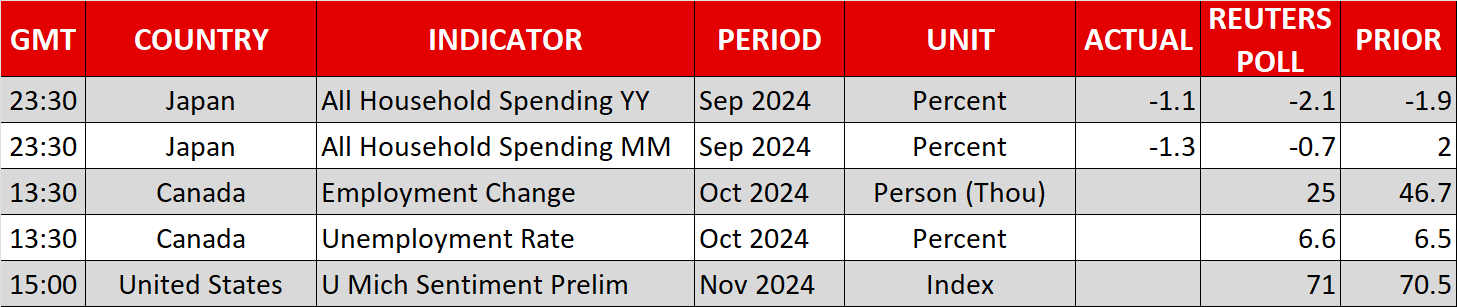

In addition, expectations for a December BoJ rate hike are high, with the market currently fully pricing in a 10bps rate move, despite the ongoing political uncertainty following the recent Japanese snap election. Moreover, recent data prints have been modestly positive, apart from the consumer side of the economy. The September retail sales figure was weak, with this negative sentiment also depicted in the October consumer confidence index.

Relaterade tillgångar

Senaste nytt

Ansvarsfriskrivning: XM Group-enheter tillhandahåller sin tjänst enbart för exekvering och tillgången till vår onlinehandelsplattform, som innebär att en person kan se och/eller använda tillgängligt innehåll på eller via webbplatsen, påverkar eller utökar inte detta, vilket inte heller varit avsikten. Denna tillgång och användning omfattas alltid av i) villkor, ii) riskvarningar och iii) fullständig ansvarsfriskrivning. Detta innehåll tillhandahålls därför uteslutande som allmän information. Var framför allt medveten om att innehållet på vår onlinehandelsplattform varken utgör en uppmaning eller ett erbjudande om att ingå några transaktioner på de finansiella marknaderna. Handel på alla finansiella marknader involverar en betydande risk för ditt kapital.

Allt material som publiceras på denna sida är enbart avsett för utbildnings- eller informationssyften och innehåller inte – och ska inte heller anses innehålla – rådgivning och rekommendationer om finansiella frågor, investeringsskatt eller handel, dokumentation av våra handelskurser eller ett erbjudande om, eller en uppmaning till, en transaktion i finansiella instrument eller oönskade finansiella erbjudanden som är riktade till dig.

Tredjepartsinnehåll, liksom innehåll framtaget av XM såsom synpunkter, nyheter, forskningsrön, analyser, kurser, andra uppgifter eller länkar till tredjepartssajter som återfinns på denna webbplats, tillhandahålls i befintligt skick, som allmän marknadskommentar, och utgör ingen investeringsrådgivning. I den mån som något innehåll tolkas som investeringsforskning måste det noteras och accepteras att innehållet varken har varit avsett som oberoende investeringsforskning eller har utarbetats i enlighet med de rättsliga kraven för att främja ett sådant syfte, och därför är att betrakta som marknadskommunikation enligt tillämpliga lagar och föreskrifter. Se till så att du har läst och förstått vårt meddelande om icke-oberoende investeringsforskning och riskvarning om ovannämnda information, som finns här.