Will Alphabet’s earnings tempt investors to buy more of its stock? – Stock Markets

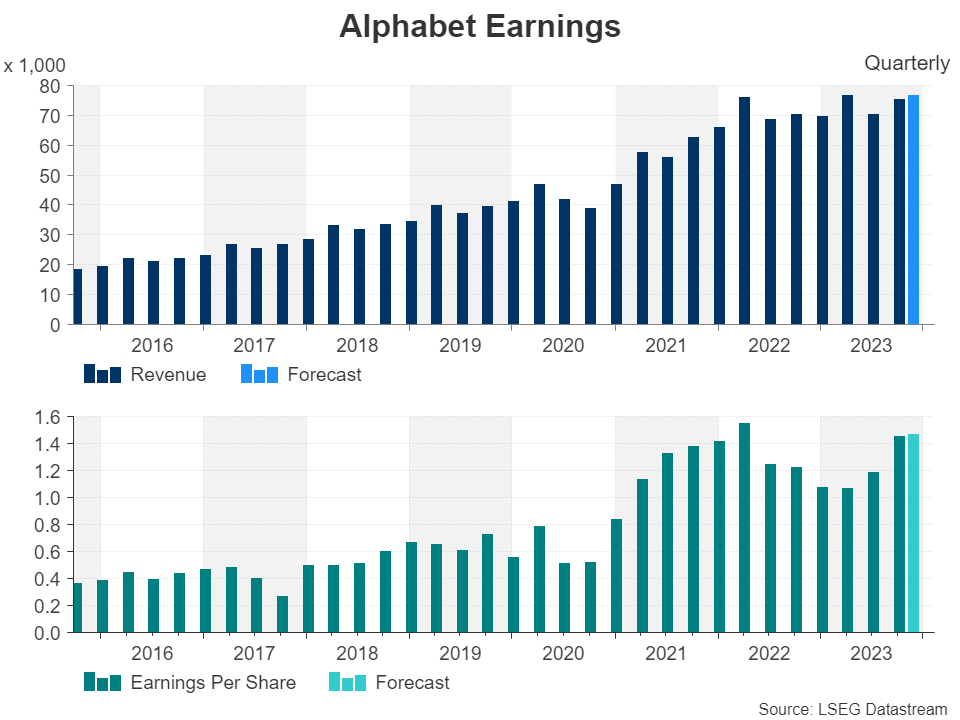

Alphabet is expected to report a nearly 10% increase in revenue

Despite latest rally, it remains relatively cheap compared to its peers

Results are scheduled to be released on October 24, after closing bell

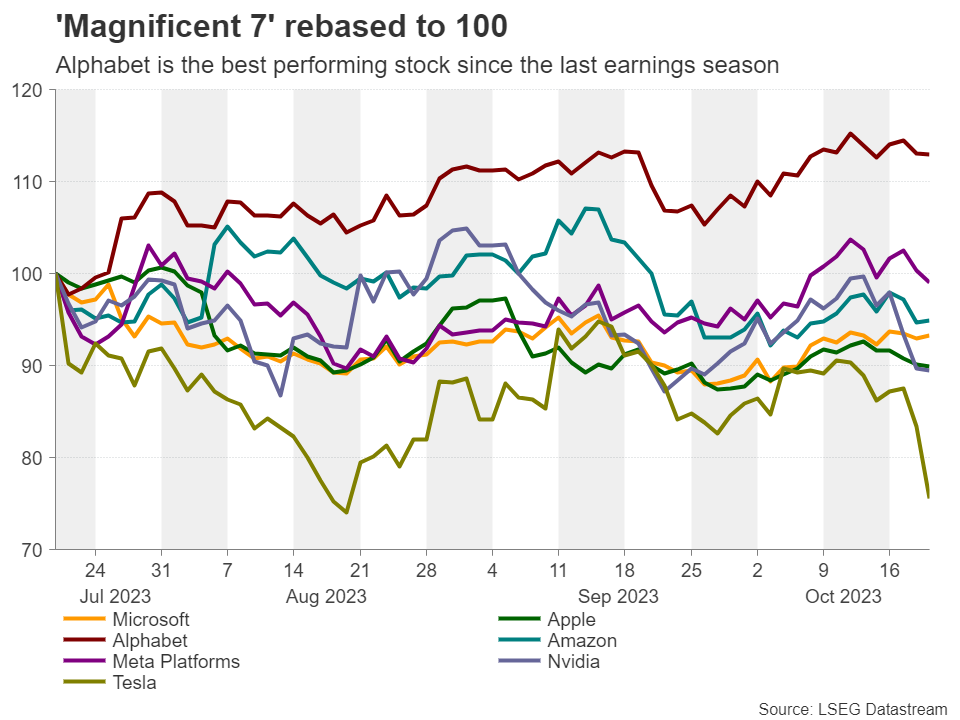

Since the prior earnings season, when Alphabet reported better-than-expected results for Q2, the firm’s shares rose more than 10%, outperforming all the other US mega-cap tech companies of the ‘Magnificent 7’ group.

