Market Comment – Better-than-expected US PMIs help the dollar rebound

PMIs suggest the US economy entered Q4 on solid footing

The divergence between US/Eurozone outlooks weighs on euro/dollar

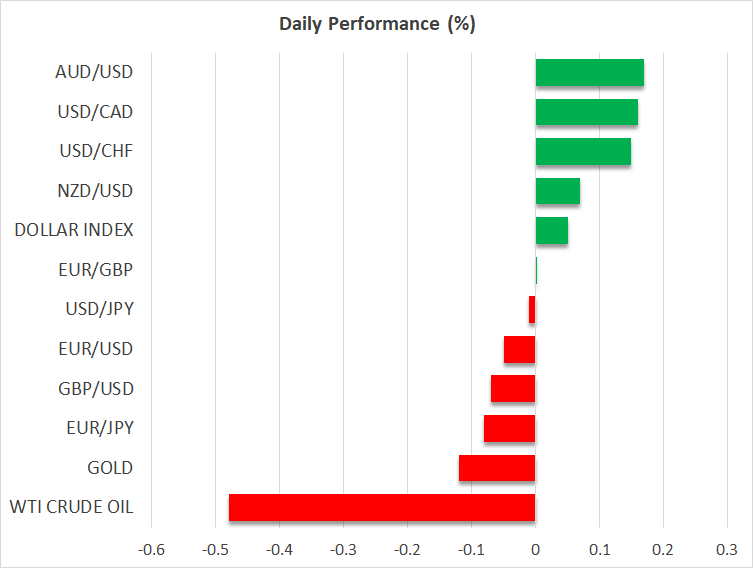

Aussie rallies on stickier inflation, yen pinned near 150-per-dollar mark

Wall Street pays attention to corporate earnings

Euro/dollar slides from near key resistance on PMI data

Euro/dollar slides from near key resistance on PMI dataAlthough the 10-year US Treasury yield held steady comfortably below the psychological zone of 5%, the US dollar was able to stage a comeback against most of its major counterparts as the flash US PMIs for October suggested that the world’s largest economy fared better than expected during the first month of the fourth quarter, with the manufacturing index escaping a contraction for the first time since April, and the composite index rising to 51.0 from 50.2.

This came in huge contrast to the Euro-area PMIs for the month that were released earlier in the day and painted an even uglier picture than they did in September. The divergence allowed euro/dollar bears to jump into the action from near the crossroads of the pair's 50-day moving average and the key resistance barrier of 1.0665, suggesting the latest recovery may have been just a corrective wave within the broader downtrend.

Dollar traders turn gaze to Q3 GDPThe slide may extend, and the pair could soon retest this month’s lows if Thursday’s data reveal astounding performance of the US economy in Q3. Expectations are for a solid 4.2% annualized growth rate, with the risks perhaps tilted to the upside as the Atlanta Fed GDPNow model estimates that the US economy may have grown 5.4% during that period.

The fact that Treasury yields did not track the dollar’s rebound may be an indication that investors were still reluctant to add to bets of another hike by the Fed after the better PMIs. Indeed, according to Fed funds futures, there is only a 40% chance for one final 25bps increase by January, while there are still around 80bps worth of rate reductions penciled in for next year. That said, the implied path could well be lifted, and rate cuts could be scaled back if upcoming data continues to point to a resilient US economy.

Aussie extends gains after CPIs, dollar/yen pinned near 150The aussie was among the currencies that outperformed the dollar yesterday, spiking even higher today after data showed that Australia’s inflation slowed by less than expected in Q3 and that the monthly y/y rate for September rose to 5.6% from 5.2%. This prompted investors to add to their bets of more hikes by the RBA, with the probability of another quarter-point increase at the November gathering rising to around 42%.

The yen attempted a recovery at some point yesterday, but the rebound in the dollar pinned the dollar/yen pair back near the highly monitored 150 territory, with traders biting their nails in anticipation of any signs of intervention by Japanese authorities. What could reveal whether officials are ready to act now or whether the level at which they feel comfortable intervening has shifted higher, may be a stellar US GDP print tomorrow that could force the pair to pierce through that psychological ceiling.

Wall Street ekes out gains, driven by upbeat earningsWall Street closed Tuesday in the green after upbeat forecasts from Verizon, Coca-Cola and other firms sparked optimism regarding the health of US businesses, encouraging investors to increase their risk exposure. The fact that the Fed’s implied rate path was not lifted after the better PMIs may have also helped Wall Street, which seems to be slowly shifting its attention away from the Middle East conflict.

After the closing bell, both Microsoft and Alphabet reported better-than-expected results, but the performance of their cloud services diverged. Microsoft’s Azure took off during the third quarter, but Alphabet’s cloud business saw its slowest growth in at least 11 quarters. After today’s close, it will be the turn of Meta Platforms to announce results.

In another sign that the financial world is turning its focus away from geopolitics, oil prices fell for the third straight day yesterday, perhaps as weak business surveys from the Eurozone and the UK weighed on the demand outlook.

Relaterade tillgångar

Senaste nytt

Ansvarsfriskrivning: XM Group-enheter tillhandahåller sin tjänst enbart för exekvering och tillgången till vår onlinehandelsplattform, som innebär att en person kan se och/eller använda tillgängligt innehåll på eller via webbplatsen, påverkar eller utökar inte detta, vilket inte heller varit avsikten. Denna tillgång och användning omfattas alltid av i) villkor, ii) riskvarningar och iii) fullständig ansvarsfriskrivning. Detta innehåll tillhandahålls därför uteslutande som allmän information. Var framför allt medveten om att innehållet på vår onlinehandelsplattform varken utgör en uppmaning eller ett erbjudande om att ingå några transaktioner på de finansiella marknaderna. Handel på alla finansiella marknader involverar en betydande risk för ditt kapital.

Allt material som publiceras på denna sida är enbart avsett för utbildnings- eller informationssyften och innehåller inte – och ska inte heller anses innehålla – rådgivning och rekommendationer om finansiella frågor, investeringsskatt eller handel, dokumentation av våra handelskurser eller ett erbjudande om, eller en uppmaning till, en transaktion i finansiella instrument eller oönskade finansiella erbjudanden som är riktade till dig.

Tredjepartsinnehåll, liksom innehåll framtaget av XM såsom synpunkter, nyheter, forskningsrön, analyser, kurser, andra uppgifter eller länkar till tredjepartssajter som återfinns på denna webbplats, tillhandahålls i befintligt skick, som allmän marknadskommentar, och utgör ingen investeringsrådgivning. I den mån som något innehåll tolkas som investeringsforskning måste det noteras och accepteras att innehållet varken har varit avsett som oberoende investeringsforskning eller har utarbetats i enlighet med de rättsliga kraven för att främja ett sådant syfte, och därför är att betrakta som marknadskommunikation enligt tillämpliga lagar och föreskrifter. Se till så att du har läst och förstått vårt meddelande om icke-oberoende investeringsforskning och riskvarning om ovannämnda information, som finns här.