Will Alphabet’s earnings tempt investors to buy more of its stock? – Stock Markets

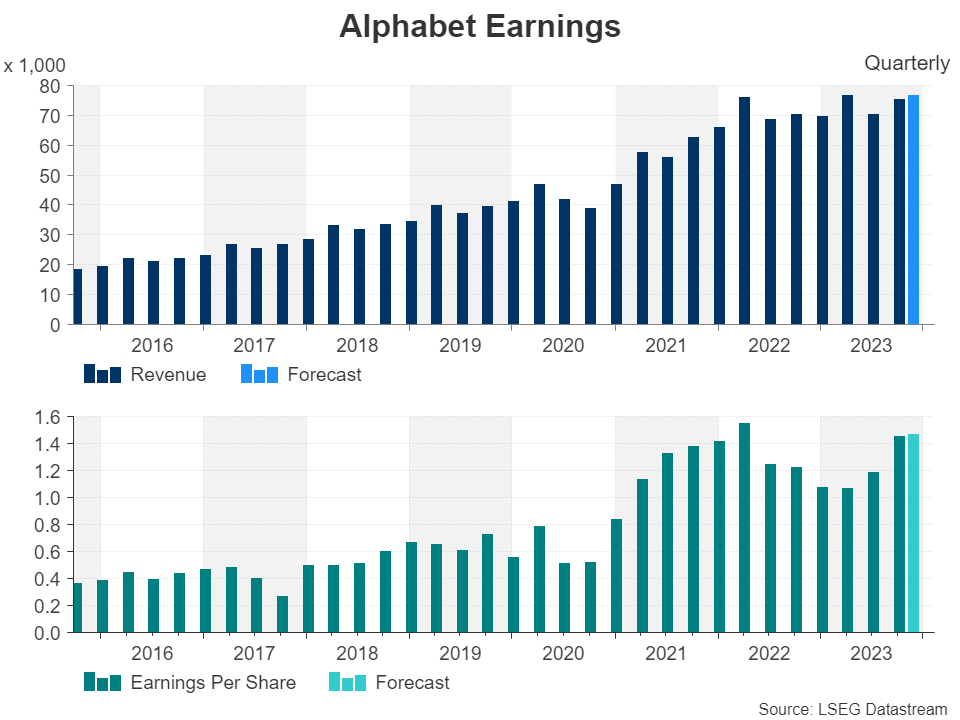

Alphabet is expected to report a nearly 10% increase in revenue

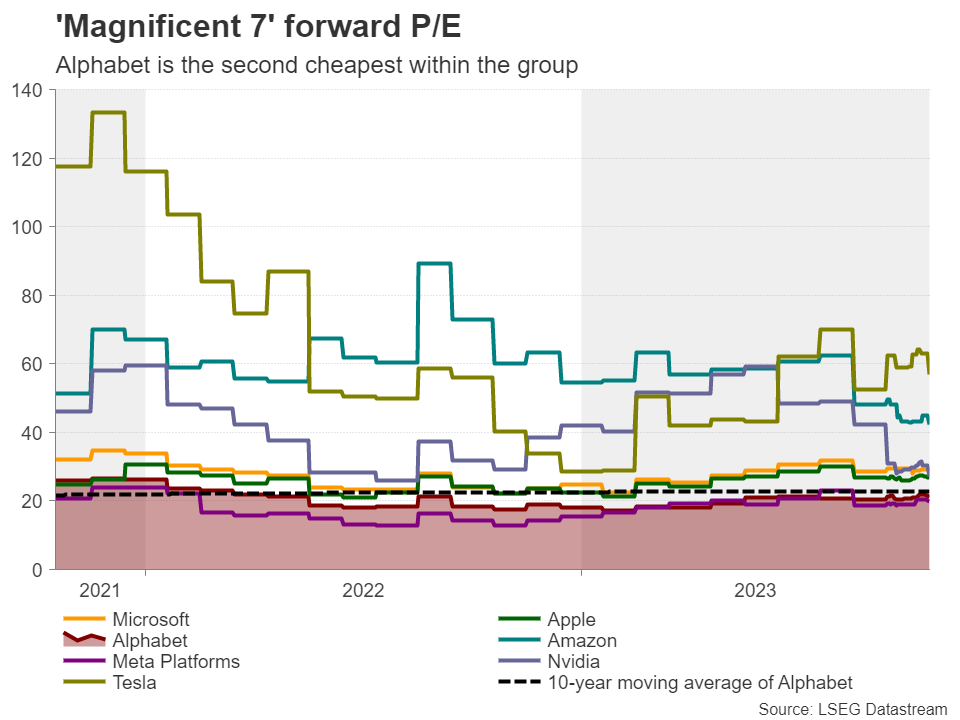

Despite latest rally, it remains relatively cheap compared to its peers

Results are scheduled to be released on October 24, after closing bell

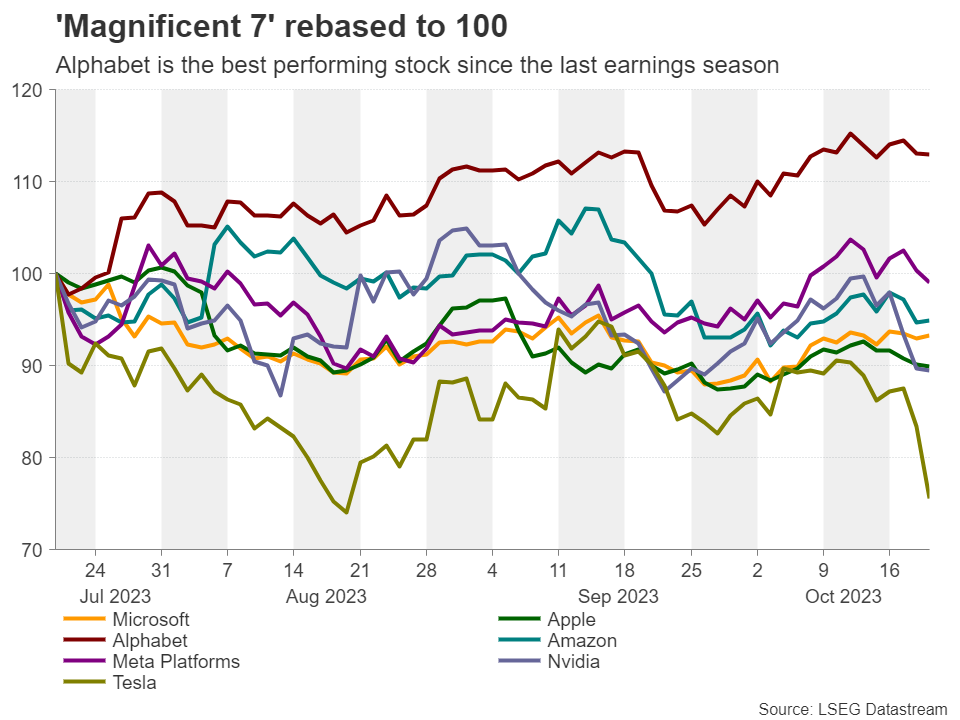

Since the prior earnings season, when Alphabet reported better-than-expected results for Q2, the firm’s shares rose more than 10%, outperforming all the other US mega-cap tech companies of the ‘Magnificent 7’ group.

On Tuesday, Google’s parent is forecast to announce earnings per share (EPS) of $1.45 during Q3, which would mark an impressive jump of 36.61% from the same period last year, while revenue is seen growing 9.91% to $75.94bn, which will mark the biggest y/y increase since Q2 2022. It is also worth mentioning that EPS returned to growth only in Q2 this year after six quarters of deterioration.

Back then, the highlights were Google Cloud and YouTube ads, which were the two biggest contributors to the overall revenue growth. Therefore, it would be interesting to see whether momentum continued in Q3.

Advertisement to take center stageWith the Google advertising segment accounting for around 78% of the firm’s revenue, YouTube ads as well as ads on Google’s search engine may play a determinant role on where the stock may be headed next, even if the initial reaction is triggered by any deviations from the EPS and overall revenue projections.

Google search is estimated to have around a 90% share of the search-engine market, and it is not a surprise that the antitrust case against its monopoly has attracted special attention. That said, even with the trials going on, investors expect the advertising sector’s revenue to grow by 6.44% y/y, nearly double the growth rate it posted in Q2.

On top of that, YouTube ads revenue received a boost in Q2 thanks to the offering of Shorts, a streaming service, and Primetime Channels, with the future looking more promising than the past. Yes, advertising may have been more cautious this year due to very high interest rates, and investors may have concerns that an economic slowdown could hinder a potential rebound even if interest rates begin to fall at some point, but the US Presidential elections and the Olympic games could very well offset this uncertainty, as these events have been historically proven to be major drivers in ad spend.

