Week Ahead – Focus on US retail sales as debt ceiling drama rumbles on

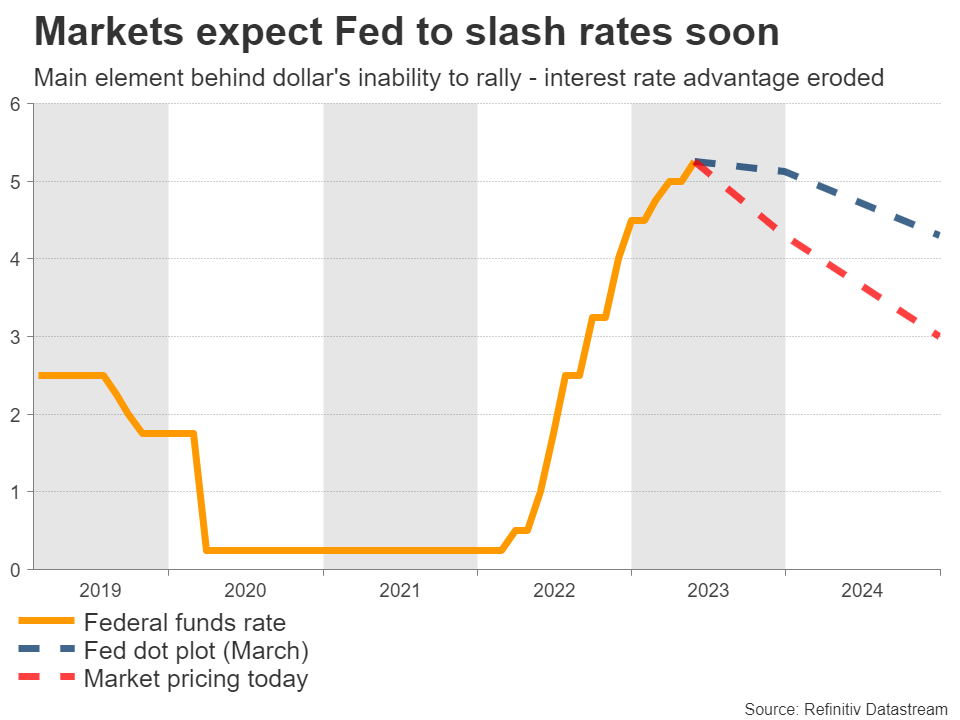

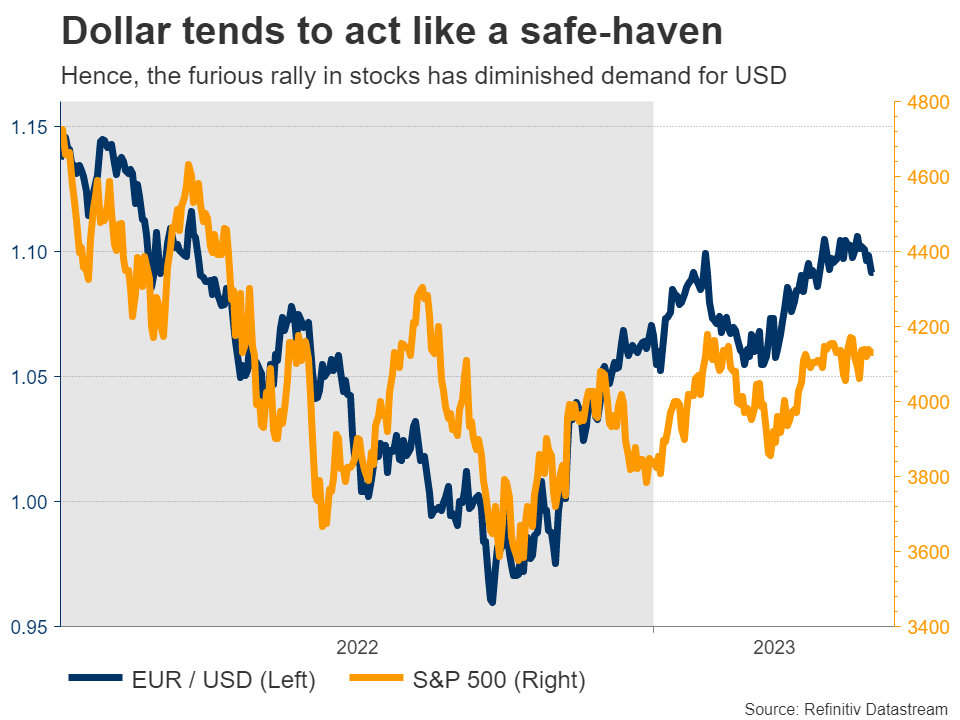

Traders seem to be betting that the problems in the banking system will override inflation concerns, forcing the Fed to reduce borrowing costs in order to avoid a domino of bank failures, even if that means tolerating a period of higher inflation. Another problem for the dollar has been the rally in stocks. Since the greenback often acts like a haven asset, the optimistic tone in markets has limited demand for the reserve currency. The charts tell the same story - the dollar index topped in late September, right before the stock market bottomed. In other words, the dollar’s yield advantage has been eroded because of rate-cut bets, and its safe-haven qualities are not very popular right now. Therefore, for the greenback to start ‘working’ again, it might need an equity selloff that fuels demand for protection or a stream of encouraging data that dispels speculation of imminent rate cuts.

Traders seem to be betting that the problems in the banking system will override inflation concerns, forcing the Fed to reduce borrowing costs in order to avoid a domino of bank failures, even if that means tolerating a period of higher inflation. Another problem for the dollar has been the rally in stocks. Since the greenback often acts like a haven asset, the optimistic tone in markets has limited demand for the reserve currency. The charts tell the same story - the dollar index topped in late September, right before the stock market bottomed. In other words, the