On Tuesday, Google’s parent is forecast to announce earnings per share (EPS) of $1.45 during Q3, which would mark an impressive jump of 36.61% from the same period last year, while revenue is seen growing 9.91% to $75.94bn, which will mark the biggest y/y increase since Q2 2022. It is also worth mentioning that EPS returned to growth only in Q2 this year after six quarters of deterioration.

Back then, the highlights were Google Cloud and YouTube ads, which were the two biggest contributors to the overall revenue growth. Therefore, it would be interesting to see whether momentum continued in Q3.

Advertisement to take center stageWith the Google advertising segment accounting for around 78% of the firm’s revenue, YouTube ads as well as ads on Google’s search engine may play a determinant role on where the stock may be headed next, even if the initial reaction is triggered by any deviations from the EPS and overall revenue projections.

Google search is estimated to have around a 90% share of the search-engine market, and it is not a surprise that the antitrust case against its monopoly has attracted special attention. That said, even with the trials going on, investors expect the advertising sector’s revenue to grow by 6.44% y/y, nearly double the growth rate it posted in Q2.

On top of that, YouTube ads revenue received a boost in Q2 thanks to the offering of Shorts, a streaming service, and Primetime Channels, with the future looking more promising than the past. Yes, advertising may have been more cautious this year due to very high interest rates, and investors may have concerns that an economic slowdown could hinder a potential rebound even if interest rates begin to fall at some point, but the US Presidential elections and the Olympic games could very well offset this uncertainty, as these events have been historically proven to be major drivers in ad spend.

Cloud and AI business also in focusGoogle’s Cloud business grew around 28% in each of the prior quarters of the year, but it is now expected to have slowed to around 26%. Maybe the slowdown was due to higher interest rates weighing on consumption growth. With that in mind, it will be interesting to see whether expectations of rate cuts by the Fed next year will positively impact the firm’s projections of revenue from this service.

Regarding the artificial intelligence (AI) business, Microsoft’s ChatGPT initially appeared to be a major threat to Google’s Search, but Alphabet introduced its own chatbot, named Bard, which appears to be a more personalized service than ChatGPT that is more of a writing content-generating machine. As Bard is able to make personal suggestions, like creating vacation plans or recommending a diet, it could very well help the firm grow its advertising revenue even more.

