Daily Market Comment – US CPI spikes again, dollar rallies; kiwi surges too after RBNZ ends QE

- US inflation jumps again, sending stocks spinning and dollar and yields flying

- RBNZ shocks by halting bond purchases, kiwi soars as August rate hike eyed

- Powell testimony in the spotlight as Fed’s patience put to the test

Markets settle down after another CPI shock

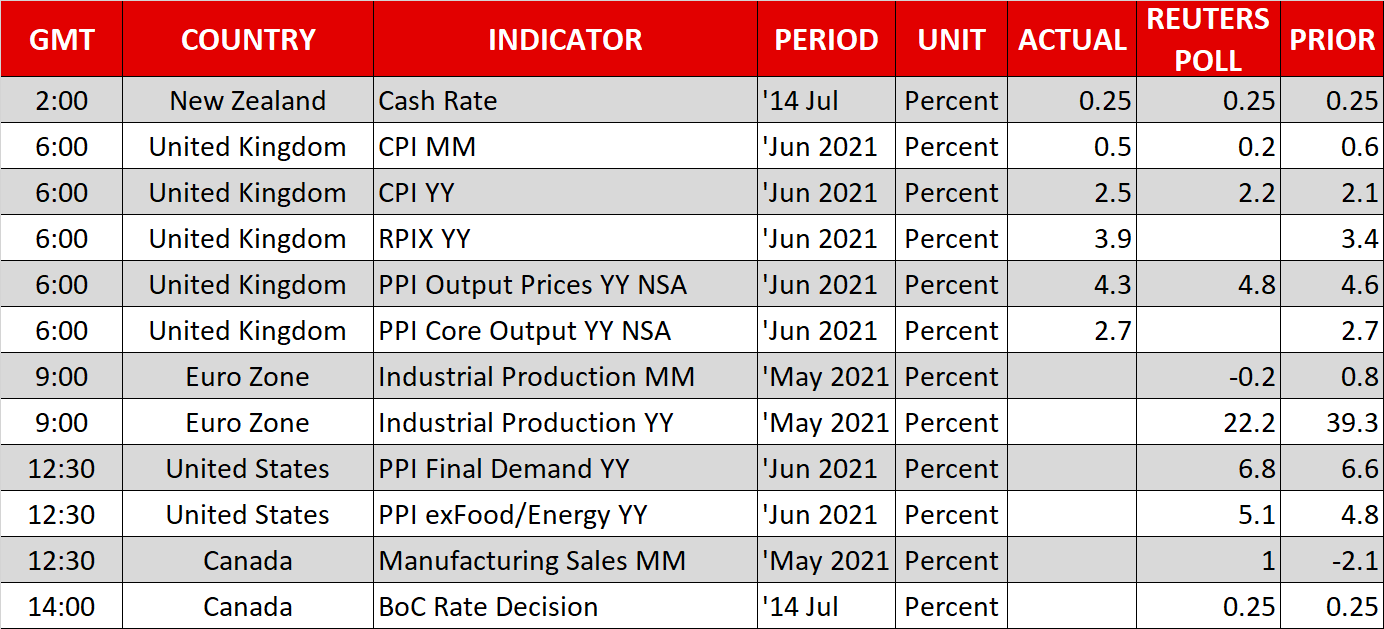

Markets settle down after another CPI shockAnnual inflation in the United States hit a fresh 13-year high of 5.4% in June, surpassing the top estimates and casting doubt on the Fed’s narrative that this inflationary episode will be transitory. Month-on-month, both the headline and core CPI rates jumped by 0.9% - around double the expectations. While most of the evidence suggests the price hikes are still being driven by temporary factors, fuelled by the reopening of the economy such as demand for used vehicles and air travel, there are worries that some of the increases being seen in sectors like food and energy are not necessarily transitory.

Treasury yields on both the short- and long-end of the curve spiked after the data, boosting the US dollar. Although the yield curve initially flattened, as short-term yields rose more steeply, longer-dated yields soon caught up after a Treasury auction for 30-year bonds was met with weak demand.