dollar’s yield advantage has been eroded because of rate-cut bets, and its safe-haven qualities are not very popular right now. Therefore, for the greenback to start ‘working’ again, it might need an equity selloff that fuels demand for protection or a stream of encouraging data that dispels speculation of imminent rate cuts.  This puts extra emphasis on US retail sales out on Tuesday, which will reveal how consumers are holding up. Forecasts point to a 0.7% monthly increase in April, a rebound following a decline of similar size last month. This notion is supported by an increase in Visa’s US Spending Momentum Index, yet similar card data from Bank of America point to a spending rise of just 0.3% in April, presenting some downside risks. Meanwhile, debt ceiling negotiations will continue. The Treasury Secretary has warned the US could face default by early June without a deal, although in reality, it is likely closer to July. Outside of short-term Treasury yields and credit default swaps, markets haven’t cared much about this standoff so far, but that might change as the X-date draws closer. China and Japan await key dataCrossing into China, the ball will get rolling on Tuesday with retail sales, industrial production, and fixed asset investment - all for April. Investors will be looking at whether the reopening momentum has started to fade, as recent business surveys suggested. Over in Japan, things will heat up with GDP growth data for Q1 on Wednesday, ahead of the latest round of inflation stats on Friday. The Japanese economy is expected to have grown again entering 2023, albeit just barely.

