Disney to report higher earnings but will its shakeup plan impress? – Stock Markets

Walt Disney will unveil its fiscal Q4 earnings on Wednesday after the closing bell

Cost cutting and price hikes likely boosted earnings per share

But slowing revenue growth and downbeat guidance may weigh on the stock

Trouble at the top

Trouble at the topThe Walt Disney Company (Disney) has been undergoing a significant overhaul this year as returning CEO, Bob Iger, attempts to streamline the flagging business following several years of major acquisitions. There have been further changes at the very top of management too, with the latest being the announcement of a new chief financial officer.

Aside from the multiple challenges facing the business, the management is also battling the activist investor, Nelson Peltz, who just raised his stake in Disney and is demanding multiple seats on the board amid growing shareholder disgruntlement about the direction of the company. The latest earnings results will therefore be crucial in restoring investors’ trust in the management and the future of the company.

ESPN future under scrutiny as Disney+ strugglesEarlier in the year, the company split its ESPN sports network from the rest of the entertainment business, creating a third division, with parks, experiences and products being the other. ESPN has seen its revenue fall in recent quarters, so the move has raised speculation that Disney may be prepping to sell the unit. There is a counter argument against this, though, which is that ESPN remains a cash cow despite the recent revenue decline. Iger insists ESPN is not for sale and he is only looking for strategic partners. Apple is rumoured to be one of the companies interested in a possible stake.

The company’s popular streaming service, Disney+, hasn’t been doing so well either and continues to lose money. The streaming platform lost subscribers in each of the last three quarters after prices were raised last December. Some analysts, however, think that fiscal Q4 was a turning point, with net subscriber numbers growing slightly and this may have helped narrow the losses. The company is hoping that taking full ownership of Hulu – a sister streaming service – will bolster Disney+’s appeal by making content from Hulu available on both platforms.

Revenue boost from price hikesThe only real bright spot is likely to be the parks business where revenue has been surging. But even here the picture is not entirely positive as the record income is mostly being driven by higher prices rather than by growing visitor numbers. Still, the company is investing heavily in this segment and for the time being, the strategy appears to be paying off.

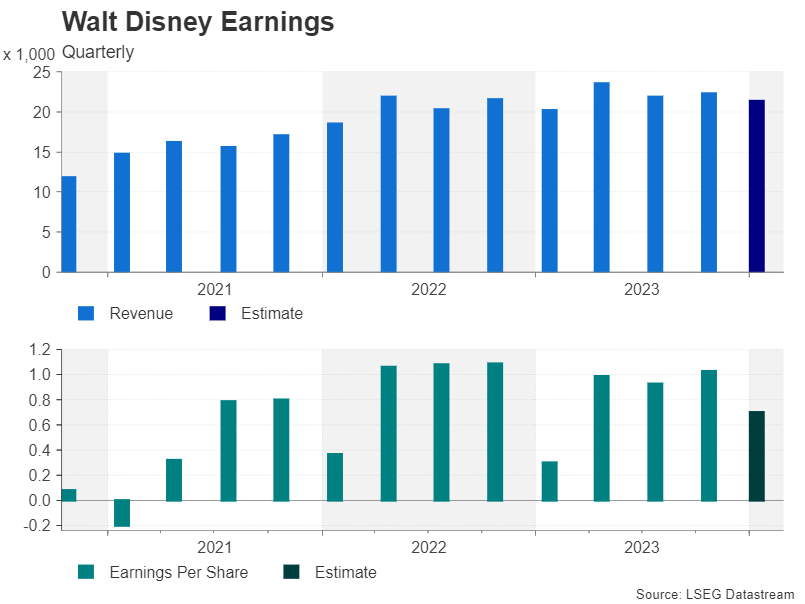

Total revenue in fiscal Q4 is expected to have reached $21.36 billion according to LSEG IBES data, up 6% from the same period a year ago but lower than the $22.33 billion reported in the prior quarter. Earnings per share (EPS), meanwhile, is anticipated at $0.70, representing a 133% jump from 12 months ago but down 32% from fiscal Q3.