Investors were likely spooked by the latest inflation data, which hurt sentiment ahead of the auction. However, bond markets are much calmer today, helping FX markets to stabilize as well.

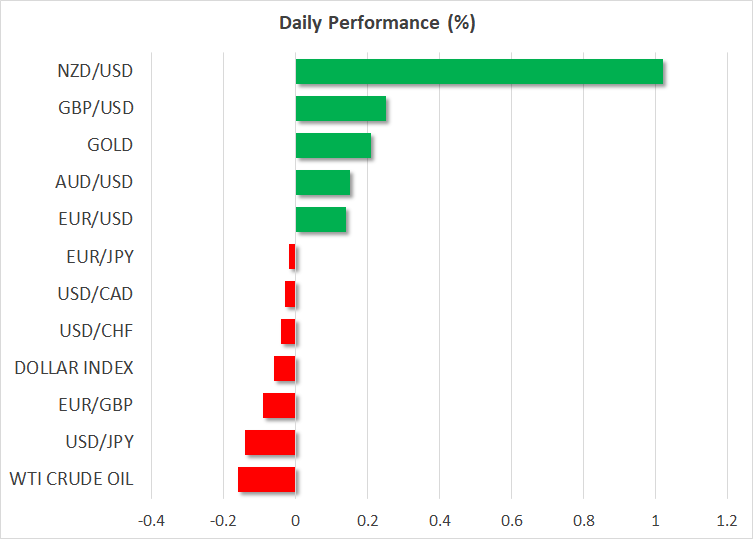

Dollar off highs but euro stays under pressureThe US dollar pared back some of its gains early on Wednesday following yesterday’s CPI-led surge. The dollar index is easing after failing to break above last week’s 3-month top of 92.845. Most majors are on a somewhat firmer footing versus the greenback today, but the euro is still looking very wobbly. Euro/dollar seems to have found near-term support at $1.1770. But with the European Central Bank getting ready to adjust its forward guidance, possibly to signal that it will tolerate inflation above 2%, the real test could soon be the $1.17 level, which was the March 31 trough.

The Australian dollar was struggling too after the lockdown in Sydney – Australia’s largest city – was extended by another two weeks. But the pound got a lift from the UK’s own CPI prints out today rising by more than expected, with the 12-month rate hitting 2.5% - the highest since August 2018.

Kiwi’s not-so-spectacular climb after RBNZ’s QE exitBut the winner so far on Wednesday is the New Zealand dollar, which skyrocketed after the Reserve Bank of New Zealand took markets by surprise by announcing an early end to its large scale asset purchase programme. The RBNZ will stop buying bonds on July 23.

The unexpected move prompted investors to price in an earlier rate hike than anticipated heading into the meeting. Markets had already brought forward rate hike expectations to November after the recent upbeat business confidence surveys, but consensus now seems to be forming for the August meeting.

Nevertheless, the kiwi’s 1% gain today would have been much bigger had it not been for USD strength. Even with the RBNZ being on track to become the first major central bank to hike rates in a post-pandemic world, the bullish dollar is making it difficult for the kiwi to secure a grip above the $0.70 handle.

Unimpressed by earnings, higher yields weigh on Wall StreetIn equity markets, the Dow Jones, S&P 500 and Nasdaq Composite all retreated from intra-day all-time highs after the US inflation data and subsequent rise in yields. But the positive momentum was weak to begin with and impressive earnings from JPMorgan and Goldman Sachs didn’t really spark much excitement.

Today’s earnings highlights will come from the Bank of America, Citigroup, Wells Fargo and Delta Air Lines. Nasdaq futures were last trading in slightly positive territory, with other futures still in the red, along with European indices.

Trading will likely remain subdued until Fed Chair Jerome Powell’s statement before the House Financial Services Committee in Congress for his semi-annual testimony. Powell will probably steer clear of flagging any timeline around tapering but undoubtedly, he will be quizzed about the latest inflation surge by lawmakers.

It might be a bit more difficult this time for Powell to tread as carefully around the inflation being transitory narrative. But in a worst case scenario, risk assets might be able to find some support from progress in infrastructure talks after Senate Democrats reached a deal on a $3.5 trillion investment plan that will likely be passed using the budget reconciliation process.

