Disney to report higher earnings but will its shakeup plan impress? – Stock Markets

Walt Disney will unveil its fiscal Q4 earnings on Wednesday after the closing bell

Cost cutting and price hikes likely boosted earnings per share

But slowing revenue growth and downbeat guidance may weigh on the stock

Trouble at the top

Trouble at the topThe Walt Disney Company (Disney) has been undergoing a significant overhaul this year as returning CEO, Bob Iger, attempts to streamline the flagging business following several years of major acquisitions. There have been further changes at the very top of management too, with the latest being the announcement of a new chief financial officer.

Aside from the multiple challenges facing the business, the management is also battling the activist investor, Nelson Peltz, who just raised his stake in Disney and is demanding multiple seats on the board amid growing shareholder disgruntlement about the direction of the company. The latest earnings results will therefore be crucial in restoring investors’ trust in the management and the future of the company.

ESPN future under scrutiny as Disney+ strugglesEarlier in the year, the company split its ESPN sports network from the rest of the entertainment business, creating a third division, with parks, experiences and products being the other. ESPN has seen its revenue fall in recent quarters, so the move has raised speculation that Disney may be prepping to sell the unit. There is a counter argument against this, though, which is that ESPN remains a cash cow despite the recent revenue decline. Iger insists ESPN is not for sale and he is only looking for strategic partners. Apple is rumoured to be one of the companies interested in a possible stake.

The company’s popular streaming service, Disney+, hasn’t been doing so well either and continues to lose money. The streaming platform lost subscribers in each of the last three quarters after prices were raised last December. Some analysts, however, think that fiscal Q4 was a turning point, with net subscriber numbers growing slightly and this may have helped narrow the losses. The company is hoping that taking full ownership of Hulu – a sister streaming service – will bolster Disney+’s appeal by making content from Hulu available on both platforms.

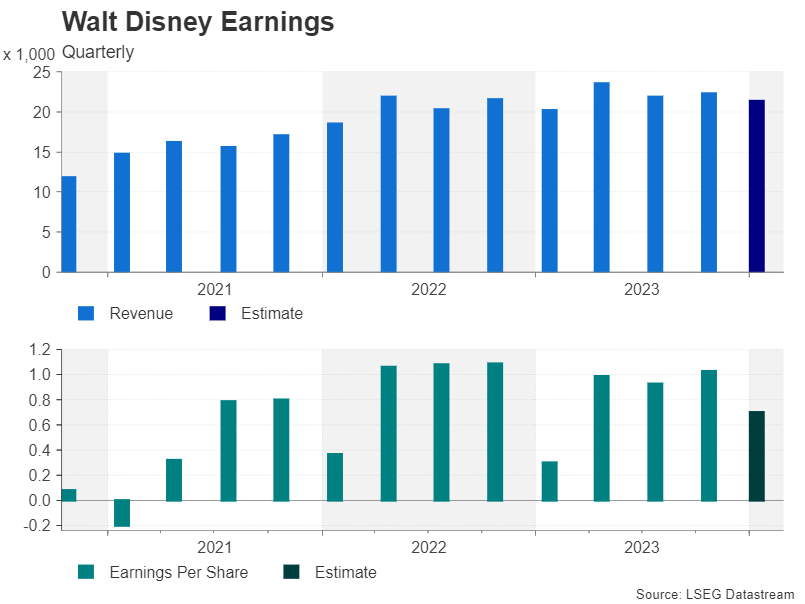

Revenue boost from price hikesThe only real bright spot is likely to be the parks business where revenue has been surging. But even here the picture is not entirely positive as the record income is mostly being driven by higher prices rather than by growing visitor numbers. Still, the company is investing heavily in this segment and for the time being, the strategy appears to be paying off.

Total revenue in fiscal Q4 is expected to have reached $21.36 billion according to LSEG IBES data, up 6% from the same period a year ago but lower than the $22.33 billion reported in the prior quarter. Earnings per share (EPS), meanwhile, is anticipated at $0.70, representing a 133% jump from 12 months ago but down 32% from fiscal Q3.

All eyes on cost cutting progressWhilst there is plenty of room for disappointment as the company struggles to compete in the streaming arena and is in the midst of a major reorganisation, upside surprises are possible too as Iger implements his $5.5 billion cost-cutting drive, most of which will come from layoffs of up to 7,000 jobs.

