With clouds gathering over the UK economy, what’s next for the pound?

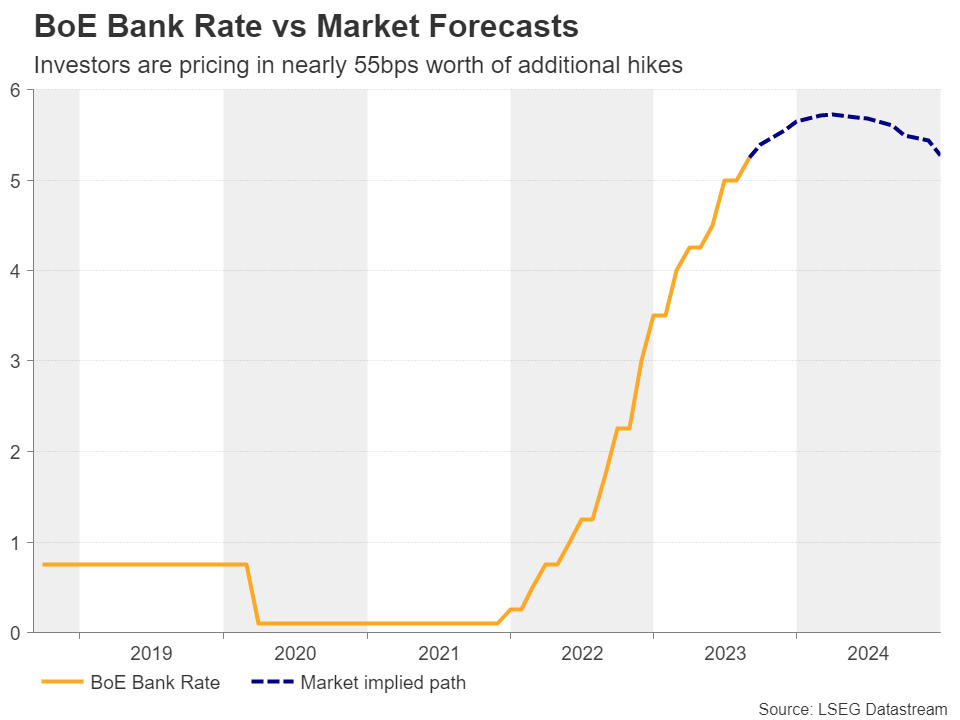

BoE policymakers decided to slow their tightening efforts at the August gathering, raising interest rates by 25bps, a smaller hike than July’s half-point increment, with Governor Bailey noting that he didn’t think there was a case for another 50bps hike. This hurt market expectations regarding the BoE’s future course of action and weighed on the pound, which was already struggling against its US counterpart due to data suggesting that the US remains in better shape than other major economies.