Finally, the Bank of Canada will also be in focus today, amid expectations that it will taper its own asset purchase programme as well.

ข่าวล่าสุด

ข้อความสงวนสิทธิ์: บริษัทในเครือ XM Group มีการให้บริการดำเนินคำสั่งและการเข้าถึงแพลตฟอร์มซื้อขายออนไลน์ของเรา ซึ่งช่วยให้บุคคลสามารถดู และ/หรือใช้ข้อมูลที่มีอยู่บนหรือผ่านทางเว็บไซต์ ซึ่งไม่ได้มีการเปลี่ยนแปลงหรือขยายความจากสิ่งนี้ อีกทั้งการเข้าถึงดังกล่าวจะอยู่ภายใต้: (i) เงื่อนไขและข้อตกลง; (ii) คำเตือนเกี่ยวกับความเสี่ยง; และ (iii) ข้อความสงวนสิทธิ์ฉบับเต็ม ดังนั้นข้อมูลดังกล่าวจึงเป็นเพียงแค่ข้อมูลทั่วไปเท่านั้น นอกจากนี้โปรดทราบว่าข้อมูลต่างๆ บนแพลตฟอร์มซื้อขายออนไลน์ของเราไม่ได้มีการเชื้อเชิญหรือถือเป็นข้อเสนอให้ทำธุรกรรมใดๆ บนตลาดการเงิน และการซื้อขายบนตลาดการเงินใดๆ มีความเสี่ยงในระดับสูงกับเงินทุนของคุณ

เนื้อหาทั้งหมดที่ถูกเผยแพร่อยู่บนแพลตฟอร์มเทรดออนไลน์ของเรามีวัตถุประสงค์เพื่อให้ข้อมูล/ความรู้เท่านั้นและไม่มี – และไม่ควรถือว่ามี – คำแนะนำด้านการเงิน, ภาษีการลงทุน, หรือการเทรด หรือข้อมูลราคาย้อนหลัง, หรือข้อเสนอ, หรือการเชื้อเชิญให้ทำธุรกรรมใดๆ เกี่ยวกับตราสารทางการเงินหรือโปรโมชั่นทางการเงินสำหรับท่าน

เนื้อหาของบุคคลที่สามใดๆ รวมถึงเนื้อหาที่ถูกจัดเตรียมขึ้นโดย XM เช่น ข้อคิดเห็น, ข่าวสาร, บทวิเคราะห์, ราคา, ข้อมูลอื่นๆ หรือลิงก์ไปยังเว็บไซต์ของบุคคลที่สามที่อยู่ในเว็บไซต์นี้ถูกจัดทำขึ้น “ตามที่เป็น” ซึ่งเป็นการแสดงความคิดเห็นเกี่ยวกับตลาดโดยทั่วไปและไม่ถือเป็นคำแนะนำด้านการลงทุน เนื่องจากเนื้อหาเหล่านี้ถือเป็นบทวิจัยด้านการลงทุน ท่านจะต้องทราบและยอมรับว่า เนื้อหาเหล่านี้ไม่ได้มีวัตถุประสงค์และไม่ได้มีการถูกจัดเตรียมขึ้นตามข้อกำหนดทางด้านกฎหมายที่ถูกออกแบบขึ้นมาเพื่อส่งเสริมการวิจัยด้านการลงทุนที่เป็นอิสระ ดังนั้นเนื้อหาเหล่านี้ถือเป็นการสื่อสารทางการตลาดภายใต้กฎหมายและกฎระเบียบที่เกี่ยวข้อง โปรดอ่านและทำความเข้าใจประกาศเกี่ยวกับบทวิจัยด้านการลงทุนที่ไม่ได้มีความเป็นอิสระและคำเตือนเกี่ยวกับความเสี่ยงซึ่งมีความเกี่ยวข้องกับข้อมูลต่างๆ ดังที่ได้กล่าวไปแล้ว โดยท่านสามารถดูได้ ที่นี่