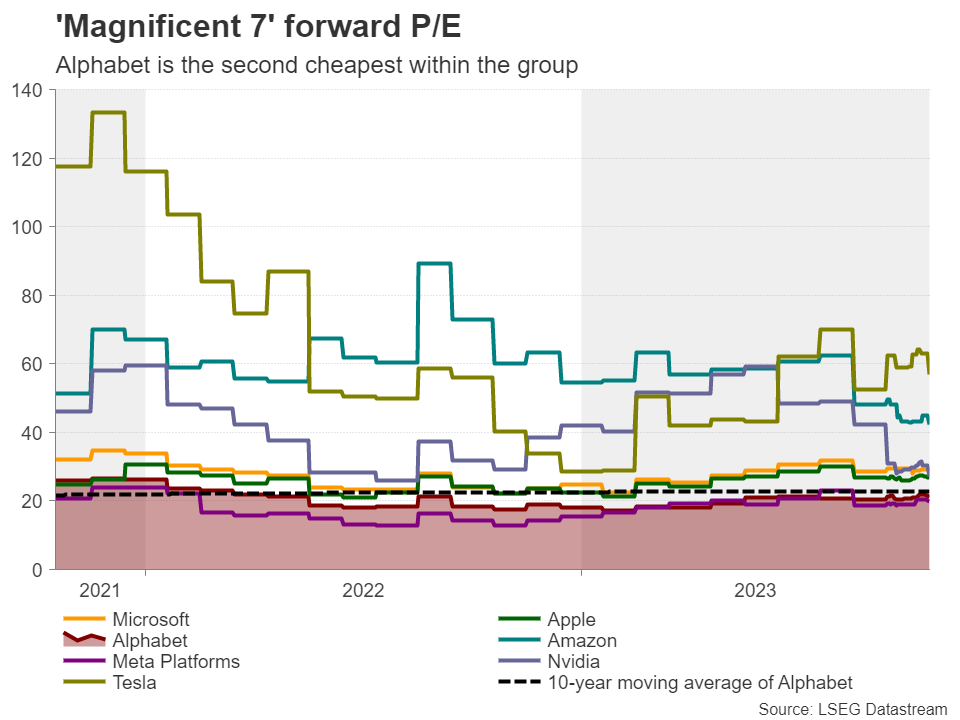

Valuation adds to attractivenessAlthough Alphabet is the best performing stock within the ‘Magnificent 7’ group since the last earnings season, it holds only the fourth place year-to-date, while from a multiples’ perspective, it appears to be the second cheapest, with a forward price-to-earnings ratio (P/E) of 21.4x. This multiple is slightly above the forward P/E ratio of the S&P 500 of 18.3x, but below its own 10-year moving average.

All this adds to the stock’s attractiveness, and even if the EPS or revenue results disappoint, a slide in the share price may be seen by investors as an opportunity to enter the market at more favorable levels.

Will the uptrend continue?From a technical standpoint, Alphabet’s stock entered a consolidation phase after hitting a one-and-a-half year high near the 141.00 zone on October 12. However, it remains in a broader uptrend, as the price structure remains of higher highs and higher lows above the uptrend line drawn from the low of April 26. Thus, even if it corrects lower in the near future, as long as it remains above that line, investors could well jump back into the action and drive the price up for another test near the 141.00 zone, or near 144.00, which is marked by the peak of March 29, 2022.

For the outlook to turn bearish, the stock may need to dive all the way below the 127.50 territory, which provided strong support in August and September, and acted as key resistance in June.

For the outlook to turn bearish, the stock may need to dive all the way below the 127.50 territory, which provided strong support in August and September, and acted as key resistance in June.Mga Kaugnay na Asset

Pinakabagong Balita

Disclaimer: Ang mga kabilang sa XM Group ay nagbibigay lang ng serbisyo sa pagpapatupad at pag-access sa aming Online Trading Facility, kung saan pinapahintulutan nito ang pagtingin at/o paggamit sa nilalaman na makikita sa website o sa pamamagitan nito, at walang layuning palitan o palawigin ito, at hindi din ito papalitan o papalawigin. Ang naturang pag-access at paggamit ay palaging alinsunod sa: (i) Mga Tuntunin at Kundisyon; (ii) Mga Babala sa Risk; at (iii) Kabuuang Disclaimer. Kaya naman ang naturang nilalaman ay ituturing na pangkalahatang impormasyon lamang. Mangyaring isaalang-alang na ang mga nilalaman ng aming Online Trading Facility ay hindi paglikom, o alok, para magsagawa ng anumang transaksyon sa mga pinansyal na market. Ang pag-trade sa alinmang pinansyal na market ay nagtataglay ng mataas na lebel ng risk sa iyong kapital.

Lahat ng materyales na nakalathala sa aming Online Trading Facility ay nakalaan para sa layuning edukasyonal/pang-impormasyon lamang at hindi naglalaman – at hindi dapat ituring bilang naglalaman – ng payo at rekomendasyon na pangpinansyal, tungkol sa buwis sa pag-i-invest, o pang-trade, o tala ng aming presyo sa pag-trade, o alok para sa, o paglikom ng, transaksyon sa alinmang pinansyal na instrument o hindi ginustong pinansyal na promosyon.

Sa anumang nilalaman na galing sa ikatlong partido, pati na ang mga nilalaman na inihanda ng XM, ang mga naturang opinyon, balita, pananaliksik, pag-analisa, presyo, ibang impormasyon o link sa ibang mga site na makikita sa website na ito ay ibibigay tulad ng nandoon, bilang pangkalahatang komentaryo sa market at hindi ito nagtataglay ng payo sa pag-i-invest. Kung ang alinmang nilalaman nito ay itinuring bilang pananaliksik sa pag-i-invest, kailangan mong isaalang-alang at tanggapin na hindi ito inilaan at inihanda alinsunod sa mga legal na pangangailangan na idinisenyo para maisulong ang pagsasarili ng pananaliksik sa pag-i-invest, at dahil dito ituturing ito na komunikasyon sa marketing sa ilalim ng mga kaugnay na batas at regulasyon. Mangyaring siguruhin na nabasa at naintindihan mo ang aming Notipikasyon sa Hindi Independyenteng Pananaliksik sa Pag-i-invest at Babala sa Risk na may kinalaman sa impormasyong nakalagay sa itaas, na maa-access dito.