Daily Comment – US dollar and stock rally continues

- Euphoria in US assets, stock indices reach new highs

- Today's Fed speakers could threaten Monday’s gains

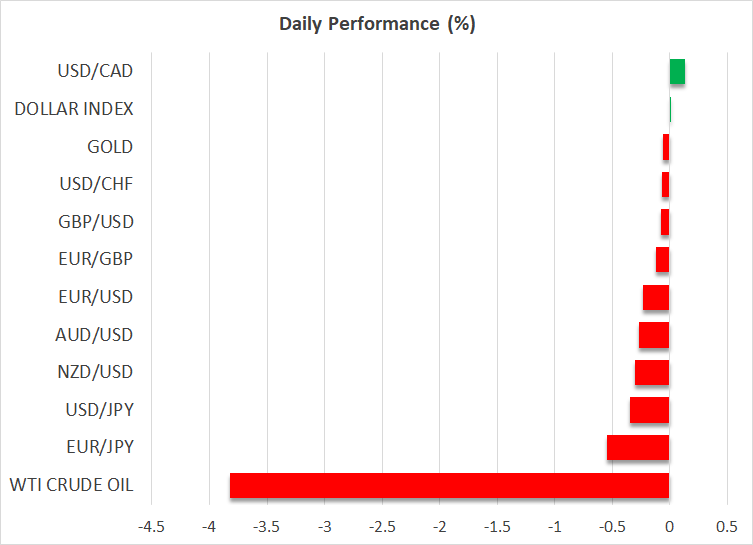

- Oil and gold in the red, bitcoin enjoys a strong boost

- Pound ignores jobs data, awaits Wednesday’s CPI

US stocks and dollar in the green

Both the US dollar and main US equity indices enjoyed another strong session yesterday. Euro/dollar traded at a 45-day low, and both the S&P 500 and the Dow Jones indices recorded new all-time highs despite the Columbus Day bank holiday keeping both the bond market closed and trading volumes below their recent averages. The release of third quarter earnings is already underway, with some big banking names on the list today and Netflix scheduled for Thursday, but the positive figures up to now do not justify the aggressive risk-on reaction.

In the meantime, the daily barrage of attacks between Israel and Iran’s proxies continues despite efforts from the US administration for a ceasefire, which could also boost Harris’ poll ratings. There were some comments from Israeli officials that Iran's nuclear and oil installations won't be targeted, but this doctrine could be quickly abandoned if Israeli losses continue to mount.

Therefore, one of the catalysts for both the dollar’s and stocks’ performance could be the latest Fedspeak. In remarks yesterday, Fed members Kashkari and Waller remained dovish even though the strong jobs market is probably forcing them to take a more relaxed approach regarding the November meeting. Interestingly, Fed board member Waller was quite frank in stating that if inflation unexpectedly rises, the Fed could pause the rate cuts.

Therefore, one of the catalysts for both the dollar’s and stocks’ performance could be the latest Fedspeak

The next CPI report will be published one week after the November 7 Fed meeting, but before that there will be an array of releases that could reveal the current inflation trend. Considering that the Fed expects a pickup in inflation in Q4, the November rate cut might appear more secure, at this stage, than the December one.

Fed members Daly, Kugler and Bostic will be on the wires today. Last week, San Francisco Fed President Daly opened the door to the possibility of no rate cut in November by stating that one or two cuts this year are likely, with Atlanta’s Bostic receiving the assist and openly talking about a November pause. A repeat of these comments from both members won’t shock the market, but it could potentially dent yesterday’s positive sentiment.

Gold and oil drop, bitcoin trying to maintain Monday’s gains

Amidst these developments, gold and oil have retreated somewhat, partly on the back of the dollar's renewed strength. Gold remains a tad below its recent all-time high while oil appears to be giving back a good chunk of its recent sizeable gains. China is partly responsible for the latter as the new support measures are again deemed as insufficient to restart the Chinese economy.

On the flip side, bitcoin rallied aggressively on Monday and tested the late September highs. It is surrendering part of its gains today, but the sentiment in the crypto space has probably changed, despite Minneapolis Fed President Kashkari repeating his aversion for bitcoin. Interestingly, presidential candidate Harris tried yesterday to appease crypto investors by announcing a ‘regulatory framework'. Harris’ plan was light on the details, but since former president Trump is an avid crypto supporter, cryptocurrencies could eventually enjoy a boost regardless of the November 5 winner.

Harris’ plan was light on the details, but since former president Trump is an avid crypto supporter, cryptocurrencies could eventually enjoy a boost regardless of the November 5 winner.

