Market Comment – Dollar at 10-month high as yields keep surging

US 10-year yield hits 16-year high amid no letup in hawkish Fed rhetoric

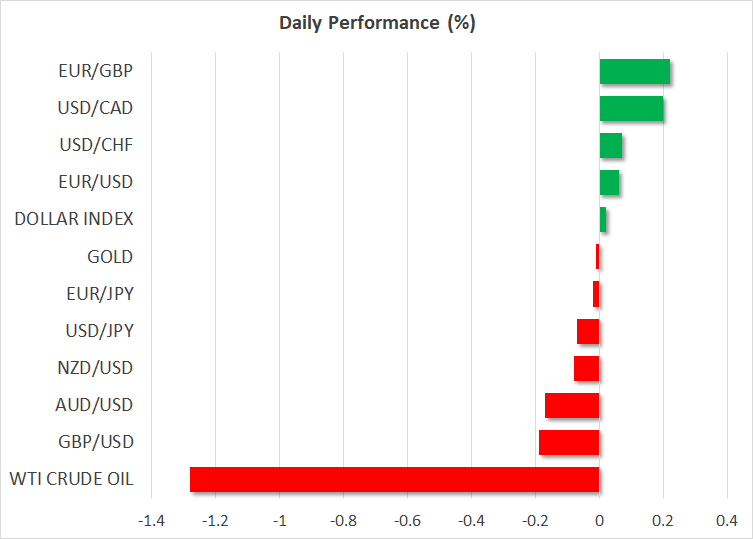

Dollar powers ahead, euro and pound crumble, yen in danger zone

Stocks resume decline after late rebound on Wall Street

Bond market rout deepens

Bond market rout deepensThe selloff in bond markets is showing no sign of easing as investors are dumping government securities in favour of cash amid expectations that interest rates in the US may yet rise further. Despite the tightening cycle nearing its end, the hawkish drumbeat from the Fed has only gotten louder, unnerving investors who were betting on rate cuts as early as in the spring of 2024.

The yield on 10-year Treasury notes broke above 4.50% on Monday for the first time since November 2007 and continues to climb to fresh highs today. The 30-year yield, meanwhile, has surged to 12½-year highs as long-term rates adjust to the Fed’s “higher for longer” mantra.

Minneapolis Fed President Neel Kashkari hinted on Monday that “rates probably have to go a little bit higher” if the US economy stays fundamentally resilient, while Chicago Fed chief Austan Goolsbee reiterated that rates will have to stay high for longer than what markers had anticipated.

The odds of one final 25-basis-point hike now stand at 50%, up from 40% prior to last week’s FOMC decision. However, there’s been no notable scaling back of rate cut expectations over the past week, suggesting that there’s room for further repricing should inflation remain stubbornly high.

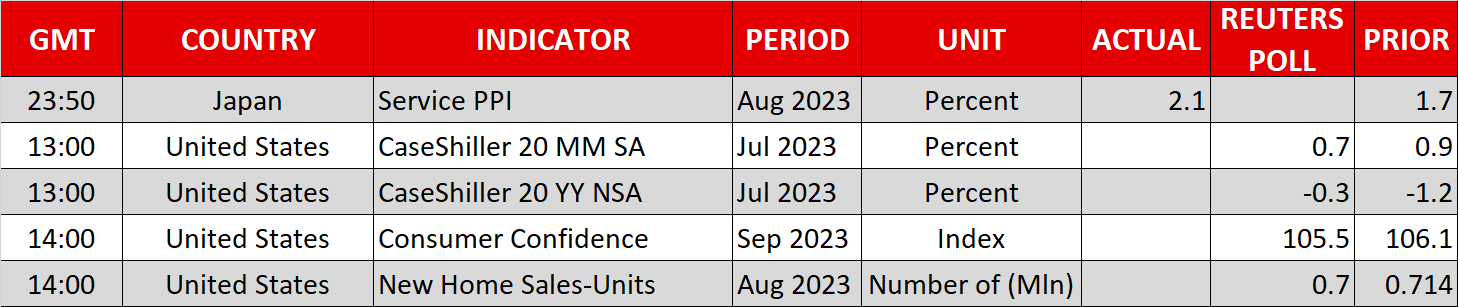

There’s no stopping the dollarThe next update on the inflation front will be Friday’s core PCE price index, which had edged up in July. If the Fed’s favourite price gauge falls to 3.9% in August as forecast, the rally in bond yields might pause for breath, halting the US dollar’s advance.

