What does central bank divergence mean for FX?

But it’s not all central banks. Some are faced with economies that are still struggling, so they won’t be exiting cheap money anytime soon. This sets the stage for some powerful FX trends moving forward. Carry tradeHigher interest rates are naturally beneficial for a currency. Investors can borrow in a low-yielding currency and then invest that money in higher-yielding assets abroad, earning a return on the difference and boosting demand for the high-yielding currency. This is called a carry trade. When investors sense that a central bank will be raising rates down the road, they usually try to front-run this trade by buying that currency, expecting it will appreciate later on. So who is raising rates? In a nutshell, of particular interest for FX traders is that the central banks of America, Canada, the UK, and New Zealand have all taken the first steps towards normalizing rates. The markets think the Reserve Bank of New Zealand will act first, currently pricing in an 80% chance for a rate increase in November this year, with another one to follow by spring 2022.

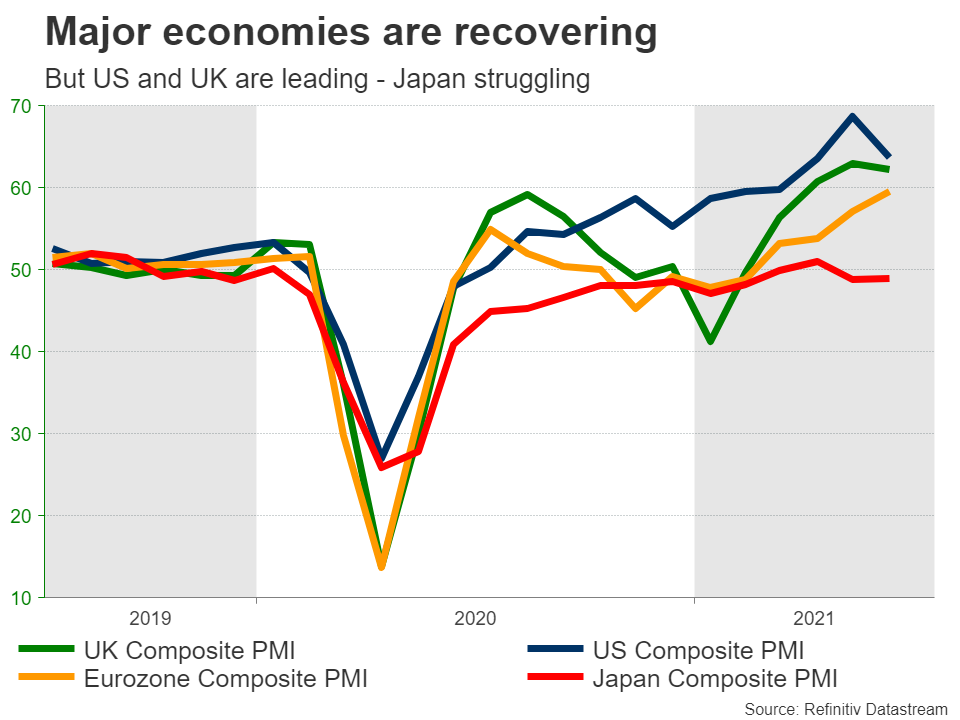

But it’s not all central banks. Some are faced with economies that are still struggling, so they won’t be exiting cheap money anytime soon. This sets the stage for some powerful FX trends moving forward. Carry tradeHigher interest rates are naturally beneficial for a currency. Investors can borrow in a low-yielding currency and then invest that money in higher-yielding assets abroad, earning a return on the difference and boosting demand for the high-yielding currency. This is called a carry trade. When investors sense that a central bank will be raising rates down the road, they usually try to front-run this trade by buying that currency, expecting it will appreciate later on. So who is raising rates? In a nutshell, of particular interest for FX traders is that the central banks of America, Canada, the UK, and New Zealand have all taken the first steps towards normalizing rates. The markets think the Reserve Bank of New Zealand will act first, currently pricing in an 80% chance for a rate increase in November this year, with another one to follow by spring 2022.  In America, the Fed is widely expected to announce that it will scale back its enormous asset purchase program in the coming months, which would be the first step towards higher rates. The first rate increase is priced in for December 2022, with almost another two in 2023. This pricing took a hit lately due to worries around the Delta variant, but not dramatically. The Bank of England is a similar story, along with the Bank of Canada. Who isn’t normalizing?The Eurozone, Japan, and Switzerland won’t be raising rates anytime soon. Japan and Switzerland are still trapped in a low inflation regime and economic growth is far from impressive. Europe is doing better so the European Central Bank might ultimately dial back its asset purchases, but it won’t raise rates for several years. The economy is just not that strong. In fact, the ECB recently raised its inflation target, essentially committing to negative interest rates for a longer period of time. Winners and losersAdding everything together, the currencies of nations that will enjoy higher interest rates are likely to outperform those that won’t be raising rates over the coming years.