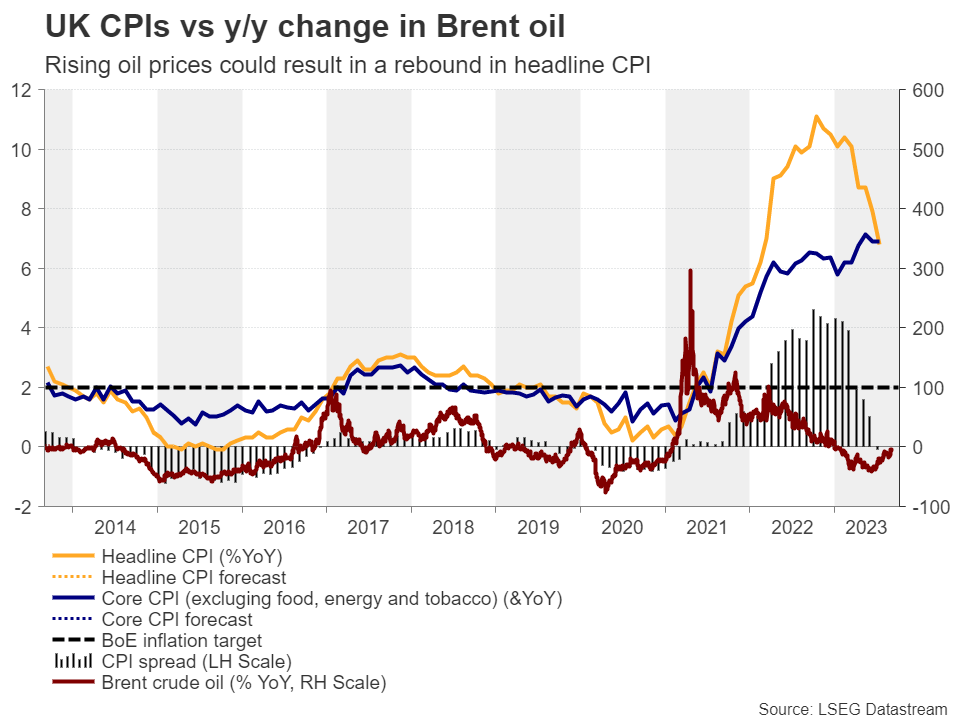

After the decision, GDP data showed that the economy grew somewhat instead of stagnating as the forecast suggested, with industrial and manufacturing production proving much stronger than expected in June. What’s more, despite the economy losing jobs and the unemployment rate rising to 4.2% in June from 4.0%, wages excluding bonuses accelerated by a full percentage point, adding to the already elevated inflation concerns. And as if all this was not enough, the CPI data revealed that the core CPI rate held steady at 6.9% y/y in July, suggesting that the decent slowdown in the headline print was due to volatile items like food and energy. With oil prices extending their recovery during August, a rebound in the headline rate in coming months cannot be ruled out.

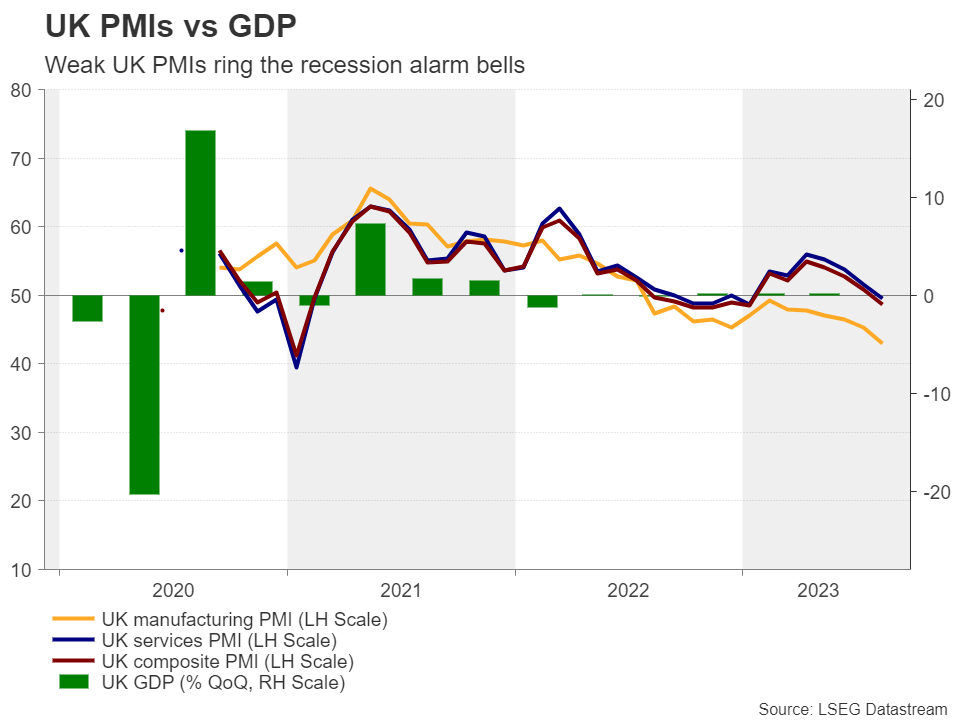

Ugly UK PMIs leave the BoE with a dilemma

Ugly UK PMIs leave the BoE with a dilemmaAll these numbers suggest that the BoE should stay the course and continue raising rates in order to bring ultra-sticky inflation to heel. However, the PMIs for August painted an ugly picture, with the composite PMI slipping into contractionary territory for the first time since January, heightening recession fears and leaving the BoE with a dilemma: continue raising rates and risk further damaging the economy or take a breather and risk allowing inflation to get out of control?

Just last week, remarks by Chief Economist Hew Pill revealed that he is in favor of keeping rates at current levels for longer rather than continuing to raise them and start cutting when they conclude the job is done. In other words, he may be willing to vote to keep interest rates on hold at the upcoming gathering on September 21. Still, the market is assigning an 83% probability for a 25bps hike that gathering, while it is fully pricing in another one by February.