In the meantime, though, there’s no stopping the greenback as the dollar index is back above 106.0, reaching the highest since late November. What’s striking is that long-term bond yields have jumped across the board, with the exception of UK gilt yields, yet only the dollar stands tall.

The worsening economic data in Europe, China’s never-ending property crisis and the surprise rally in oil prices has dampened the prospects for most other major currencies. Even if the likes of the ECB and Bank of England are not about to cut rates anytime soon, the US economic outlook is far stronger at the moment. Moreover, a gloomy picture globally tends to draw safe haven bids for the dollar, thus there could be more gains in store in the near-to-medium term.

This can only be bad news for the euro and pound, which have slipped below the key levels of $1.06 and $1.22, respectively, over the past day.

Yen dangerously close to intervention levelThe yen is also under increasing strain as the Bank of Japan has set the bar high for warranting an exit from ultra-accommodative policy. There had been some hopes that the BoJ would soon begin laying the groundwork for an eventual exit but Governor Ueda’s dovish remarks in recent days suggest the timing remains a long way off.

That has left the yen extremely vulnerable in a landscape where there is renewed dollar upside. The greenback briefly spiked above 149 yen earlier today before easing back. The last time the yen approached the 150 level a year ago, Japanese officials had stepped up their verbal warnings before going ahead and intervening in the FX market to shore up the currency. But verbal intervention has been unusually scarce this time around, which may be an indication that the threshold has shifted somewhat.

Stocks continue to struggle despite Wall Street bounceHigher yields are weighing on European and Asian equities for a second day. Adding to the risk-off mood is news that China’s property giant, Evergrande, missed a bond payment, and a warning by ratings agency Moody’s that it may downgrade its rating on US debt if there is a government shutdown.

A credit downgrade could exacerbate the selloff in US Treasuries, which, apart from Fed tightening, are under pressure from the massive issuance in new debt.

Nevertheless, US stocks managed to stage a late rebound on Monday, with the S&P 500 adding 0.4% and the Nasdaq Composite gaining 0.5%.

The bounce back came about after Amazon said it will invest $4 billion in an AI startup, reviving the AI mania. Wall Street futures are in the red today, but a small relief rally is possible as Senate Republicans and Democrats are close to agreeing on a deal on a temporary spending measure to extend funding to the US government for six weeks. Although there’s a risk that the bill might not get through the House, it does represent a step in the right direction.

相關資產

最新新聞

免責聲明: XM Group提供線上交易平台的登入和執行服務,允許個人查看和/或使用網站所提供的內容,但不進行任何更改或擴展其服務和訪問權限,並受以下條款與條例約束:(i)條款與條例;(ii)風險提示;(iii)完全免責聲明。網站內部所提供的所有資訊,僅限於一般資訊用途。請注意,我們所有的線上交易平台內容並不構成,也不被視為進入金融市場交易的邀約或邀請 。金融市場交易會對您的投資帶來重大風險。

所有缐上交易平台所發佈的資料,僅適用於教育/資訊類用途,不包含也不應被視爲適用於金融、投資稅或交易相關諮詢和建議,或是交易價格紀錄,或是任何金融商品或非應邀途徑的金融相關優惠的交易邀約或邀請。

本網站的所有XM和第三方所提供的内容,包括意見、新聞、研究、分析、價格其他資訊和第三方網站鏈接,皆爲‘按原狀’,並作爲一般市場評論所提供,而非投資建議。請理解和接受,所有被歸類為投資研究範圍的相關内容,並非爲了促進投資研究獨立性,而根據法律要求所編寫,而是被視爲符合營銷傳播相關法律與法規所編寫的内容。請確保您已詳讀並完全理解我們的非獨立投資研究提示和風險提示資訊,相關詳情請點擊 這裡查看。