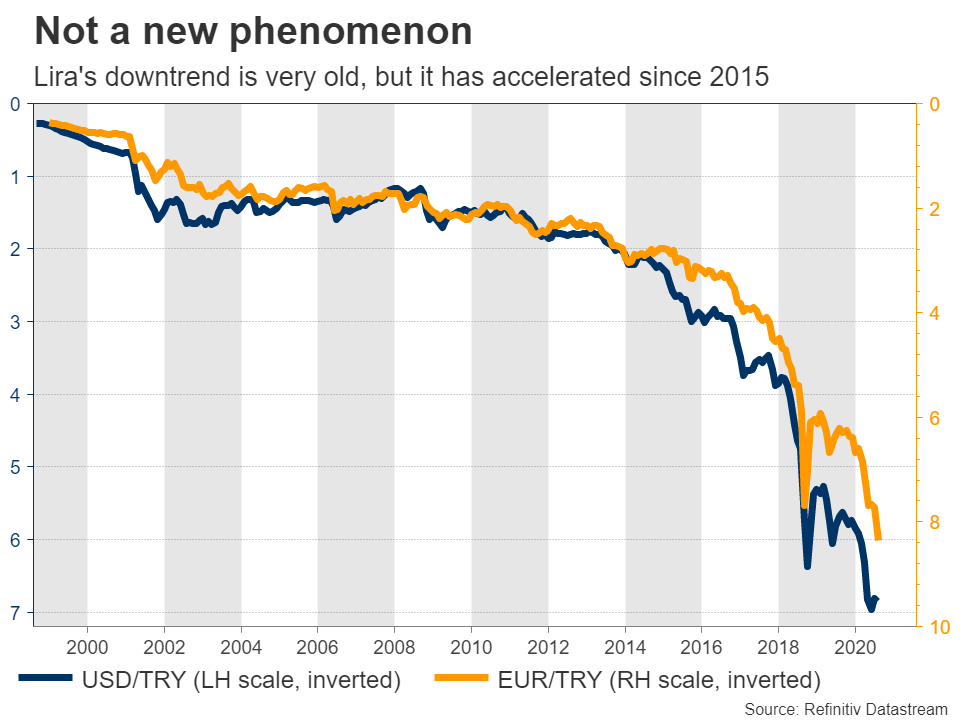

Turkish lira: Another crisis unfolds

The past few years have been a difficult period for the Turkish currency, and things have unfortunately not calmed down in 2020. The lira hit an all-time low against the dollar in May, then against the euro in July, and then plunged to fresh record lows against both currencies this week.

This is not a new phenomenon. The lira has been in a broader downtrend for two decades now, though the pace of the currency’s collapse has accelerated in recent years as a cocktail of worrisome economic developments has caused capital to flee the country.