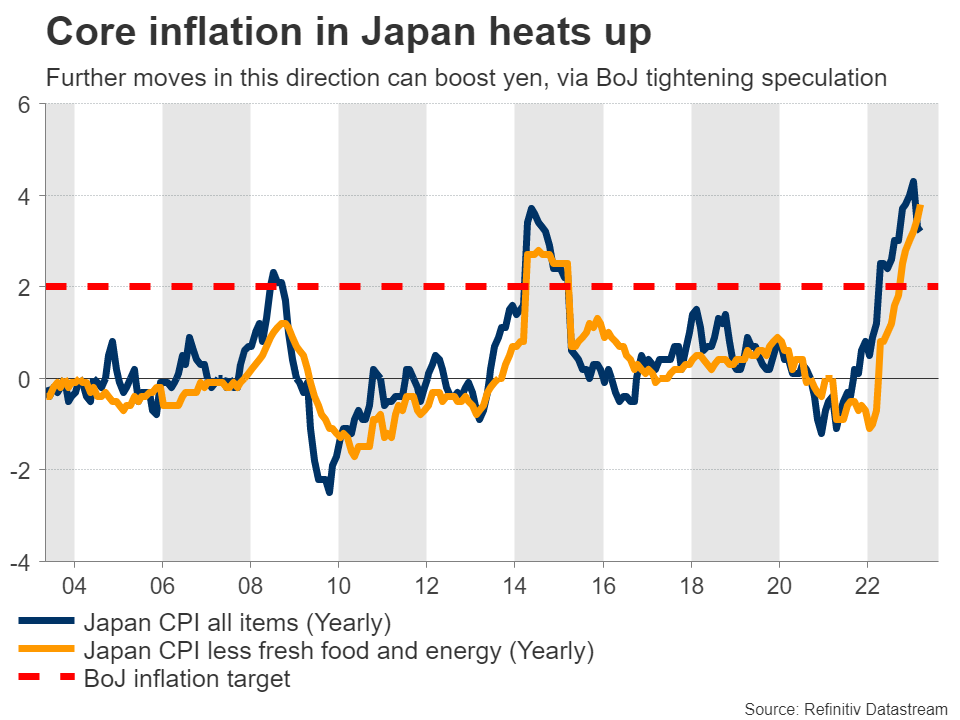

This puts extra emphasis on US retail sales out on Tuesday, which will reveal how consumers are holding up. Forecasts point to a 0.7% monthly increase in April, a rebound following a decline of similar size last month. This notion is supported by an increase in Visa’s US Spending Momentum Index, yet similar card data from Bank of America point to a spending rise of just 0.3% in April, presenting some downside risks. Meanwhile, debt ceiling negotiations will continue. The Treasury Secretary has warned the US could face default by early June without a deal, although in reality, it is likely closer to July. Outside of short-term Treasury yields and credit default swaps, markets haven’t cared much about this standoff so far, but that might change as the X-date draws closer. China and Japan await key dataCrossing into China, the ball will get rolling on Tuesday with retail sales, industrial production, and fixed asset investment - all for April. Investors will be looking at whether the reopening momentum has started to fade, as recent business surveys suggested. Over in Japan, things will heat up with GDP growth data for Q1 on Wednesday, ahead of the latest round of inflation stats on Friday. The Japanese economy is expected to have grown again entering 2023, albeit just barely.  On the inflation front, inflationary pressures probably continued to heat up in April, mirroring the forward-looking Tokyo CPIs. That would be pleasant news for the Bank of Japan, possibly fueling speculation for policy tightening in the future, perhaps this summer already. The BoJ’s reluctance to tighten policy has devastated the yen, so any hints that this might change can help the currency regain strength. Governor Ueda has signaled he’s open to tightening, provided that inflation is persistent. For the yen, the dream scenario would be for the BoJ to start tightening right as other central banks stop, during a period of turbulence in global markets.Risk-linked currencies eyed, Turkey goes to electionsTurning to currencies with strong links to risk sentiment, the British pound will be in the spotlight Tuesday with the release of jobs data for March. The Bank of England disappointed traders this week by not providing any strong clues about future action, so markets are pricing the rate decision next month almost like a coin toss. In Australia, there’s a barrage of releases starting on Tuesday with the minutes of the latest RBA meeting, where the central bank unexpectedly raised interest rates. The wage price index for Q1 will follow Wednesday, ahead of jobs numbers for April on Thursday. Over in Canada, the latest inflation stats are out Tuesday, ahead of retail sales on Friday. Market pricing suggests the Bank of Canada is done raising rates, so anything that challenges this perception could inject more volatility into the Canadian dollar, which has been shaken around lately by massive swings in oil prices.

