Market Comment – Better-than-expected US PMIs help the dollar rebound

PMIs suggest the US economy entered Q4 on solid footing

The divergence between US/Eurozone outlooks weighs on euro/dollar

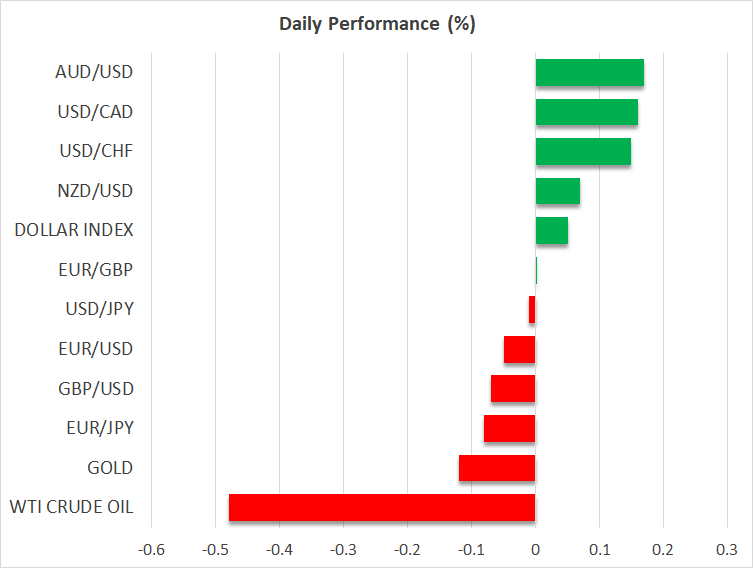

Aussie rallies on stickier inflation, yen pinned near 150-per-dollar mark

Wall Street pays attention to corporate earnings

Euro/dollar slides from near key resistance on PMI data

Euro/dollar slides from near key resistance on PMI dataAlthough the 10-year US Treasury yield held steady comfortably below the psychological zone of 5%, the US dollar was able to stage a comeback against most of its major counterparts as the flash US PMIs for October suggested that the world’s largest economy fared better than expected during the first month of the fourth quarter, with the manufacturing index escaping a contraction for the first time since April, and the composite index rising to 51.0 from 50.2.

This came in huge contrast to the Euro-area PMIs for the month that were released earlier in the day and painted an even uglier picture than they did in September. The divergence allowed euro/dollar bears to jump into the action from near the crossroads of the pair's 50-day moving average and the key resistance barrier of 1.0665, suggesting the latest recovery may have been just a corrective wave within the broader downtrend.

Dollar traders turn gaze to Q3 GDPThe slide may extend, and the pair could soon retest this month’s lows if Thursday’s data reveal astounding performance of the US economy in Q3. Expectations are for a solid 4.2% annualized growth rate, with the risks perhaps tilted to the upside as the Atlanta Fed GDPNow model estimates that the US economy may have grown 5.4% during that period.

The fact that Treasury yields did not track the dollar’s rebound may be an indication that investors were still reluctant to add to bets of another hike by the Fed after the better PMIs. Indeed, according to Fed funds futures, there is only a 40% chance for one final 25bps increase by January, while there are still around 80bps worth of rate reductions penciled in for next year. That said, the implied path could well be lifted, and rate cuts could be scaled back if upcoming data continues to point to a resilient US economy.

Aussie extends gains after CPIs, dollar/yen pinned near 150The aussie was among the currencies that outperformed the dollar yesterday, spiking even higher today after data showed that Australia’s inflation slowed by less than expected in Q3 and that the monthly y/y rate for September rose to 5.6% from 5.2%. This prompted investors to add to their bets of more hikes by the RBA, with the probability of another quarter-point increase at the November gathering rising to around 42%.

The yen attempted a recovery at some point yesterday, but the rebound in the dollar pinned the dollar/yen pair back near the highly monitored 150 territory, with traders biting their nails in anticipation of any signs of intervention by Japanese authorities. What could reveal whether officials are ready to act now or whether the level at which they feel comfortable intervening has shifted higher, may be a stellar US GDP print tomorrow that could force the pair to pierce through that psychological ceiling.

Wall Street ekes out gains, driven by upbeat earningsWall Street closed Tuesday in the green after upbeat forecasts from Verizon, Coca-Cola and other firms sparked optimism regarding the health of US businesses, encouraging investors to increase their risk exposure. The fact that the Fed’s implied rate path was not lifted after the better PMIs may have also helped Wall Street, which seems to be slowly shifting its attention away from the Middle East conflict.

After the closing bell, both Microsoft and Alphabet reported better-than-expected results, but the performance of their cloud services diverged. Microsoft’s Azure took off during the third quarter, but Alphabet’s cloud business saw its slowest growth in at least 11 quarters. After today’s close, it will be the turn of Meta Platforms to announce results.

In another sign that the financial world is turning its focus away from geopolitics, oil prices fell for the third straight day yesterday, perhaps as weak business surveys from the Eurozone and the UK weighed on the demand outlook.

Các tài sản liên quan

Tin mới

Khước từ trách nhiệm: các tổ chức thuộc XM Group chỉ cung cấp dịch vụ khớp lệnh và truy cập Trang Giao dịch trực tuyến của chúng tôi, cho phép xem và/hoặc sử dụng nội dung có trên trang này hoặc thông qua trang này, mà hoàn toàn không có mục đích thay đổi hoặc mở rộng. Việc truy cập và sử dụng như trên luôn phụ thuộc vào: (i) Các Điều kiện và Điều khoản; (ii) Các Thông báo Rủi ro; và (iii) Khước từ trách nhiệm toàn bộ. Các nội dung như vậy sẽ chỉ được cung cấp dưới dạng thông tin chung. Đặc biệt, xin lưu ý rằng các thông tin trên Trang Giao dịch trực tuyến của chúng tôi không phải là sự xúi giục, mời chào để tham gia bất cứ giao dịch nào trên các thị trường tài chính. Giao dịch các thị trường tài chính có rủi ro cao đối với vốn đầu tư của bạn.

Tất cả các tài liệu trên Trang Giao dịch trực tuyến của chúng tôi chỉ nhằm các mục đích đào tạo/cung cấp thông tin và không bao gồm - và không được coi là bao gồm - các tư vấn tài chính, đầu tư, thuế, hoặc giao dịch, hoặc là một dữ liệu về giá giao dịch của chúng tôi, hoặc là một lời chào mời, hoặc là một sự xúi giục giao dịch các sản phẩm tài chính hoặc các chương trình khuyến mãi tài chính không tự nguyện.

Tất cả nội dung của bên thứ ba, cũng như nội dung của XM như các ý kiến, tin tức, nghiên cứu, phân tích, giá cả, các thông tin khác hoặc các đường dẫn đến trang web của các bên thứ ba có trên trang web này được cung cấp với dạng "nguyên trạng", là các bình luận chung về thị trường và không phải là các tư vấn đầu tư. Với việc các nội dung đều được xây dựng với mục đích nghiên cứu đầu tư, bạn cần lưu ý và hiểu rằng các nội dung này không nhằm mục đích và không được biên soạn để tuân thủ các yêu cầu pháp lý đối với việc quảng bá nghiên cứu đầu tư này và vì vậy, được coi như là một tài liệu tiếp thị. Hãy chắc chắn rằng bạn đã đọc và hiểu Thông báo về Nghiên cứu Đầu tư không độc lập và Cảnh báo Rủi ro tại đây liên quan đến các thông tin ở trên.