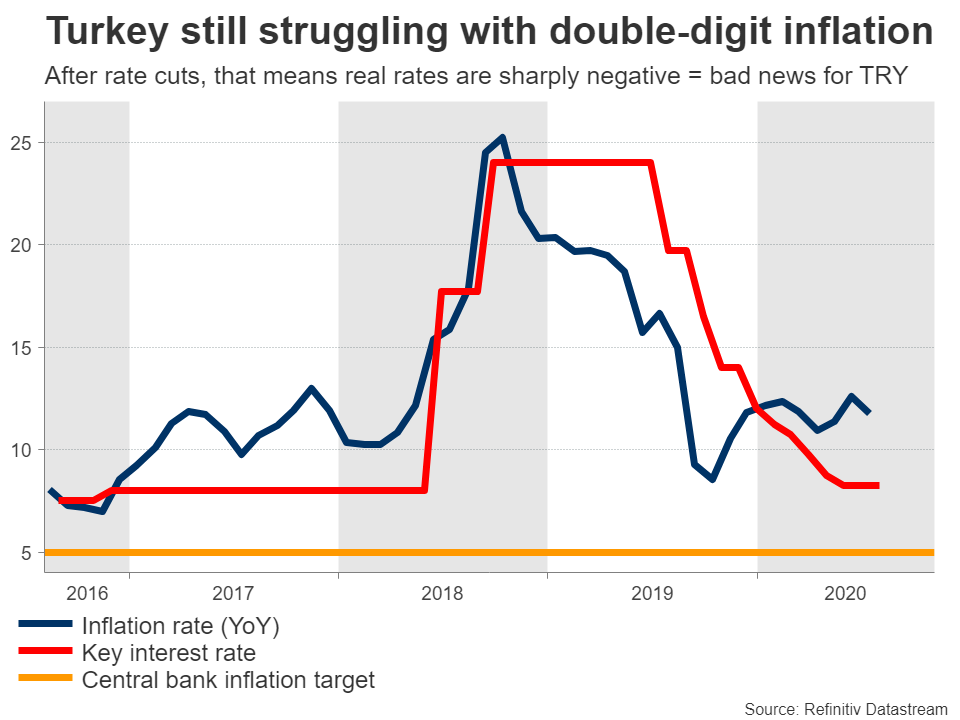

Inflation soars, deficits widenThe main issue that has devastated the lira is double-digit inflation. High inflation erodes purchasing power and is anathema for currencies. Even after the pandemic, when inflation would naturally sink because of lower demand, Turkey’s inflation rate still clocked in at almost 12% in July – more than double the 5% targeted by the central bank.

To make matters worse, Turkey also runs a chronic current account deficit. That basically means the nation is a net borrower, importing more than it exports and relying on capital flows from abroad to finance the difference. The problem is that if these capital flows dry up or foreign investors decide to withdraw their investments, this begins to exert massive downward pressure on the currency.

Additionally, both the government and the private sector have high levels of debt in foreign currencies, which become much harder to pay back with a depreciating lira.

Central bank prioritizes growthIn a situation like this, the central bank would typically raise interest rates to rein in inflation, stabilize the current account deficit by attracting more foreign capital, and defend the currency. Of course, this is a painful process. Higher rates would slow down borrowing, hit demand, hurt economic growth, and even risk an increase in unemployment.

Even though the central bank did raise rates dramatically in 2018 to avert a full-blown currency crisis, it has since lowered them again by more than 15 percentage points, to 8.25% currently. That’s a tricky endeavor. It’s basically a gamble, where policymakers are trying to boost growth at all costs, by incentivizing another borrowing boom and allowing inflation to soar.

The gamble is whether their FX reserves will be sufficient to keep the lira from collapsing while they attempt to boost growth. Foreign reserves naturally run out when you are constantly trying to defend a currency, and Turkey has been burning through its own at a furious pace.

What’s the point of all this? Since inflation exceeds interest rates so dramatically, Turkey has some of the most negative real interest rates globally, which is really bad news for a currency over time. Why would foreign investors put capital into a Turkish bank, where they might earn 9% interest, when inflation is running at 12%? That implies a loss of 3% per year, which is unlikely to attract foreign capital, and if anything, might push investors to leave Turkey altogether.

What can be done?In the short term, there are two methods that could halt the lira’s slide, but admittedly, neither is likely to be implemented.

The first would be to raise interest rates again. But the central bank doesn’t want to do that. We are in the middle of a crisis, which will naturally hurt the economy, so their main priority is to stimulate growth at all costs, even if that means higher inflation and a weaker currency. Plus, there may be some political pressure involved, as President Erdogan has long been a critic of high interest rates, even describing them as “the mother and father of all evil”.

The second would be introducing strict capital controls. It looks bad, as it tarnishes an economy’s credibility and might incite panic among foreign investors, but if you are trying to stop a currency crisis, it works. That option however has been repeatedly ruled out by the nation’s finance minister, who is also President Erdogan’s son-in-law.

What’s most likely then?In a nutshell, the lira will likely be allowed to depreciate. The central bank has already burned through most of its FX reserves, and lately, it has been spending reserves it has borrowed from local banks to support the currency. It has also resorted to more ‘questionable’ methods, such as making it more difficult to short the lira in the markets.

But these tools look exhausted. The lira wouldn’t be hitting new record lows against a US dollar that is weak itself, if they were effective. So it’s either rate hikes, capital controls, or allowing the currency to depreciate further. A currency can’t resist economic gravity for long.

At some point, the central bank will probably be forced to raise rates. But for that to happen, the lira probably has to experience more pain first, leaving policymakers no choice.

