Market Comment – Stocks pummelled as yields and oil extend gains, dollar firms ahead of Powell

Bond yields continue to rise as surging oil prices add to higher for longer case

Stocks pressured as higher yields start to bite, earnings disappoint

Oil and gold ease from highs but eye more gains amid ongoing tensions in Mideast

Markets unsettled by geopolitics as oil rallies

Markets unsettled by geopolitics as oil ralliesStock markets fell deeper into the red on Thursday after widespread losses yesterday on the back of the tense mood in the Middle East that has fanned the rally in crude oil, which in turn is pushing up soaring bond yields even higher.

President Biden’s unscheduled visit to Israel on Wednesday was marred by the bombing of a hospital in Gaza that prompted Arab leaders to cancel a planned summit with the US President. But although a ceasefire looks even further off than it did prior to this week’s developments, there was some relief that Biden is stepping up efforts to get aid into the Gaza strip as well as urging Israel to proceed cautiously amid preparations for a possible ground offensive.

The ongoing risk of an escalation of the conflict that could draw in other regional powers such as oil-rich Iran drove oil futures up more than 3% at one point. A much bigger-than-expected drop in weekly US crude inventories added to the upside pressure.

Both WTI and Brent crude futures later erased some of those gains to close around 1.8% higher but gold maintained a sturdier uptrend. The precious metal has jumped more than 6% since the outbreak of violence in Israel on October 7 and it is trading higher today to test the $1,950/oz level.

Powell speech awaited as 10-year yield approaches 5.0%Demand for safe havens failed to put a cap on bond yields although yesterday’s auction for 20-year Treasuries did attract plenty of buyers. Nevertheless, concerns not just about the rise in oil prices but also about the recent run of solid economic indicators out of the United States has added fuel to the rally in Treasury yields.

The yield on 10-year Treasury notes reached a fresh 16-year high of 4.98% today, while the 30-year yield breached the 5.0% threshold for the second time in two weeks.

Fed officials have been questioning the need for additional rate hikes lately, arguing that the tighter financial conditions stemming from higher yields have done some of the work for them. But after the hattrick of data beats from the nonfarm payrolls, CPI and retail sales reports, investors have begun to price in a higher probability of one final 25-bps rate hike.

Speaking in London yesterday, Fed Governor Christopher Waller signalled a pause in November, saying he wants to “wait, watch and see”, but he did not rule out “more action” at a later point if needed. All eyes today, though, will be on the Fed Chair as Powell will be speaking at the Economic Club of New York (16:00 GMT) before the blackout period begins at the weekend.

Equities face growing headwindsStocks took fright from the relentless upward march in bond yields, with all three of Wall Street’s leading indices closing lower on Wednesday. Even if the Fed decides against raising rates further, the ‘higher for longer’ reality is slowly sinking in for investors, with 2024 rate cut expectations pared back sharply this week.

After starting the week on a positive note following a strong set of bank earnings on Friday, stocks took a dive yesterday as rising borrowing costs took the steam out of the latest bounce, while the Israel-Gaza conflict further muddied the outlook.

Morgan Stanley was a major drag as the stock plunged 6.8% after the bank reported a 9% fall in its Q3 earnings. Tesla’s results also disappointed and its stock looks set to extend yesterday’s 4.8% drop, which came even before the earnings were announced.

However, Netflix could spread some joy today as its stock surged by more than 10% in after-hours trading when it reported impressive revenue and subscriber numbers.

