Turkish lira falls apart, what can turn the tide?

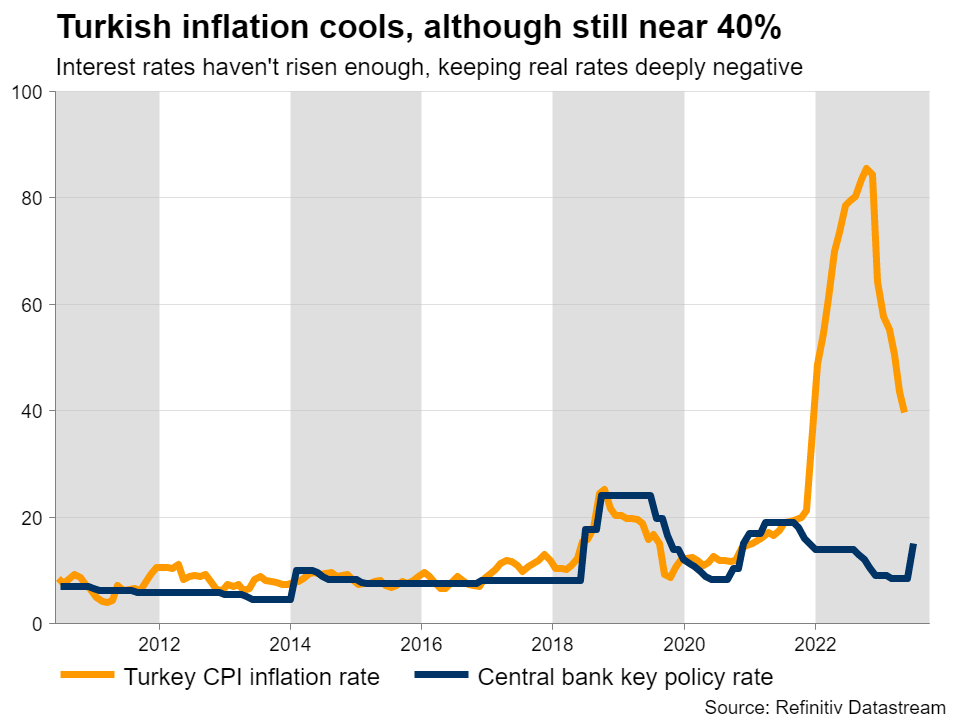

That’s only half the story, though. Another element that ravaged the lira was the central bank’s latest decision on interest rates. With a new governor coming in, there was rampant speculation about a massive increase in rates to fight runaway inflation. Some economists expected rates to be raised immediately to 25%, so when the central bank only lifted them to 15%, investors saw that as a huge disappointment. With inflation running around 40%, this move was seen as a ‘half measure’ that won’t be sufficient in cooling the economy down. Behind the downtrendTaking a step back, the lira’s downtrend is not a new phenomenon. The currency has been in decline for more than two decades, although the losses accelerated sharply after 2018 as inflation started to fire up and the nation’s deficits blew up. When inflation moves far higher but interest rates don’t follow suit, the result is that real interest rates fall deep into negative territory. That’s toxic for the lira because it discourages investors and consumers from holding it. Nobody wants to keep a currency that is constantly losing its value, if they are not compensated through high interest rates.

That’s only half the story, though. Another element that ravaged the lira was the central bank’s latest decision on interest rates. With a new governor coming in, there was rampant speculation about a massive increase in rates to fight runaway inflation. Some economists expected rates to be raised immediately to 25%, so when the central bank only lifted them to 15%, investors saw that as a huge disappointment. With inflation running around 40%, this move was seen as a ‘half measure’ that won’t be sufficient in cooling the economy down. Behind the downtrendTaking a step back, the lira’s downtrend is not a new phenomenon. The currency has been in decline for more than two decades, although the losses accelerated sharply after 2018 as inflation started to fire up and the nation’s deficits blew up. When inflation moves far higher but interest rates don’t follow suit, the result is that real interest rates fall deep into negative territory. That’s toxic for the lira because it discourages investors and consumers from holding it. Nobody wants to keep a currency that is constantly losing its value, if they are not compensated through high interest rates.  Many have attributed the central bank’s reluctance to raise rates to political pressure from President Erdogan, who has characterized high interest rates as “the mother and father of all evil”. The fact the central bank has changed its Governor four times over the last five years is a testament to this political arm-twisting, as Erdogan simply replaced any leaders that dared to raise rates much. Therefore, it can be argued the central bank has effectively lost its independence, leaving it unable to take the actions necessary to extinguish inflation. Even the new governor - who has a background as a Wall Street banker - could not break this spell. Making matters worse for the lira, Turkey runs a chronic current account deficit, which has swelled in recent years. That means the nation is a net-borrower, importing more than it exports and relying on capital flows from abroad to finance the difference. Over time, these deficits can exert massive downward pressure on a currency, especially if they keep widening.

