Daily Market Comment – Markets calm before the central bank storm

Massive week begins, featuring rate decisions in US, Europe, and Japan

US inflation report also on tap tomorrow, could influence Fed decision

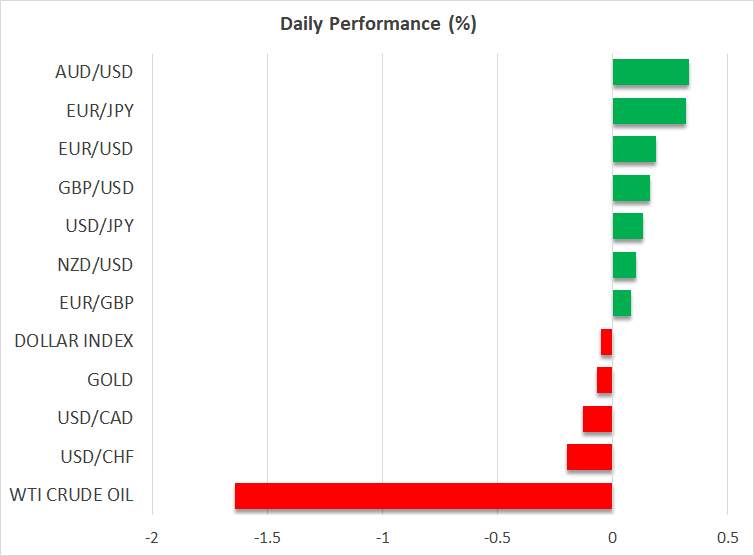

Yen hits seven-year low against pound, Turkish lira goes into freefall

Calm ahead of key events

A bombshell week lies ahead for global markets. Interest rate decisions in the United States, Eurozone, and Japan will almost certainly fuel volatility in every asset class, especially if the rhetoric of these central banks deviates from the prevailing market consensus.

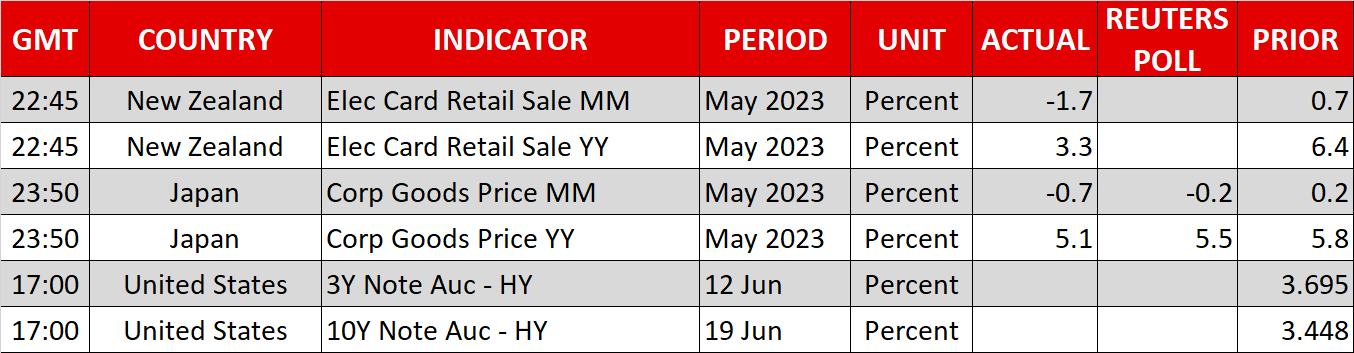

In the United States, the ball will get rolling tomorrow with the release of the latest CPI inflation data, which will be instrumental in shaping expectations around the Fed decision on Wednesday.

Even though the US economic data pulse is still pretty strong, with the labor market in good shape and GDP growth on track to hit 2% this quarter, market pricing only assigns a 25% probability for a rate increase this week. That’s because several Fed officials have signaled they prefer to ‘play it slow’ and examine incoming data before raising rates again.

Unless something dramatic changes after tomorrow’s CPI data, the Fed will probably ‘pause’ the tightening cycle this week, shifting the emphasis to the updated rate projections and any messages about the likelihood of resuming rate hikes in July. Hence, the reaction in the dollar will depend on several elements, including also how foreign central banks behave.

ECB could disappoint euro

Over in the Eurozone, the economy has fallen into a technical recession but that’s unlikely to stop the European Central Bank from raising rates on Thursday. A rate increase of 25bps is fully priced in, as the ECB has telegraphed its intentions well in advance.