Beyond the lira – mind European banks and the euroIn the bigger picture, if Turkey indeed faces a new currency crisis, that could also be bad news for the euro. European banks are exposed to Turkey, much more than American banks, and if the situation worsens they might have to take losses on those operations.

The European banking system is still tormented by the legacy of the euro crisis, and with the pandemic likely to cause another spike in non-performing loans, any Turkey-related worries may spill over into the euro. Of course, this is a minor factor, but it may play some role in slowing down the recent uptrend in euro/dollar.ข่าวล่าสุด

ข้อความสงวนสิทธิ์: บริษัทในเครือ XM Group มีการให้บริการดำเนินคำสั่งและการเข้าถึงแพลตฟอร์มซื้อขายออนไลน์ของเรา ซึ่งช่วยให้บุคคลสามารถดู และ/หรือใช้ข้อมูลที่มีอยู่บนหรือผ่านทางเว็บไซต์ ซึ่งไม่ได้มีการเปลี่ยนแปลงหรือขยายความจากสิ่งนี้ อีกทั้งการเข้าถึงดังกล่าวจะอยู่ภายใต้: (i) เงื่อนไขและข้อตกลง; (ii) คำเตือนเกี่ยวกับความเสี่ยง; และ (iii) ข้อความสงวนสิทธิ์ฉบับเต็ม ดังนั้นข้อมูลดังกล่าวจึงเป็นเพียงแค่ข้อมูลทั่วไปเท่านั้น นอกจากนี้โปรดทราบว่าข้อมูลต่างๆ บนแพลตฟอร์มซื้อขายออนไลน์ของเราไม่ได้มีการเชื้อเชิญหรือถือเป็นข้อเสนอให้ทำธุรกรรมใดๆ บนตลาดการเงิน และการซื้อขายบนตลาดการเงินใดๆ มีความเสี่ยงในระดับสูงกับเงินทุนของคุณ

เนื้อหาทั้งหมดที่ถูกเผยแพร่อยู่บนแพลตฟอร์มเทรดออนไลน์ของเรามีวัตถุประสงค์เพื่อให้ข้อมูล/ความรู้เท่านั้นและไม่มี – และไม่ควรถือว่ามี – คำแนะนำด้านการเงิน, ภาษีการลงทุน, หรือการเทรด หรือข้อมูลราคาย้อนหลัง, หรือข้อเสนอ, หรือการเชื้อเชิญให้ทำธุรกรรมใดๆ เกี่ยวกับตราสารทางการเงินหรือโปรโมชั่นทางการเงินสำหรับท่าน

เนื้อหาของบุคคลที่สามใดๆ รวมถึงเนื้อหาที่ถูกจัดเตรียมขึ้นโดย XM เช่น ข้อคิดเห็น, ข่าวสาร, บทวิเคราะห์, ราคา, ข้อมูลอื่นๆ หรือลิงก์ไปยังเว็บไซต์ของบุคคลที่สามที่อยู่ในเว็บไซต์นี้ถูกจัดทำขึ้น “ตามที่เป็น” ซึ่งเป็นการแสดงความคิดเห็นเกี่ยวกับตลาดโดยทั่วไปและไม่ถือเป็นคำแนะนำด้านการลงทุน เนื่องจากเนื้อหาเหล่านี้ถือเป็นบทวิจัยด้านการลงทุน ท่านจะต้องทราบและยอมรับว่า เนื้อหาเหล่านี้ไม่ได้มีวัตถุประสงค์และไม่ได้มีการถูกจัดเตรียมขึ้นตามข้อกำหนดทางด้านกฎหมายที่ถูกออกแบบขึ้นมาเพื่อส่งเสริมการวิจัยด้านการลงทุนที่เป็นอิสระ ดังนั้นเนื้อหาเหล่านี้ถือเป็นการสื่อสารทางการตลาดภายใต้กฎหมายและกฎระเบียบที่เกี่ยวข้อง โปรดอ่านและทำความเข้าใจประกาศเกี่ยวกับบทวิจัยด้านการลงทุนที่ไม่ได้มีความเป็นอิสระและคำเตือนเกี่ยวกับความเสี่ยงซึ่งมีความเกี่ยวข้องกับข้อมูลต่างๆ ดังที่ได้กล่าวไปแล้ว โดยท่านสามารถดูได้ ที่นี่