Daily Comment – US dollar and stock rally continues

- Euphoria in US assets, stock indices reach new highs

- Today's Fed speakers could threaten Monday’s gains

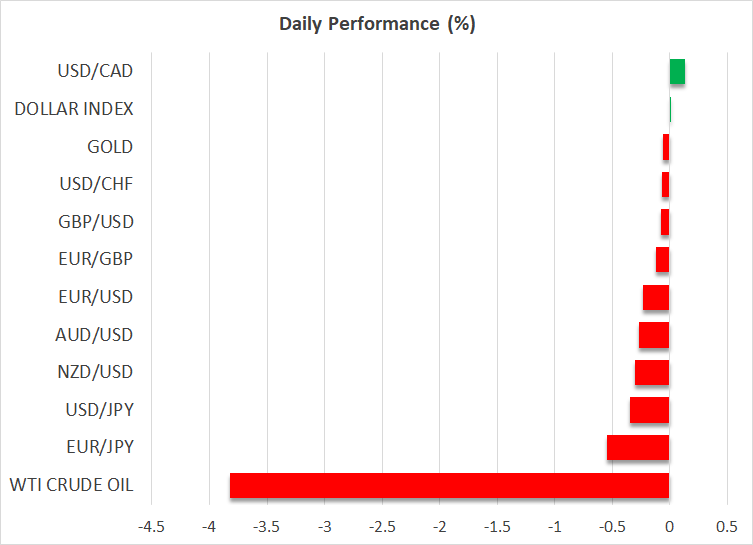

- Oil and gold in the red, bitcoin enjoys a strong boost

- Pound ignores jobs data, awaits Wednesday’s CPI

US stocks and dollar in the green

Both the US dollar and main US equity indices enjoyed another strong session yesterday. Euro/dollar traded at a 45-day low, and both the S&P 500 and the Dow Jones indices recorded new all-time highs despite the Columbus Day bank holiday keeping both the bond market closed and trading volumes below their recent averages. The release of third quarter earnings is already underway, with some big banking names on the list today and Netflix scheduled for Thursday, but the positive figures up to now do not justify the aggressive risk-on reaction.

In the meantime, the daily barrage of attacks between Israel and Iran’s proxies continues despite efforts from the US administration for a ceasefire, which could also boost Harris’ poll ratings. There were some comments from Israeli officials that Iran's nuclear and oil installations won't be targeted, but this doctrine could be quickly abandoned if Israeli losses continue to mount.

Therefore, one of the catalysts for both the dollar’s and stocks’ performance could be the latest Fedspeak. In remarks yesterday, Fed members Kashkari and Waller remained dovish even though the strong jobs market is probably forcing them to take a more relaxed approach regarding the November meeting. Interestingly, Fed board member Waller was quite frank in stating that if inflation unexpectedly rises, the Fed could pause the rate cuts.

Therefore, one of the catalysts for both the dollar’s and stocks’ performance could be the latest Fedspeak

The next CPI report will be published one week after the November 7 Fed meeting, but before that there will be an array of releases that could reveal the current inflation trend. Considering that the Fed expects a pickup in inflation in Q4, the November rate cut might appear more secure, at this stage, than the December one.

Fed members Daly, Kugler and Bostic will be on the wires today. Last week, San Francisco Fed President Daly opened the door to the possibility of no rate cut in November by stating that one or two cuts this year are likely, with Atlanta’s Bostic receiving the assist and openly talking about a November pause. A repeat of these comments from both members won’t shock the market, but it could potentially dent yesterday’s positive sentiment.

Gold and oil drop, bitcoin trying to maintain Monday’s gains

Amidst these developments, gold and oil have retreated somewhat, partly on the back of the dollar's renewed strength. Gold remains a tad below its recent all-time high while oil appears to be giving back a good chunk of its recent sizeable gains. China is partly responsible for the latter as the new support measures are again deemed as insufficient to restart the Chinese economy.

On the flip side, bitcoin rallied aggressively on Monday and tested the late September highs. It is surrendering part of its gains today, but the sentiment in the crypto space has probably changed, despite Minneapolis Fed President Kashkari repeating his aversion for bitcoin. Interestingly, presidential candidate Harris tried yesterday to appease crypto investors by announcing a ‘regulatory framework'. Harris’ plan was light on the details, but since former president Trump is an avid crypto supporter, cryptocurrencies could eventually enjoy a boost regardless of the November 5 winner.

Harris’ plan was light on the details, but since former president Trump is an avid crypto supporter, cryptocurrencies could eventually enjoy a boost regardless of the November 5 winner.