That might go some way in explaining why analysts have maintained their ‘buy’ recommendation for the stock during this somewhat difficult period for the entertainment giant, even as the share price has fallen by about 3.3% in the year-to-date. Nevertheless, analysts are sticking to their triple digit price target. The median price target is currently $109.00 – about 30% higher than Monday’s closing price of $84.02 a share.

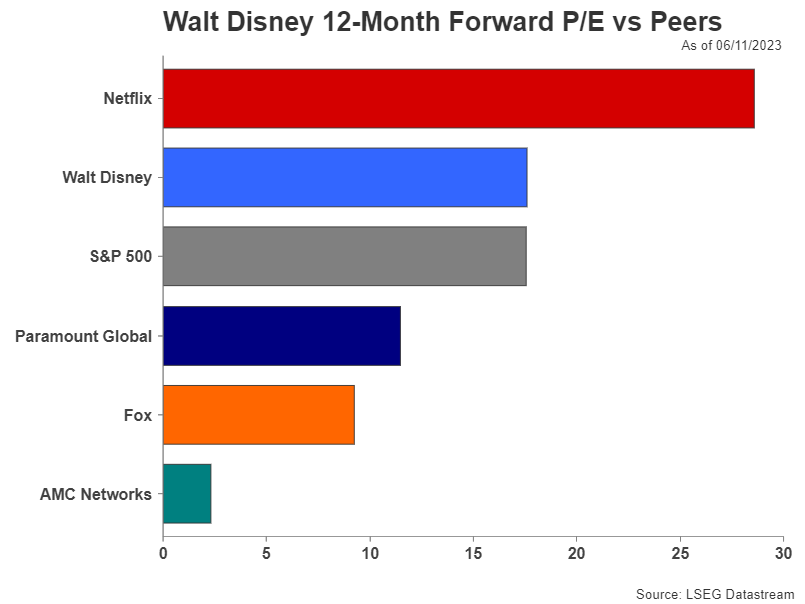

Is a rebound in the stock around the corner?On the positive side, the stock’s complete retracement of its post-pandemic rally when it hit an all-time high of $203.02 in March 2021 has made it more attractive from a valuation perspective. Disney’s forward price-to-earnings (P/E) ratio is below that of its main rival, Netflix, and equal to that of the S&P 500.

Looking ahead, the stock may have just formed a double bottom pattern and appears poised for a rebound. If the latest earnings results provide further evidence that Iger’s turnaround plan is bearing fruit, that may shore up support in the $80 region. However, in the short term, any relief rally may be capped by the 200-day moving average near the $92 level and investors will likely want to see sustained growth in streaming subscribers before taking the price back above $100.

Ativos relacionados

Últimas notícias

Isenção de Responsabilidade: As entidades do XM Group proporcionam serviço de apenas-execução e acesso à nossa plataforma online de negociação, permitindo a visualização e/ou uso do conteúdo disponível no website ou através deste, o que não se destina a alterar ou a expandir o supracitado. Tal acesso e uso estão sempre sujeitos a: (i) Termos e Condições; (ii) Avisos de Risco; e (iii) Termos de Responsabilidade. Este, é desta forma, fornecido como informação generalizada. Particularmente, por favor esteja ciente que os conteúdos da nossa plataforma online de negociação não constituem solicitação ou oferta para iniciar qualquer transação nos mercados financeiros. Negociar em qualquer mercado financeiro envolve um nível de risco significativo de perda do capital.

Todo o material publicado na nossa plataforma de negociação online tem apenas objetivos educacionais/informativos e não contém — e não deve ser considerado conter — conselhos e recomendações financeiras, de negociação ou fiscalidade de investimentos, registo de preços de negociação, oferta e solicitação de transação em qualquer instrumento financeiro ou promoção financeira não solicitada direcionadas a si.

Qual conteúdo obtido por uma terceira parte, assim como o conteúdo preparado pela XM, tais como, opiniões, pesquisa, análises, preços, outra informação ou links para websites de terceiras partes contidos neste website são prestados "no estado em que se encontram", como um comentário de mercado generalizado e não constitui conselho de investimento. Na medida em que qualquer conteúdo é construído como pesquisa de investimento, deve considerar e aceitar que este não tem como objetivo e nem foi preparado de acordo com os requisitos legais concebidos para promover a independência da pesquisa de investimento, desta forma, deve ser considerado material de marketing sob as leis e regulações relevantes. Por favor, certifique-se que leu e compreendeu a nossa Notificação sobre Pesquisa de Investimento não-independente e o Aviso de Risco, relativos à informação supracitada, os quais podem ser acedidos aqui.