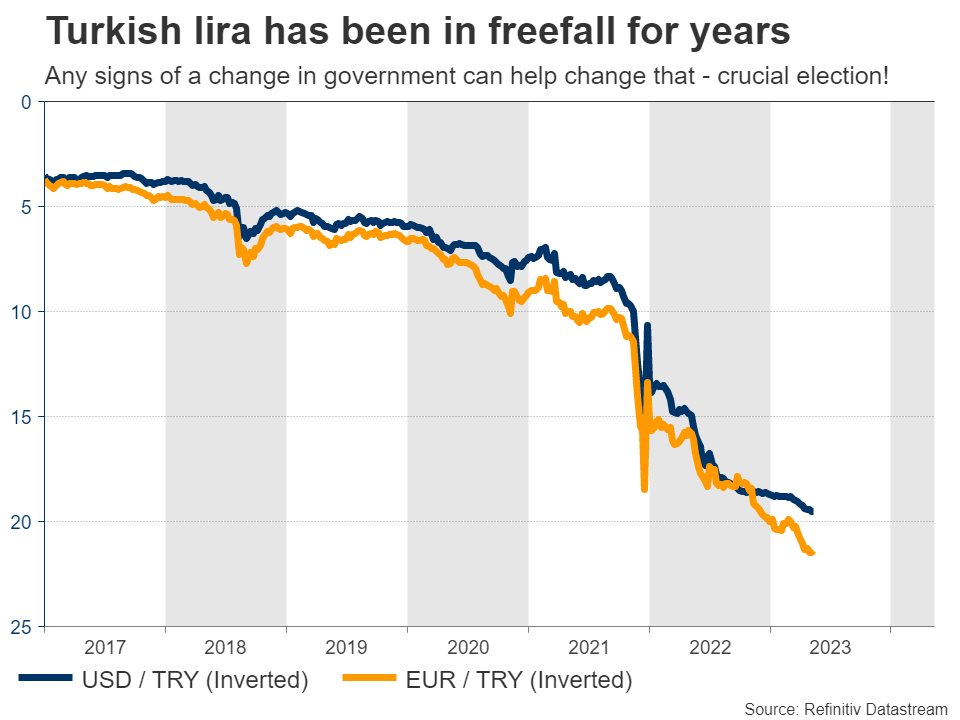

On the inflation front, inflationary pressures probably continued to heat up in April, mirroring the forward-looking Tokyo CPIs. That would be pleasant news for the Bank of Japan, possibly fueling speculation for policy tightening in the future, perhaps this summer already. The BoJ’s reluctance to tighten policy has devastated the yen, so any hints that this might change can help the currency regain strength. Governor Ueda has signaled he’s open to tightening, provided that inflation is persistent. For the yen, the dream scenario would be for the BoJ to start tightening right as other central banks stop, during a period of turbulence in global markets.Risk-linked currencies eyed, Turkey goes to electionsTurning to currencies with strong links to risk sentiment, the British pound will be in the spotlight Tuesday with the release of jobs data for March. The Bank of England disappointed traders this week by not providing any strong clues about future action, so markets are pricing the rate decision next month almost like a coin toss. In Australia, there’s a barrage of releases starting on Tuesday with the minutes of the latest RBA meeting, where the central bank unexpectedly raised interest rates. The wage price index for Q1 will follow Wednesday, ahead of jobs numbers for April on Thursday. Over in Canada, the latest inflation stats are out Tuesday, ahead of retail sales on Friday. Market pricing suggests the Bank of Canada is done raising rates, so anything that challenges this perception could inject more volatility into the Canadian dollar, which has been shaken around lately by massive swings in oil prices.  Finally in Turkey, the nation will elect its next parliament and president on Sunday. President Erdogan is lagging behind his main rival Kilicdaroglu, although neither candidate is expected to secure 50% of the votes, which means there will probably be a second round in two weeks. A strong showing by Kilicdaroglu could help the Turkish lira to appreciate, perhaps with a large gap at the open on Monday, on expectations that a new government will restore orthodox economic policies and allow the central bank to raise interest rates in order to fight runaway inflation.