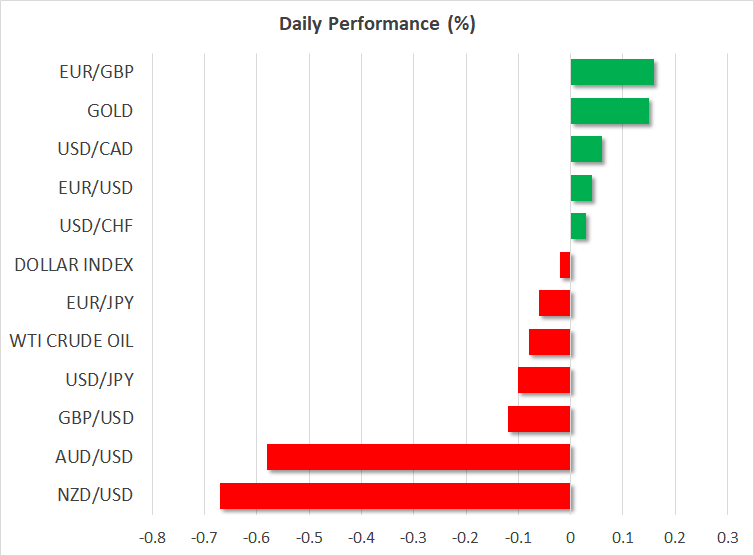

Dollar’s uninspiring performanceThe US dollar was marginally firmer on Thursday, failing to significantly capitalize on the spike in Treasury yields as well as the flight to safety. The dollar index remains below its October 3 peak, suggesting that FX markets are adhering to the shift in Fed rhetoric differently than bond markets.

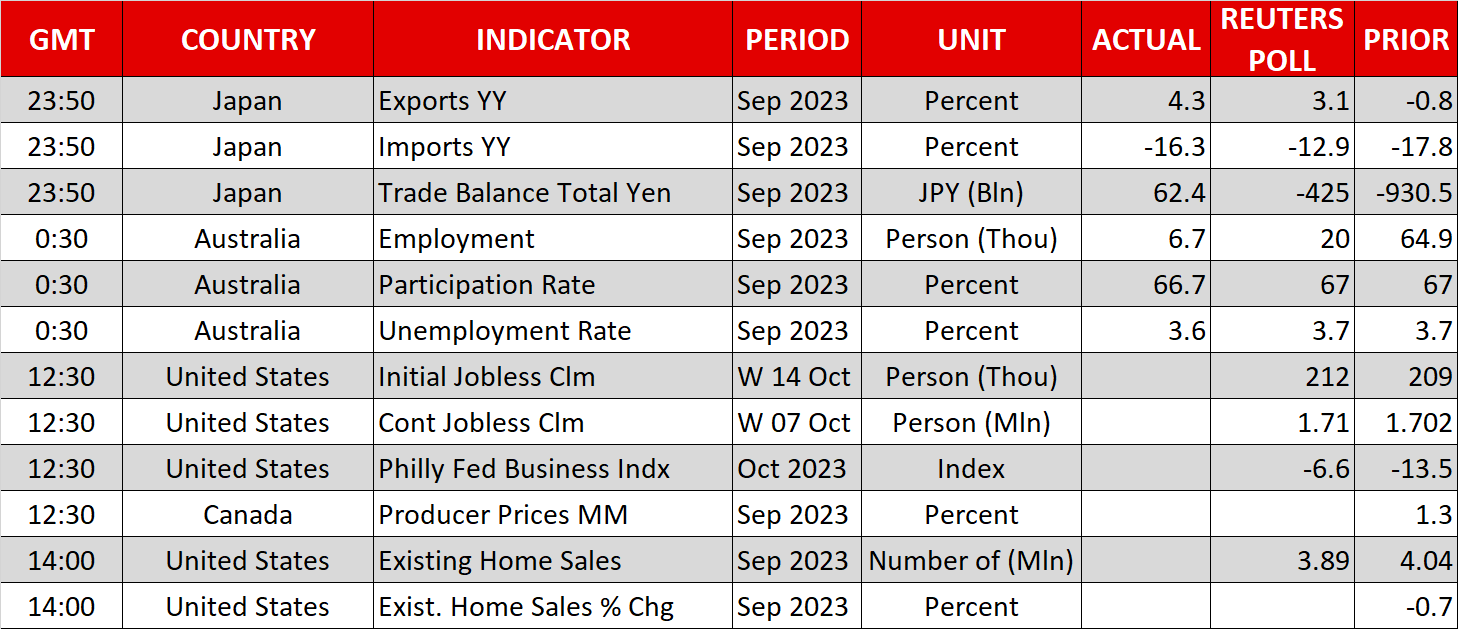

The pound is trading at a two-week low as yesterday’s hotter-than-expected UK CPI data didn't alter rate hike bets much for the Bank of England. The Australian dollar, meanwhile, is one of the worst performers today, weighed by a smaller-than-forecast increase in Australian employment in September, which slightly dented expectations of the RBA raising rates again.