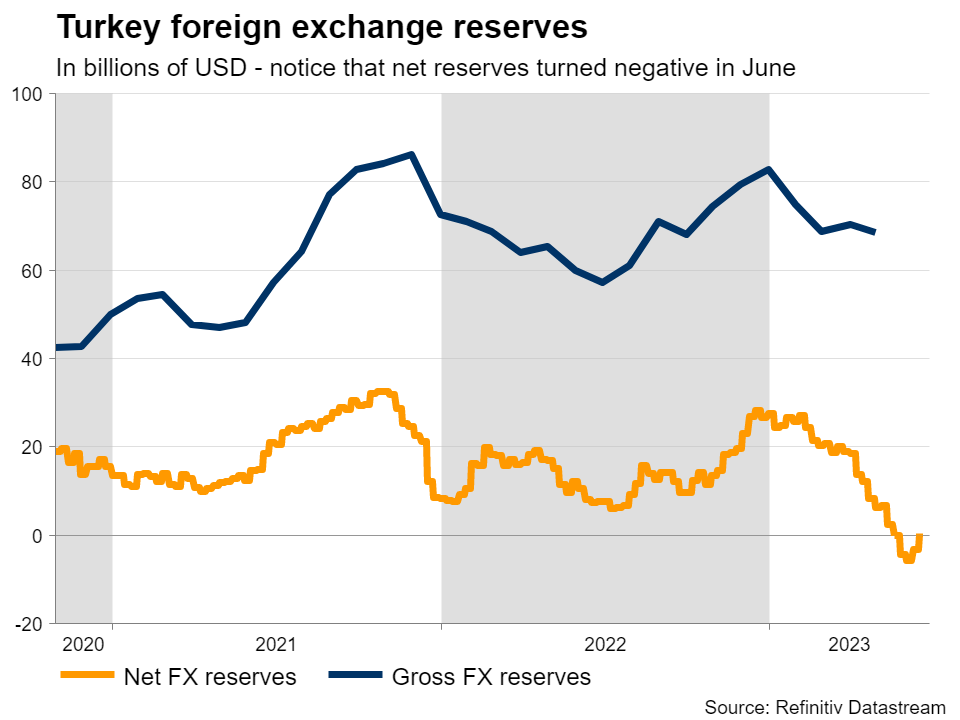

Many have attributed the central bank’s reluctance to raise rates to political pressure from President Erdogan, who has characterized high interest rates as “the mother and father of all evil”. The fact the central bank has changed its Governor four times over the last five years is a testament to this political arm-twisting, as Erdogan simply replaced any leaders that dared to raise rates much. Therefore, it can be argued the central bank has effectively lost its independence, leaving it unable to take the actions necessary to extinguish inflation. Even the new governor - who has a background as a Wall Street banker - could not break this spell. Making matters worse for the lira, Turkey runs a chronic current account deficit, which has swelled in recent years. That means the nation is a net-borrower, importing more than it exports and relying on capital flows from abroad to finance the difference. Over time, these deficits can exert massive downward pressure on a currency, especially if they keep widening.  The government has tried all sorts of unconventional tactics to stop the lira’s bleeding, such as making it more difficult to short the currency, introducing special savings accounts that compensate consumers if the lira falls sharply, and de facto confiscating foreign currencies from private banks to boost its FX reserves. These moves helped slow down the pace of depreciation for some time, alongside regular FX interventions, albeit at the cost of draining reserves. What’s next Looking ahead, there isn’t much that can turn the tides in the lira. What the currency desperately needs are higher interest rates, to slow down nominal growth and eradicate inflationary pressures, a painful process that will most likely involve a recession. Yet, President Erdogan seems determined not to let that happen. Slashing government spending could help to lower inflation, although this strategy might still be bearish for the lira initially, given its negative implications for economic growth. Plus, fiscal austerity would be a wildly unpopular move politically, making it seem even less likely.