Therefore, this meeting will be about how the ECB wishes to move forward. Market pricing suggests another rate hike is in the pipeline for July, yet the central bank might refuse to pre-commit to that, as incoming data suggest economic growth is rolling over and inflation is cooling.

Under these circumstances, the ECB is more likely to preach caution and patience, keeping its options open. The economy is already contracting and the last thing the central bank wants is to pour gasoline on the recessionary fire. If the ECB mimics the Fed and signals it might ‘take a break’ next month, the euro could be left disappointed.

GBP/JPY reaches highest levels since 2016

The past few months have been a perfect storm for pound/yen, which is trading at its highest levels since 2016, turbocharged by a blend of central bank divergence and favorable risk sentiment. Rate differentials have widened lately as investors bet the Bank of England will be forced to keep tightening but the Bank of Japan won’t join the race anytime soon, and the euphoric tone in stock markets has been similarly advantageous for risk-correlated FX pairs.

What the BoJ does on Friday could decide whether the yen keeps sinking. The Japanese economic landscape has improved by leaps and bounds, but it’s likely too early for the BoJ to hit the tightening button as many officials are concerned the recent victories on inflation and wages won’t be sustained. If the BoJ remains sidelined, that would leave the yen at the mercy of external forces, namely how risk appetite evolves.

Finally, the Turkish lira has gone into freefall, hitting another record low this week. The appointment of Gaye Erkan as central bank governor on Friday did nothing to calm the currency crisis, despite speculation she could triple interest rates to 25% from 8.5% currently. It seems even the prospect of dramatically higher rates is not enough to soothe investors' concerns, given the risk that such a sharp tightening in credit conditions will ultimately produce a recession.

Các tài sản liên quan

Tin mới

Khước từ trách nhiệm: các tổ chức thuộc XM Group chỉ cung cấp dịch vụ khớp lệnh và truy cập Trang Giao dịch trực tuyến của chúng tôi, cho phép xem và/hoặc sử dụng nội dung có trên trang này hoặc thông qua trang này, mà hoàn toàn không có mục đích thay đổi hoặc mở rộng. Việc truy cập và sử dụng như trên luôn phụ thuộc vào: (i) Các Điều kiện và Điều khoản; (ii) Các Thông báo Rủi ro; và (iii) Khước từ trách nhiệm toàn bộ. Các nội dung như vậy sẽ chỉ được cung cấp dưới dạng thông tin chung. Đặc biệt, xin lưu ý rằng các thông tin trên Trang Giao dịch trực tuyến của chúng tôi không phải là sự xúi giục, mời chào để tham gia bất cứ giao dịch nào trên các thị trường tài chính. Giao dịch các thị trường tài chính có rủi ro cao đối với vốn đầu tư của bạn.

Tất cả các tài liệu trên Trang Giao dịch trực tuyến của chúng tôi chỉ nhằm các mục đích đào tạo/cung cấp thông tin và không bao gồm - và không được coi là bao gồm - các tư vấn tài chính, đầu tư, thuế, hoặc giao dịch, hoặc là một dữ liệu về giá giao dịch của chúng tôi, hoặc là một lời chào mời, hoặc là một sự xúi giục giao dịch các sản phẩm tài chính hoặc các chương trình khuyến mãi tài chính không tự nguyện.

Tất cả nội dung của bên thứ ba, cũng như nội dung của XM như các ý kiến, tin tức, nghiên cứu, phân tích, giá cả, các thông tin khác hoặc các đường dẫn đến trang web của các bên thứ ba có trên trang web này được cung cấp với dạng "nguyên trạng", là các bình luận chung về thị trường và không phải là các tư vấn đầu tư. Với việc các nội dung đều được xây dựng với mục đích nghiên cứu đầu tư, bạn cần lưu ý và hiểu rằng các nội dung này không nhằm mục đích và không được biên soạn để tuân thủ các yêu cầu pháp lý đối với việc quảng bá nghiên cứu đầu tư này và vì vậy, được coi như là một tài liệu tiếp thị. Hãy chắc chắn rằng bạn đã đọc và hiểu Thông báo về Nghiên cứu Đầu tư không độc lập và Cảnh báo Rủi ro tại đây liên quan đến các thông tin ở trên.