Mixed UK data, pound not impressed

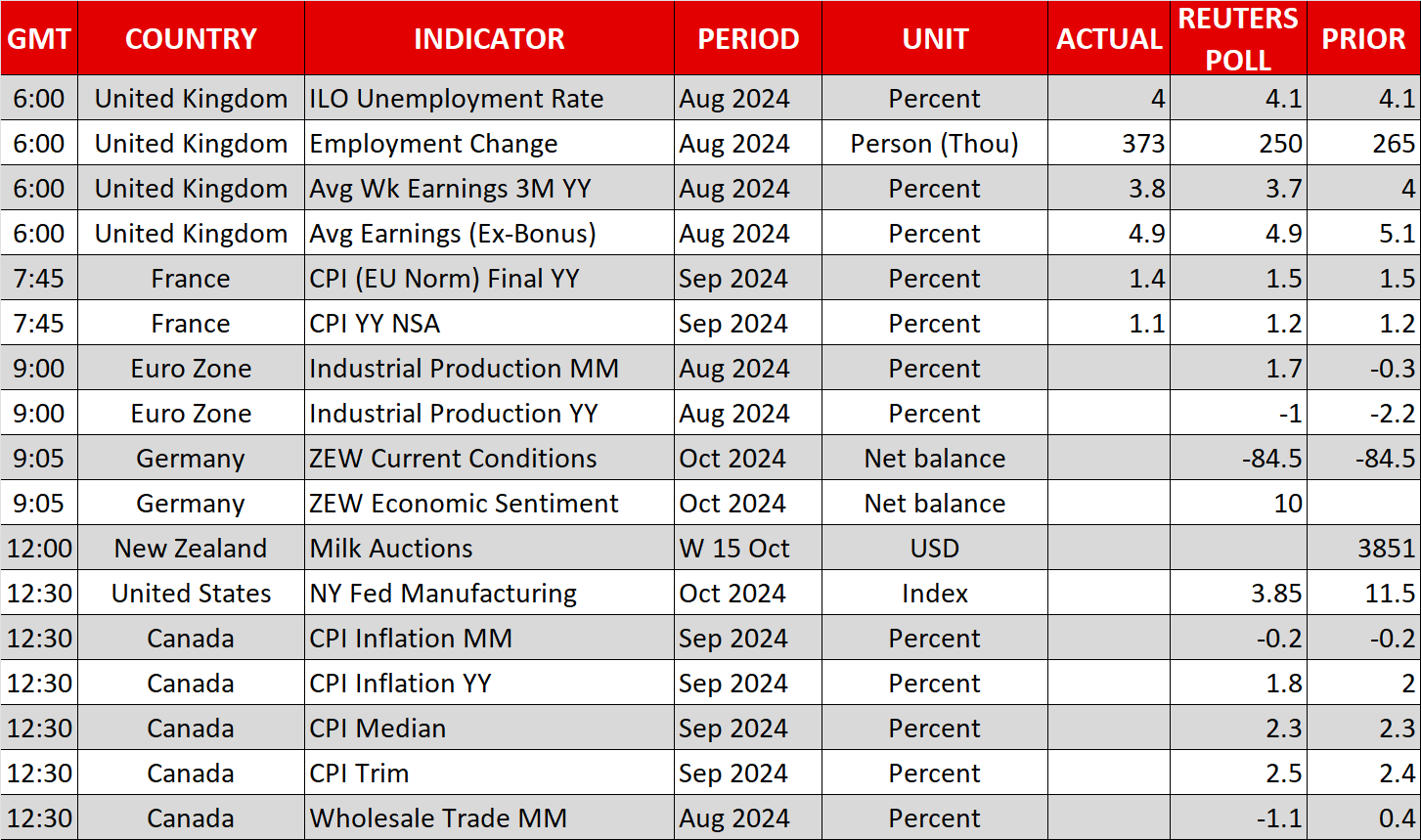

The latest UK labour market data has failed to please the pound as the unemployment rate ticked lower, but the claimant count printed above expectations and the average earnings figures edged a tad lower. Tomorrow’s CPI report remains the decisive release for the November rate cut, which is overwhelmingly priced in by the market.

Actifs liés

Dernières actualités

Avertissement : Les entités de XM Group proposent à notre plateforme de trading en ligne un service d'exécution uniquement, autorisant une personne à consulter et/ou à utiliser le contenu disponible sur ou via le site internet, qui n'a pas pour but de modifier ou d'élargir cette situation. De tels accès et utilisation sont toujours soumis aux : (i) Conditions générales ; (ii) Avertissements sur les risques et (iii) Avertissement complet. Un tel contenu n'est par conséquent fourni que pour information générale. En particulier, sachez que les contenus de notre plateforme de trading en ligne ne sont ni une sollicitation ni une offre de participation à toute transaction sur les marchés financiers. Le trading sur les marchés financiers implique un niveau significatif de risques pour votre capital.

Tout le matériel publié dans notre Centre de trading en ligne est destiné à des fins de formation / d'information uniquement et ne contient pas – et ne doit pas être considéré comme contenant – des conseils et recommandations en matière de finance, de fiscalité des investissements ou de trading, ou un enregistrement de nos prix de trading ou une offre, une sollicitation, une transaction à propos de tout instrument financier ou bien des promotions financières non sollicitées à votre égard.

Tout contenu tiers, de même que le contenu préparé par XM, tels que les opinions, actualités, études, analyses, prix, autres informations ou liens vers des sites tiers contenus sur ce site internet sont fournis "tels quels", comme commentaires généraux sur le marché et ne constituent pas des conseils en investissement. Dans la mesure où tout contenu est considéré comme de la recherche en investissement, vous devez noter et accepter que le contenu n'a pas été conçu ni préparé conformément aux exigences légales visant à promouvoir l'indépendance de la recherche en investissement et, en tant que tel, il serait considéré comme une communication marketing selon les lois et réglementations applicables. Veuillez vous assurer que vous avez lu et compris notre Avis sur la recherche en investissement non indépendante et notre avertissement sur les risques concernant les informations susdites, qui peuvent consultés ici.