This stands in a sharp contrast to the 55% probability seen for only another quarter point hike by the Fed and yet, the pound is on the back foot against the US dollar, confirming the narrative that traders are turning their gaze to growth dynamics. Despite the latest streak of data pointing to a slowdown in the US, the overall picture still suggests that the world’s largest economy is in a healthier state.

Like the September gatherings of all the major central banks, the BoE’s meeting on September 21 may prove pivotal with regards to the pound’s fate. Even if the Bank decides to press the hike button, if the decision is a close call and/or the decision has a dovish flavor, with hints that the peak of interest rates will be lower than the market currently anticipates, the pound is likely to continue to suffer. The opposite may be true if the Bank highlights the stickiness of inflation and appears ready to do whatever it takes to bring it to heel.

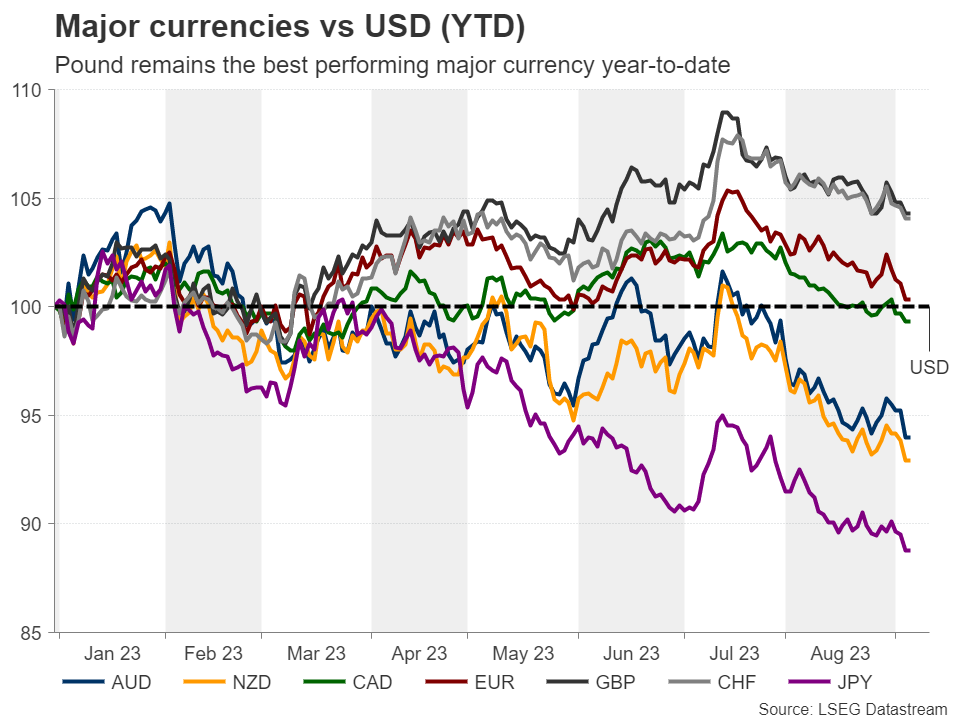

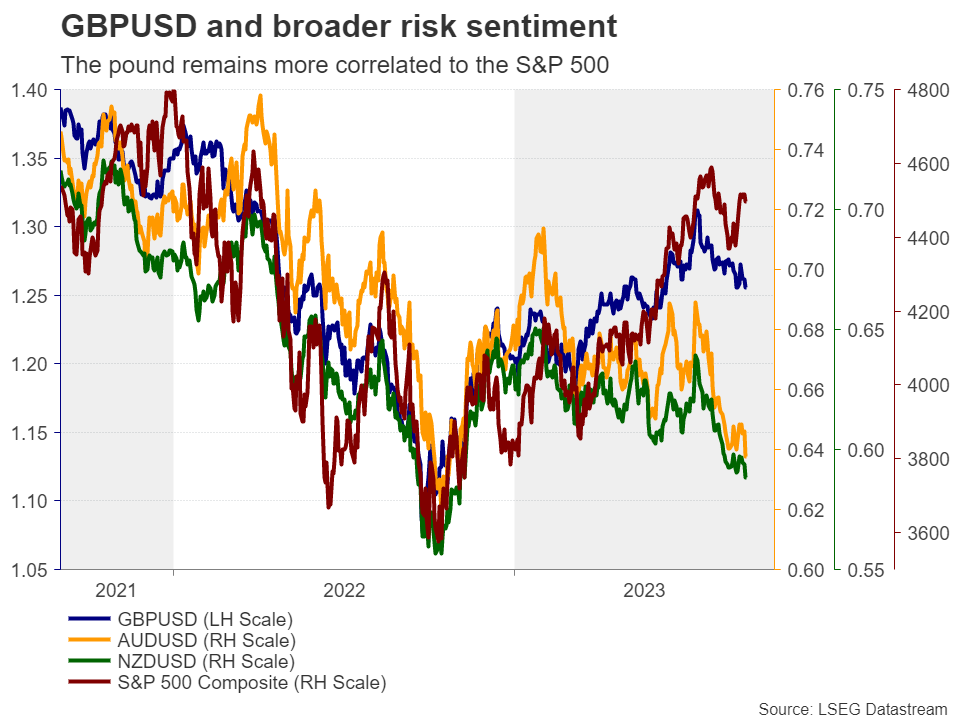

Equities have the pound’s backDespite its latest slide, the pound remains the best performing major currency – almost tied with the franc – since the turn of the year, and it is among the ones that lost the least ground since the US dollar staged a comeback. Apart from the fact that the BoE is still seen delivering more hikes than other major central banks, the pound may be also receiving support from its close correlation to the stock market.

As risk-linked currencies, the aussie and the kiwi also used to have a positive correlation with Wall Street, but due to Australia’s and New Zealand’s strong trade ties with China, these currencies are now better reflecting the concerns surrounding the performance of the world’s second largest economy. Having also in mind that both the RBA and the RBNZ seem to have concluded their tightening cycles, according to market pricing, the pound may be destined to continue outperforming those currencies. In other words, even if sterling suffers for a while longer against the US dollar, the pound/aussie and pound/kiwi pairs may be destined to continue drifting north.

