Daily Market Comment – US inflation report awaited for direction as stocks, dollar drift

- Nerves kick in as debt ceiling talks drag on, uncertainty builds ahead of US CPI

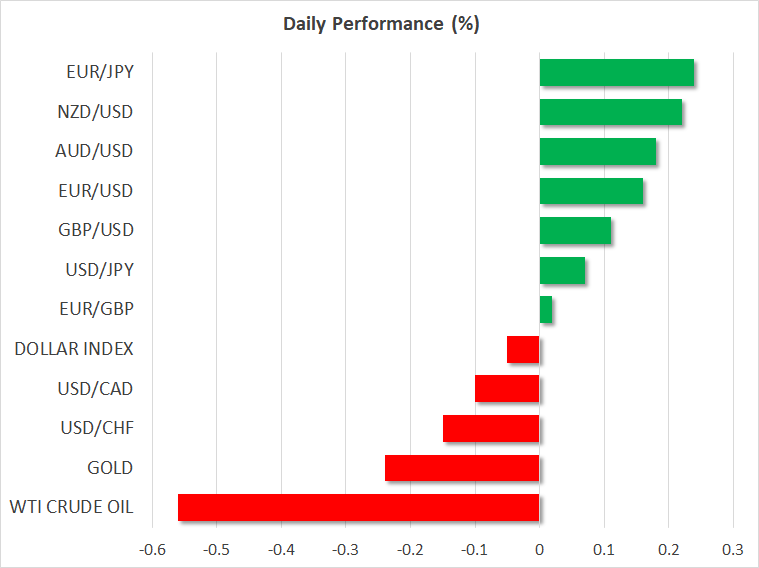

- Dollar pares some gains, euro bounces off lows but lacks momentum

- Wall Street slides as bank stocks remain under pressure, default risks rise

Caution sets in before inflation data

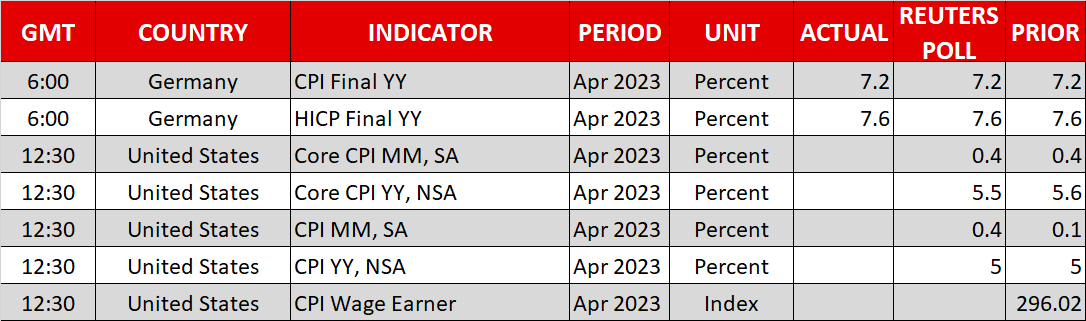

Caution sets in before inflation dataMarkets continued to struggle for direction on Wednesday amid some anxiety ahead of the April inflation report out of the United States later in the day and an ongoing stalemate in Congress over raising the debt ceiling. With the Fed clearly signalling that it remains in data-dependent mode, a pause in June hangs in the balance and today’s CPI figures could be what tips the odds in either direction.

The consumer price index is expected to have risen by 5.0% over the year to April, which would signal a stall in the progress to bring inflation down following an uninterrupted decline from the peak of 9.1% in June 2022. However, there may be some good news from the core CPI front, as it is projected to have dipped slightly to 5.5%.

If the latest PMI surveys and the Cleveland Fed’s Nowcast inflation tracker are to be believed, the risks are tilted towards an upside surprise.

After Friday’s robust NFP numbers, a hot CPI reading would cast further doubt on market bets that the Fed will begin cutting rates in the second half of the year. It is those bets that have been propping up shares on Wall Street during what has been an uninspiring earnings season, while the US dollar has been hammered against currencies like the euro and pound due to the divergence in the monetary policies.

Debt ceiling drama rumbles onAnother source of concern lately is the growing risk of a US debt default as Democrats and Republicans remain far apart on reaching a deal to raise the debt ceiling. The White House is trying to up the pressure by warning that the government could run out of cash as early as June 1, but Republicans are not giving any ground in the negotiations.

House speaker and Republican majority leader Kevin McCarthy told reporters he “didn’t see any new movement” after his meeting with President Biden yesterday. But Congressional leaders are due to meet again on Friday and this is providing some relief for traders.

Disney earnings eyed amid banking gloomUS stock futures started Wednesday in the red, extending yesterday’s losses. Bank stocks staged a modest but unconvincing rebound on Tuesday after coming under renewed pressure on Monday. The Fed’s latest loan officer survey did not point to anything too alarming in credit conditions in the aftermath of the banking turmoil and profitability in the sector hit an all-time high in the first quarter.

Nevertheless, confidence in smaller regional banks remains very low amid worries that there are more failures to come.

Disappointing earnings forecasts from PayPal and Skyworks also weighed on the broader market on Tuesday, while Disney will come under the spotlight today when it announces its results.

Dollar flat as euro lags and sterling climbs ahead of BoEIn currencies, the US dollar was more or less flat against a basket of currencies, with the euro slipping marginally and the pound crawling higher.

The euro has been underperforming over the past week following a batch of poor data out of the Eurozone’s powerhouse, Germany. The sudden deterioration of the German economy has prompted investors to scale back their rate hike expectations for the European Central Bank even though policymakers have not toned down their hawkish rhetoric.

The pound, meanwhile, has been benefiting from better-than-expected economic indicators as well as bets that the Bank of England will raise rates several more times this year, of which the next is anticipated to be announced tomorrow.

Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.