All eyes on cost cutting progressWhilst there is plenty of room for disappointment as the company struggles to compete in the streaming arena and is in the midst of a major reorganisation, upside surprises are possible too as Iger implements his $5.5 billion cost-cutting drive, most of which will come from layoffs of up to 7,000 jobs.

That might go some way in explaining why analysts have maintained their ‘buy’ recommendation for the stock during this somewhat difficult period for the entertainment giant, even as the share price has fallen by about 3.3% in the year-to-date. Nevertheless, analysts are sticking to their triple digit price target. The median price target is currently $109.00 – about 30% higher than Monday’s closing price of $84.02 a share.

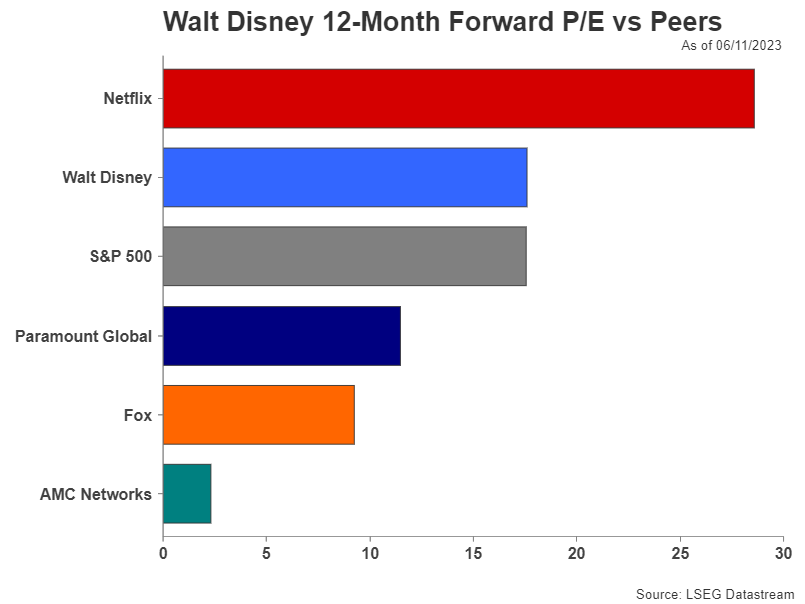

Is a rebound in the stock around the corner?On the positive side, the stock’s complete retracement of its post-pandemic rally when it hit an all-time high of $203.02 in March 2021 has made it more attractive from a valuation perspective. Disney’s forward price-to-earnings (P/E) ratio is below that of its main rival, Netflix, and equal to that of the S&P 500.

Looking ahead, the stock may have just formed a double bottom pattern and appears poised for a rebound. If the latest earnings results provide further evidence that Iger’s turnaround plan is bearing fruit, that may shore up support in the $80 region. However, in the short term, any relief rally may be capped by the 200-day moving average near the $92 level and investors will likely want to see sustained growth in streaming subscribers before taking the price back above $100.

免責聲明: XM Group提供線上交易平台的登入和執行服務,允許個人查看和/或使用網站所提供的內容,但不進行任何更改或擴展其服務和訪問權限,並受以下條款與條例約束:(i)條款與條例;(ii)風險提示;(iii)完全免責聲明。網站內部所提供的所有資訊,僅限於一般資訊用途。請注意,我們所有的線上交易平台內容並不構成,也不被視為進入金融市場交易的邀約或邀請 。金融市場交易會對您的投資帶來重大風險。

所有缐上交易平台所發佈的資料,僅適用於教育/資訊類用途,不包含也不應被視爲適用於金融、投資稅或交易相關諮詢和建議,或是交易價格紀錄,或是任何金融商品或非應邀途徑的金融相關優惠的交易邀約或邀請。

本網站的所有XM和第三方所提供的内容,包括意見、新聞、研究、分析、價格其他資訊和第三方網站鏈接,皆爲‘按原狀’,並作爲一般市場評論所提供,而非投資建議。請理解和接受,所有被歸類為投資研究範圍的相關内容,並非爲了促進投資研究獨立性,而根據法律要求所編寫,而是被視爲符合營銷傳播相關法律與法規所編寫的内容。請確保您已詳讀並完全理解我們的非獨立投資研究提示和風險提示資訊,相關詳情請點擊 這裡查看。