The government has tried all sorts of unconventional tactics to stop the lira’s bleeding, such as making it more difficult to short the currency, introducing special savings accounts that compensate consumers if the lira falls sharply, and de facto confiscating foreign currencies from private banks to boost its FX reserves. These moves helped slow down the pace of depreciation for some time, alongside regular FX interventions, albeit at the cost of draining reserves. What’s next Looking ahead, there isn’t much that can turn the tides in the lira. What the currency desperately needs are higher interest rates, to slow down nominal growth and eradicate inflationary pressures, a painful process that will most likely involve a recession. Yet, President Erdogan seems determined not to let that happen. Slashing government spending could help to lower inflation, although this strategy might still be bearish for the lira initially, given its negative implications for economic growth. Plus, fiscal austerity would be a wildly unpopular move politically, making it seem even less likely.  That leaves structural reforms and regulatory changes, but admittedly, it’s highly doubtful any such policies would be powerful enough to rescue the currency. If there were easy solutions from a legislative perspective, they would have been implemented already. As such, it’s difficult to see a path towards a sustainable FX recovery, at least under the current political leadership. While a near-term correction seems plausible after such a dramatic downfall, it is unlikely to go very far, with real rates so deep in negative territory and FX reserves exhausted.

That leaves structural reforms and regulatory changes, but admittedly, it’s highly doubtful any such policies would be powerful enough to rescue the currency. If there were easy solutions from a legislative perspective, they would have been implemented already. As such, it’s difficult to see a path towards a sustainable FX recovery, at least under the current political leadership. While a near-term correction seems plausible after such a dramatic downfall, it is unlikely to go very far, with real rates so deep in negative territory and FX reserves exhausted. Các tài sản liên quan

Tin mới

Khước từ trách nhiệm: các tổ chức thuộc XM Group chỉ cung cấp dịch vụ khớp lệnh và truy cập Trang Giao dịch trực tuyến của chúng tôi, cho phép xem và/hoặc sử dụng nội dung có trên trang này hoặc thông qua trang này, mà hoàn toàn không có mục đích thay đổi hoặc mở rộng. Việc truy cập và sử dụng như trên luôn phụ thuộc vào: (i) Các Điều kiện và Điều khoản; (ii) Các Thông báo Rủi ro; và (iii) Khước từ trách nhiệm toàn bộ. Các nội dung như vậy sẽ chỉ được cung cấp dưới dạng thông tin chung. Đặc biệt, xin lưu ý rằng các thông tin trên Trang Giao dịch trực tuyến của chúng tôi không phải là sự xúi giục, mời chào để tham gia bất cứ giao dịch nào trên các thị trường tài chính. Giao dịch các thị trường tài chính có rủi ro cao đối với vốn đầu tư của bạn.

Tất cả các tài liệu trên Trang Giao dịch trực tuyến của chúng tôi chỉ nhằm các mục đích đào tạo/cung cấp thông tin và không bao gồm - và không được coi là bao gồm - các tư vấn tài chính, đầu tư, thuế, hoặc giao dịch, hoặc là một dữ liệu về giá giao dịch của chúng tôi, hoặc là một lời chào mời, hoặc là một sự xúi giục giao dịch các sản phẩm tài chính hoặc các chương trình khuyến mãi tài chính không tự nguyện.

Tất cả nội dung của bên thứ ba, cũng như nội dung của XM như các ý kiến, tin tức, nghiên cứu, phân tích, giá cả, các thông tin khác hoặc các đường dẫn đến trang web của các bên thứ ba có trên trang web này được cung cấp với dạng "nguyên trạng", là các bình luận chung về thị trường và không phải là các tư vấn đầu tư. Với việc các nội dung đều được xây dựng với mục đích nghiên cứu đầu tư, bạn cần lưu ý và hiểu rằng các nội dung này không nhằm mục đích và không được biên soạn để tuân thủ các yêu cầu pháp lý đối với việc quảng bá nghiên cứu đầu tư này và vì vậy, được coi như là một tài liệu tiếp thị. Hãy chắc chắn rằng bạn đã đọc và hiểu Thông báo về Nghiên cứu Đầu tư không độc lập và Cảnh báo Rủi ro tại đây liên quan đến các thông tin ở trên.