Mixed UK data, pound not impressed

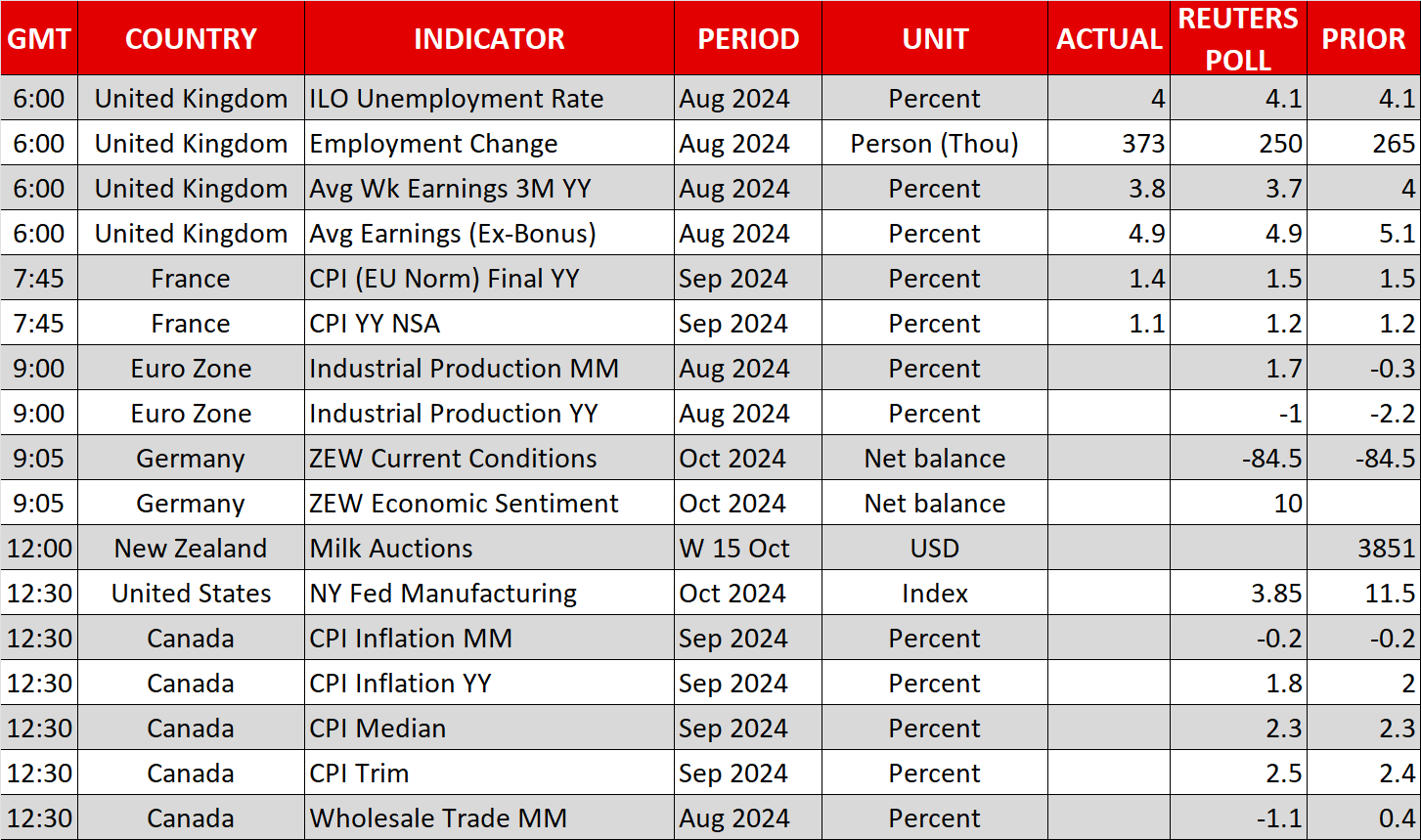

The latest UK labour market data has failed to please the pound as the unemployment rate ticked lower, but the claimant count printed above expectations and the average earnings figures edged a tad lower. Tomorrow’s CPI report remains the decisive release for the November rate cut, which is overwhelmingly priced in by the market.

Ativos relacionados

Últimas notícias

Isenção de Responsabilidade: As entidades do XM Group proporcionam serviço de apenas-execução e acesso à nossa plataforma online de negociação, permitindo a visualização e/ou uso do conteúdo disponível no website ou através deste, o que não se destina a alterar ou a expandir o supracitado. Tal acesso e uso estão sempre sujeitos a: (i) Termos e Condições; (ii) Avisos de Risco; e (iii) Termos de Responsabilidade. Este, é desta forma, fornecido como informação generalizada. Particularmente, por favor esteja ciente que os conteúdos da nossa plataforma online de negociação não constituem solicitação ou oferta para iniciar qualquer transação nos mercados financeiros. Negociar em qualquer mercado financeiro envolve um nível de risco significativo de perda do capital.

Todo o material publicado na nossa plataforma de negociação online tem apenas objetivos educacionais/informativos e não contém — e não deve ser considerado conter — conselhos e recomendações financeiras, de negociação ou fiscalidade de investimentos, registo de preços de negociação, oferta e solicitação de transação em qualquer instrumento financeiro ou promoção financeira não solicitada direcionadas a si.

Qual conteúdo obtido por uma terceira parte, assim como o conteúdo preparado pela XM, tais como, opiniões, pesquisa, análises, preços, outra informação ou links para websites de terceiras partes contidos neste website são prestados "no estado em que se encontram", como um comentário de mercado generalizado e não constitui conselho de investimento. Na medida em que qualquer conteúdo é construído como pesquisa de investimento, deve considerar e aceitar que este não tem como objetivo e nem foi preparado de acordo com os requisitos legais concebidos para promover a independência da pesquisa de investimento, desta forma, deve ser considerado material de marketing sob as leis e regulações relevantes. Por favor, certifique-se que leu e compreendeu a nossa Notificação sobre Pesquisa de Investimento não-independente e o Aviso de Risco, relativos à informação supracitada, os quais podem ser acedidos aqui.