Pound/kiwi pulled back after hitting the 2.1585 barrier, but it continues to trade above the uptrend line drawn from the low of February 2. This points to a positive outlook and should the bulls regain control, they could aim for another test at 2.1585, or the high of March 9, 2020, at 2.1680. A break higher could see scope for advances towards the psychological round number of 2.2000, also marked by the peak of May 26, 2016. For a bearish reversal to start being examined, the pair may need to drop below the key support zone of 2.0910.

Ativos relacionados

Últimas notícias

Isenção de Responsabilidade: As entidades do XM Group proporcionam serviço de apenas-execução e acesso à nossa plataforma online de negociação, permitindo a visualização e/ou uso do conteúdo disponível no website ou através deste, o que não se destina a alterar ou a expandir o supracitado. Tal acesso e uso estão sempre sujeitos a: (i) Termos e Condições; (ii) Avisos de Risco; e (iii) Termos de Responsabilidade. Este, é desta forma, fornecido como informação generalizada. Particularmente, por favor esteja ciente que os conteúdos da nossa plataforma online de negociação não constituem solicitação ou oferta para iniciar qualquer transação nos mercados financeiros. Negociar em qualquer mercado financeiro envolve um nível de risco significativo de perda do capital.

Todo o material publicado na nossa plataforma de negociação online tem apenas objetivos educacionais/informativos e não contém — e não deve ser considerado conter — conselhos e recomendações financeiras, de negociação ou fiscalidade de investimentos, registo de preços de negociação, oferta e solicitação de transação em qualquer instrumento financeiro ou promoção financeira não solicitada direcionadas a si.

Qual conteúdo obtido por uma terceira parte, assim como o conteúdo preparado pela XM, tais como, opiniões, pesquisa, análises, preços, outra informação ou links para websites de terceiras partes contidos neste website são prestados "no estado em que se encontram", como um comentário de mercado generalizado e não constitui conselho de investimento. Na medida em que qualquer conteúdo é construído como pesquisa de investimento, deve considerar e aceitar que este não tem como objetivo e nem foi preparado de acordo com os requisitos legais concebidos para promover a independência da pesquisa de investimento, desta forma, deve ser considerado material de marketing sob as leis e regulações relevantes. Por favor, certifique-se que leu e compreendeu a nossa Notificação sobre Pesquisa de Investimento não-independente e o Aviso de Risco, relativos à informação supracitada, os quais podem ser acedidos aqui.