Week Ahead – Fed, ECB and BoJ decisions take center stage

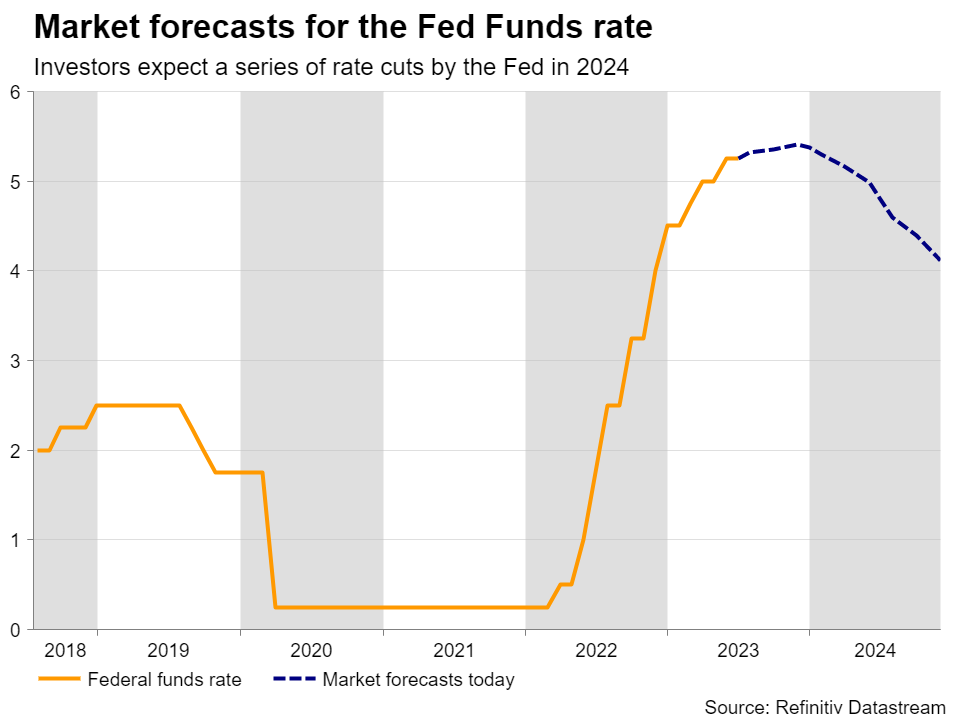

Following the dollar’s tumble last week due to the larger-than-expected slowdown in consumer and producer prices, market participants have become more convinced that the Fed will deliver only one more hike before it ends this tightening crusade, while they increased their Fed cut bets for next year.

The last time they met, Fed officials hit the pause button, but the decision had a hawkish flavor, with the ‘dot plot’ pointing to two additional rate increases and Fed Chair Powell pushing back on rate cut expectations by saying that any reductions are “a couple of years out.” Although investors were not convinced back then and neither when Powell testified before Congress, they began lifting their implied path after the Fed chief appeared at a panel discussion organized by the ECB in a hawkish suit.

But that was only until last week’s inflation data. Therefore, Wednesday’s FOMC decision may attract special attention as investors will be eager to get a clearer picture regarding the Fed’s future course of action. Given that a 25bps hike is nearly priced in, should it materialize, the spotlight is likely to turn to the accompanying statement for hints as to whether this was the last hike or whether rates could go higher.

With core inflation more than double the Fed’s 2% objective, Powell and co are unlikely to signal that this tightening crusade has ended. They may reiterate the view that the fight against inflation is not over, while at the press conference, Powell could once again push against rate cut expectations.

However, it remains to be seen whether another round of hawkish rhetoric will be enough to convince market participants enough to scale back their rate cut bets, as some of them may be holding the view that prior hikes could still work in bringing inflation further down in the coming months.

They may get an idea of where inflation may be headed from the prices subindices of the preliminary PMIs for July, due out on Monday, while Friday’s core PCE index could also affect their view after the gathering.

ECB to hike, focus to turn on Lagarde’s remarksUp until this week, the ECB was seen as much more hawkish than the Fed, expected to deliver two more quarter-point hikes this year and no cuts at all thereafter. That said, with several ECB policymakers arguing that a September hike is not a done deal, that picture has changed. Yes, there are still nearly two quarter-point hikes priced in, but traders now believe that interest rates in the Euro area will end next year 25 basis points below current levels. In other words, conditional upon two hikes being delivered this year, the market expects three rate cuts in 2024.

That pricing may be affected by the preliminary PMIs due out on Monday, and although a July hike seems a done deal, signs that the Eurozone is losing more economic steam could prompt speculation of a softer language in the statement accompanying the decision. The big question though may be whether ECB President Christine Lagarde has also softened her stance or whether she will appear in her hawkish suit again, dismissing the Eurozone’s economic slowdown and prioritizing getting inflation in check.

If Lagarde sticks to her guns the euro is likely to gain and perhaps extend those gains on Friday if preliminary CPI data suggests that inflation in Germany is stickier than previously thought.

BoJ seen on hold as Ueda pushes back on shift expectationsOn Friday, the central bank torch will be passed to the BoJ. After testing the psychological, intervention-debated, 145.00 level, dollar/yen came under strong selling interest, hitting a bottom at around 137.25, before rebounding again. The slide was not only the result of a weaker dollar but also a stronger yen as market participants may have started raising bets that the BoJ could tweak its policy at this gathering.