Cloud and AI business also in focusGoogle’s Cloud business grew around 28% in each of the prior quarters of the year, but it is now expected to have slowed to around 26%. Maybe the slowdown was due to higher interest rates weighing on consumption growth. With that in mind, it will be interesting to see whether expectations of rate cuts by the Fed next year will positively impact the firm’s projections of revenue from this service.

Regarding the artificial intelligence (AI) business, Microsoft’s ChatGPT initially appeared to be a major threat to Google’s Search, but Alphabet introduced its own chatbot, named Bard, which appears to be a more personalized service than ChatGPT that is more of a writing content-generating machine. As Bard is able to make personal suggestions, like creating vacation plans or recommending a diet, it could very well help the firm grow its advertising revenue even more.

Valuation adds to attractivenessAlthough Alphabet is the best performing stock within the ‘Magnificent 7’ group since the last earnings season, it holds only the fourth place year-to-date, while from a multiples’ perspective, it appears to be the second cheapest, with a forward price-to-earnings ratio (P/E) of 21.4x. This multiple is slightly above the forward P/E ratio of the S&P 500 of 18.3x, but below its own 10-year moving average.

All this adds to the stock’s attractiveness, and even if the EPS or revenue results disappoint, a slide in the share price may be seen by investors as an opportunity to enter the market at more favorable levels.

Will the uptrend continue?From a technical standpoint, Alphabet’s stock entered a consolidation phase after hitting a one-and-a-half year high near the 141.00 zone on October 12. However, it remains in a broader uptrend, as the price structure remains of higher highs and higher lows above the uptrend line drawn from the low of April 26. Thus, even if it corrects lower in the near future, as long as it remains above that line, investors could well jump back into the action and drive the price up for another test near the 141.00 zone, or near 144.00, which is marked by the peak of March 29, 2022.

For the outlook to turn bearish, the stock may need to dive all the way below the 127.50 territory, which provided strong support in August and September, and acted as key resistance in June.

For the outlook to turn bearish, the stock may need to dive all the way below the 127.50 territory, which provided strong support in August and September, and acted as key resistance in June.Các tài sản liên quan

Tin mới

Khước từ trách nhiệm: các tổ chức thuộc XM Group chỉ cung cấp dịch vụ khớp lệnh và truy cập Trang Giao dịch trực tuyến của chúng tôi, cho phép xem và/hoặc sử dụng nội dung có trên trang này hoặc thông qua trang này, mà hoàn toàn không có mục đích thay đổi hoặc mở rộng. Việc truy cập và sử dụng như trên luôn phụ thuộc vào: (i) Các Điều kiện và Điều khoản; (ii) Các Thông báo Rủi ro; và (iii) Khước từ trách nhiệm toàn bộ. Các nội dung như vậy sẽ chỉ được cung cấp dưới dạng thông tin chung. Đặc biệt, xin lưu ý rằng các thông tin trên Trang Giao dịch trực tuyến của chúng tôi không phải là sự xúi giục, mời chào để tham gia bất cứ giao dịch nào trên các thị trường tài chính. Giao dịch các thị trường tài chính có rủi ro cao đối với vốn đầu tư của bạn.

Tất cả các tài liệu trên Trang Giao dịch trực tuyến của chúng tôi chỉ nhằm các mục đích đào tạo/cung cấp thông tin và không bao gồm - và không được coi là bao gồm - các tư vấn tài chính, đầu tư, thuế, hoặc giao dịch, hoặc là một dữ liệu về giá giao dịch của chúng tôi, hoặc là một lời chào mời, hoặc là một sự xúi giục giao dịch các sản phẩm tài chính hoặc các chương trình khuyến mãi tài chính không tự nguyện.

Tất cả nội dung của bên thứ ba, cũng như nội dung của XM như các ý kiến, tin tức, nghiên cứu, phân tích, giá cả, các thông tin khác hoặc các đường dẫn đến trang web của các bên thứ ba có trên trang web này được cung cấp với dạng "nguyên trạng", là các bình luận chung về thị trường và không phải là các tư vấn đầu tư. Với việc các nội dung đều được xây dựng với mục đích nghiên cứu đầu tư, bạn cần lưu ý và hiểu rằng các nội dung này không nhằm mục đích và không được biên soạn để tuân thủ các yêu cầu pháp lý đối với việc quảng bá nghiên cứu đầu tư này và vì vậy, được coi như là một tài liệu tiếp thị. Hãy chắc chắn rằng bạn đã đọc và hiểu Thông báo về Nghiên cứu Đầu tư không độc lập và Cảnh báo Rủi ro tại đây liên quan đến các thông tin ở trên.