สินทรัพย์ที่เกี่ยวข้อง

ข่าวล่าสุด

ข้อความสงวนสิทธิ์: บริษัทในเครือ XM Group มีการให้บริการดำเนินคำสั่งและการเข้าถึงแพลตฟอร์มซื้อขายออนไลน์ของเรา ซึ่งช่วยให้บุคคลสามารถดู และ/หรือใช้ข้อมูลที่มีอยู่บนหรือผ่านทางเว็บไซต์ ซึ่งไม่ได้มีการเปลี่ยนแปลงหรือขยายความจากสิ่งนี้ อีกทั้งการเข้าถึงดังกล่าวจะอยู่ภายใต้: (i) เงื่อนไขและข้อตกลง; (ii) คำเตือนเกี่ยวกับความเสี่ยง; และ (iii) ข้อความสงวนสิทธิ์ฉบับเต็ม ดังนั้นข้อมูลดังกล่าวจึงเป็นเพียงแค่ข้อมูลทั่วไปเท่านั้น นอกจากนี้โปรดทราบว่าข้อมูลต่างๆ บนแพลตฟอร์มซื้อขายออนไลน์ของเราไม่ได้มีการเชื้อเชิญหรือถือเป็นข้อเสนอให้ทำธุรกรรมใดๆ บนตลาดการเงิน และการซื้อขายบนตลาดการเงินใดๆ มีความเสี่ยงในระดับสูงกับเงินทุนของคุณ

เนื้อหาทั้งหมดที่ถูกเผยแพร่อยู่บนแพลตฟอร์มเทรดออนไลน์ของเรามีวัตถุประสงค์เพื่อให้ข้อมูล/ความรู้เท่านั้นและไม่มี – และไม่ควรถือว่ามี – คำแนะนำด้านการเงิน, ภาษีการลงทุน, หรือการเทรด หรือข้อมูลราคาย้อนหลัง, หรือข้อเสนอ, หรือการเชื้อเชิญให้ทำธุรกรรมใดๆ เกี่ยวกับตราสารทางการเงินหรือโปรโมชั่นทางการเงินสำหรับท่าน

เนื้อหาของบุคคลที่สามใดๆ รวมถึงเนื้อหาที่ถูกจัดเตรียมขึ้นโดย XM เช่น ข้อคิดเห็น, ข่าวสาร, บทวิเคราะห์, ราคา, ข้อมูลอื่นๆ หรือลิงก์ไปยังเว็บไซต์ของบุคคลที่สามที่อยู่ในเว็บไซต์นี้ถูกจัดทำขึ้น “ตามที่เป็น” ซึ่งเป็นการแสดงความคิดเห็นเกี่ยวกับตลาดโดยทั่วไปและไม่ถือเป็นคำแนะนำด้านการลงทุน เนื่องจากเนื้อหาเหล่านี้ถือเป็นบทวิจัยด้านการลงทุน ท่านจะต้องทราบและยอมรับว่า เนื้อหาเหล่านี้ไม่ได้มีวัตถุประสงค์และไม่ได้มีการถูกจัดเตรียมขึ้นตามข้อกำหนดทางด้านกฎหมายที่ถูกออกแบบขึ้นมาเพื่อส่งเสริมการวิจัยด้านการลงทุนที่เป็นอิสระ ดังนั้นเนื้อหาเหล่านี้ถือเป็นการสื่อสารทางการตลาดภายใต้กฎหมายและกฎระเบียบที่เกี่ยวข้อง โปรดอ่านและทำความเข้าใจประกาศเกี่ยวกับบทวิจัยด้านการลงทุนที่ไม่ได้มีความเป็นอิสระและคำเตือนเกี่ยวกับความเสี่ยงซึ่งมีความเกี่ยวข้องกับข้อมูลต่างๆ ดังที่ได้กล่าวไปแล้ว โดยท่านสามารถดูได้ ที่นี่