However, earlier this week, Governor Ueda reiterated his remarks that there is still some distance to achieve the 2% inflation target sustainably and stably, signaling determination to maintain ultra-loose policy for now. Traders have started scaling back their bets of an imminent policy shift, allowing dollar/yen to rebound. That said, even if the Bank does not act at this gathering, market participants may be interested in the new inflation projections as they may try to estimate the length of the distance Ueda is referring to.

If those projections are revised notably higher, the yen may gain, even if there is no policy shift now, as they will start speculating for a normalization step perhaps at the next gathering. The opposite may be true if Ueda and his colleagues place more emphasis on maintaining current policy due to inflation being mainly driven by expensive imports rather than domestic demand.

Australia CPIs, UK PMIs, and tech earningsElsewhere, Australia’s CPI data for Q2 are coming out on Wednesday. Just this Thursday, the employment data for June came in better than expected, increasing the probability for another hike at the RBA’s August meeting. Currently, investors are evenly split on whether the Bank should hike or not, and the CPIs have the potential to tip the scale.

For the pound, the week starts and ends on Monday with the preliminary PMIs for July. The British currency suffered this week on the back of a larger-than-expected cooling in UK inflation for July, prompting market participants to ditch bets of another double hike in August and take off the table some of the basis points worth of hikes they were expecting thereafter. So, should the surveys reveal that prices charged during July rose at a slower pace than in June, the pound could suffer more as traders reexamine the ultra-hawkish BoE narrative.

Finally, on the earnings front, we get the results from tech giants Alphabet, Microsoft, Meta and Amazon.

สินทรัพย์ที่เกี่ยวข้อง

ข่าวล่าสุด

ข้อความสงวนสิทธิ์: บริษัทในเครือ XM Group มีการให้บริการดำเนินคำสั่งและการเข้าถึงแพลตฟอร์มซื้อขายออนไลน์ของเรา ซึ่งช่วยให้บุคคลสามารถดู และ/หรือใช้ข้อมูลที่มีอยู่บนหรือผ่านทางเว็บไซต์ ซึ่งไม่ได้มีการเปลี่ยนแปลงหรือขยายความจากสิ่งนี้ อีกทั้งการเข้าถึงดังกล่าวจะอยู่ภายใต้: (i) เงื่อนไขและข้อตกลง; (ii) คำเตือนเกี่ยวกับความเสี่ยง; และ (iii) ข้อความสงวนสิทธิ์ฉบับเต็ม ดังนั้นข้อมูลดังกล่าวจึงเป็นเพียงแค่ข้อมูลทั่วไปเท่านั้น นอกจากนี้โปรดทราบว่าข้อมูลต่างๆ บนแพลตฟอร์มซื้อขายออนไลน์ของเราไม่ได้มีการเชื้อเชิญหรือถือเป็นข้อเสนอให้ทำธุรกรรมใดๆ บนตลาดการเงิน และการซื้อขายบนตลาดการเงินใดๆ มีความเสี่ยงในระดับสูงกับเงินทุนของคุณ

เนื้อหาทั้งหมดที่ถูกเผยแพร่อยู่บนแพลตฟอร์มเทรดออนไลน์ของเรามีวัตถุประสงค์เพื่อให้ข้อมูล/ความรู้เท่านั้นและไม่มี – และไม่ควรถือว่ามี – คำแนะนำด้านการเงิน, ภาษีการลงทุน, หรือการเทรด หรือข้อมูลราคาย้อนหลัง, หรือข้อเสนอ, หรือการเชื้อเชิญให้ทำธุรกรรมใดๆ เกี่ยวกับตราสารทางการเงินหรือโปรโมชั่นทางการเงินสำหรับท่าน

เนื้อหาของบุคคลที่สามใดๆ รวมถึงเนื้อหาที่ถูกจัดเตรียมขึ้นโดย XM เช่น ข้อคิดเห็น, ข่าวสาร, บทวิเคราะห์, ราคา, ข้อมูลอื่นๆ หรือลิงก์ไปยังเว็บไซต์ของบุคคลที่สามที่อยู่ในเว็บไซต์นี้ถูกจัดทำขึ้น “ตามที่เป็น” ซึ่งเป็นการแสดงความคิดเห็นเกี่ยวกับตลาดโดยทั่วไปและไม่ถือเป็นคำแนะนำด้านการลงทุน เนื่องจากเนื้อหาเหล่านี้ถือเป็นบทวิจัยด้านการลงทุน ท่านจะต้องทราบและยอมรับว่า เนื้อหาเหล่านี้ไม่ได้มีวัตถุประสงค์และไม่ได้มีการถูกจัดเตรียมขึ้นตามข้อกำหนดทางด้านกฎหมายที่ถูกออกแบบขึ้นมาเพื่อส่งเสริมการวิจัยด้านการลงทุนที่เป็นอิสระ ดังนั้นเนื้อหาเหล่านี้ถือเป็นการสื่อสารทางการตลาดภายใต้กฎหมายและกฎระเบียบที่เกี่ยวข้อง โปรดอ่านและทำความเข้าใจประกาศเกี่ยวกับบทวิจัยด้านการลงทุนที่ไม่ได้มีความเป็นอิสระและคำเตือนเกี่ยวกับความเสี่ยงซึ่งมีความเกี่ยวข้องกับข้อมูลต่างๆ ดังที่ได้กล่าวไปแล้ว โดยท่านสามารถดูได้ ที่นี่