Finally in Turkey, the nation will elect its next parliament and president on Sunday. President Erdogan is lagging behind his main rival Kilicdaroglu, although neither candidate is expected to secure 50% of the votes, which means there will probably be a second round in two weeks. A strong showing by Kilicdaroglu could help the Turkish lira to appreciate, perhaps with a large gap at the open on Monday, on expectations that a new government will restore orthodox economic policies and allow the central bank to raise interest rates in order to fight runaway inflation. متعلقہ اثاثے

تازہ ترين خبريں

دستبرداری: XM Group کے ادارے ہماری آن لائن تجارت کی سہولت تک صرف عملدرآمد کی خدمت اور رسائی مہیا کرتے ہیں، کسی شخص کو ویب سائٹ پر یا اس کے ذریعے دستیاب کانٹینٹ کو دیکھنے اور/یا استعمال کرنے کی اجازت دیتا ہے، اس پر تبدیل یا توسیع کا ارادہ نہیں ہے ، اور نہ ہی یہ تبدیل ہوتا ہے یا اس پر وسعت کریں۔ اس طرح کی رسائی اور استعمال ہمیشہ مشروط ہوتا ہے: (i) شرائط و ضوابط؛ (ii) خطرہ انتباہات؛ اور (iii) مکمل دستبرداری۔ لہذا اس طرح کے مواد کو عام معلومات سے زیادہ کے طور پر فراہم کیا جاتا ہے۔ خاص طور پر، براہ کرم آگاہ رہیں کہ ہماری آن لائن تجارت کی سہولت کے مندرجات نہ تو کوئی درخواست ہے، اور نہ ہی فنانشل مارکیٹ میں کوئی لین دین داخل کرنے کی پیش کش ہے۔ کسی بھی فنانشل مارکیٹ میں تجارت میں آپ کے سرمائے کے لئے ایک خاص سطح کا خطرہ ہوتا ہے۔

ہماری آن لائن تجارتی سہولت پر شائع ہونے والے تمام مٹیریل کا مقصد صرف تعلیمی/معلوماتی مقاصد کے لئے ہے، اور اس میں شامل نہیں ہے — اور نہ ہی اسے فنانشل، سرمایہ کاری ٹیکس یا تجارتی مشورے اور سفارشات؛ یا ہماری تجارتی قیمتوں کا ریکارڈ؛ یا کسی بھی فنانشل انسٹرومنٹ میں لین دین کی پیشکش؛ یا اسکے لئے مانگ؛ یا غیر متنازعہ مالی تشہیرات پر مشتمل سمجھا جانا چاہئے۔

کوئی تھرڈ پارٹی کانٹینٹ، نیز XM کے ذریعہ تیار کردہ کانٹینٹ، جیسے: راۓ، خبریں، تحقیق، تجزیہ، قیمتیں اور دیگر معلومات یا اس ویب سائٹ پر مشتمل تھرڈ پارٹی کے سائٹس کے لنکس کو "جیسے ہے" کی بنیاد پر فراہم کیا جاتا ہے، عام مارکیٹ کی تفسیر کے طور پر، اور سرمایہ کاری کے مشورے کو تشکیل نہ دیں۔ اس حد تک کہ کسی بھی کانٹینٹ کو سرمایہ کاری کی تحقیقات کے طور پر سمجھا جاتا ہے، آپ کو نوٹ کرنا اور قبول کرنا ہوگا کہ یہ کانٹینٹ سرمایہ کاری کی تحقیق کی آزادی کو فروغ دینے کے لئے ڈیزائن کردہ قانونی تقاضوں کے مطابق نہیں ہے اور تیار نہیں کیا گیا ہے، اسی طرح، اس پر غور کیا جائے گا بطور متعلقہ قوانین اور ضوابط کے تحت مارکیٹنگ مواصلات۔ براہ کرم یقینی بنائیں کہ آپ غیر آزاد سرمایہ کاری سے متعلق ہماری اطلاع کو پڑھ اور سمجھ چکے ہیں۔ مذکورہ بالا معلومات کے بارے میں تحقیق اور رسک وارننگ ، جس تک رسائی یہاں حاصل کی جا سکتی ہے۔