In America, the Fed is widely expected to announce that it will scale back its enormous asset purchase program in the coming months, which would be the first step towards higher rates. The first rate increase is priced in for December 2022, with almost another two in 2023. This pricing took a hit lately due to worries around the Delta variant, but not dramatically. The Bank of England is a similar story, along with the Bank of Canada. Who isn’t normalizing?The Eurozone, Japan, and Switzerland won’t be raising rates anytime soon. Japan and Switzerland are still trapped in a low inflation regime and economic growth is far from impressive. Europe is doing better so the European Central Bank might ultimately dial back its asset purchases, but it won’t raise rates for several years. The economy is just not that strong. In fact, the ECB recently raised its inflation target, essentially committing to negative interest rates for a longer period of time. Winners and losersAdding everything together, the currencies of nations that will enjoy higher interest rates are likely to outperform those that won’t be raising rates over the coming years.  Specifically, this implies that the US dollar, British pound, Canadian dollar, and New Zealand dollar might shine against the Japanese yen, Swiss franc, and to a lesser extent the euro. Pairs like dollar/yen or pound/franc could head higher over time as this theme crystallizes. What’s the risk? The main risk to this view would be some shock that hits global markets. For example, a new covid mutation that the vaccines are not effective against, which sees lockdowns return. That could slow down the pace of normalization in many countries, and also boost both the yen and the franc through safe-haven demand. In fact, we have already seen this play out this week. Concerns around the Delta covid variant have seen rates decline as investors started pricing in a slower normalization path by the major central banks, boosting the yen and the franc in the process.

Specifically, this implies that the US dollar, British pound, Canadian dollar, and New Zealand dollar might shine against the Japanese yen, Swiss franc, and to a lesser extent the euro. Pairs like dollar/yen or pound/franc could head higher over time as this theme crystallizes. What’s the risk? The main risk to this view would be some shock that hits global markets. For example, a new covid mutation that the vaccines are not effective against, which sees lockdowns return. That could slow down the pace of normalization in many countries, and also boost both the yen and the franc through safe-haven demand. In fact, we have already seen this play out this week. Concerns around the Delta covid variant have seen rates decline as investors started pricing in a slower normalization path by the major central banks, boosting the yen and the franc in the process.  But ultimately, this is unlikely to last long. The Delta variant might slow down this trend, but it won’t derail it. It is mainly an issue for emerging markets, not the advanced economies that are mostly vaccinated already. It will take something much bigger to demolish the narrative of monetary policy normalization.

But ultimately, this is unlikely to last long. The Delta variant might slow down this trend, but it won’t derail it. It is mainly an issue for emerging markets, not the advanced economies that are mostly vaccinated already. It will take something much bigger to demolish the narrative of monetary policy normalization. Pinakabagong Balita

Disclaimer: Ang mga kabilang sa XM Group ay nagbibigay lang ng serbisyo sa pagpapatupad at pag-access sa aming Online Trading Facility, kung saan pinapahintulutan nito ang pagtingin at/o paggamit sa nilalaman na makikita sa website o sa pamamagitan nito, at walang layuning palitan o palawigin ito, at hindi din ito papalitan o papalawigin. Ang naturang pag-access at paggamit ay palaging alinsunod sa: (i) Mga Tuntunin at Kundisyon; (ii) Mga Babala sa Risk; at (iii) Kabuuang Disclaimer. Kaya naman ang naturang nilalaman ay ituturing na pangkalahatang impormasyon lamang. Mangyaring isaalang-alang na ang mga nilalaman ng aming Online Trading Facility ay hindi paglikom, o alok, para magsagawa ng anumang transaksyon sa mga pinansyal na market. Ang pag-trade sa alinmang pinansyal na market ay nagtataglay ng mataas na lebel ng risk sa iyong kapital.

Lahat ng materyales na nakalathala sa aming Online Trading Facility ay nakalaan para sa layuning edukasyonal/pang-impormasyon lamang at hindi naglalaman – at hindi dapat ituring bilang naglalaman – ng payo at rekomendasyon na pangpinansyal, tungkol sa buwis sa pag-i-invest, o pang-trade, o tala ng aming presyo sa pag-trade, o alok para sa, o paglikom ng, transaksyon sa alinmang pinansyal na instrument o hindi ginustong pinansyal na promosyon.

Sa anumang nilalaman na galing sa ikatlong partido, pati na ang mga nilalaman na inihanda ng XM, ang mga naturang opinyon, balita, pananaliksik, pag-analisa, presyo, ibang impormasyon o link sa ibang mga site na makikita sa website na ito ay ibibigay tulad ng nandoon, bilang pangkalahatang komentaryo sa market at hindi ito nagtataglay ng payo sa pag-i-invest. Kung ang alinmang nilalaman nito ay itinuring bilang pananaliksik sa pag-i-invest, kailangan mong isaalang-alang at tanggapin na hindi ito inilaan at inihanda alinsunod sa mga legal na pangangailangan na idinisenyo para maisulong ang pagsasarili ng pananaliksik sa pag-i-invest, at dahil dito ituturing ito na komunikasyon sa marketing sa ilalim ng mga kaugnay na batas at regulasyon. Mangyaring siguruhin na nabasa at naintindihan mo ang aming Notipikasyon sa Hindi Independyenteng Pananaliksik sa Pag-i-invest at Babala sa Risk na may kinalaman sa impormasyong nakalagay sa itaas, na maa-access dito.