Week Ahead – Tracking the recovery: is Europe lagging the US?

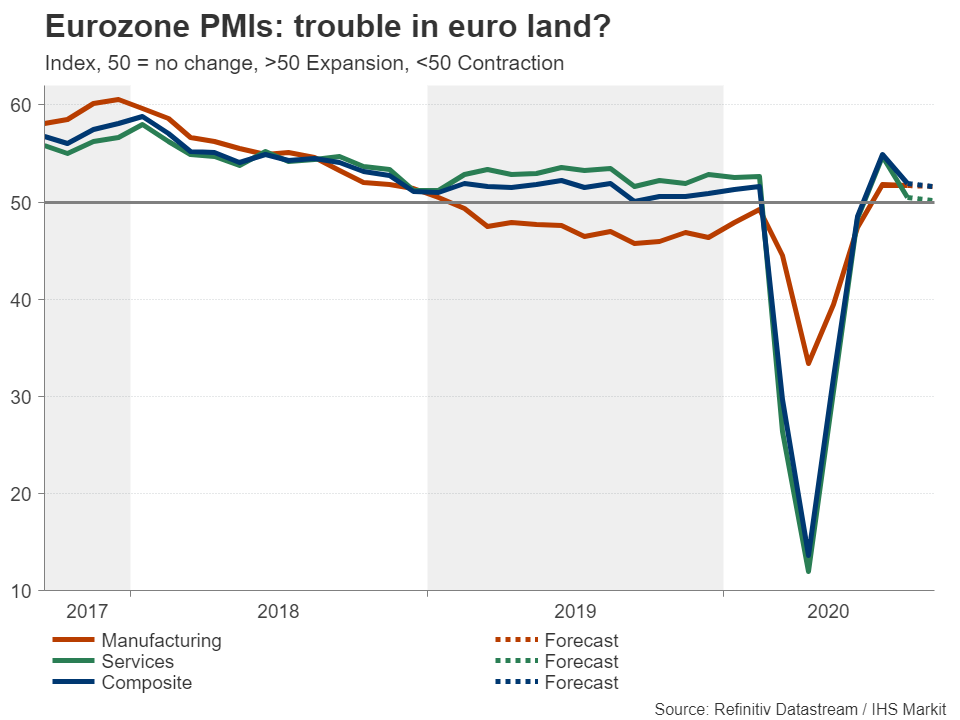

Europe may still be simmering under unusually warm temperatures, but the economic climate may have already started to cool. The last set of PMIs by IHS Markit were far from encouraging and the September numbers will be crucial in determining whether this was simply a mild tapering in momentum or a sign of the limits to how much economic life can return to normal while the pandemic rages on.

The flash readings for the euro area are due on Wednesday and the forecasts suggest the recovery has been moderating further in September. The manufacturing PMI is expected to slip 0.1 points to 51.6, but more worryingly, the services print is anticipated to fall to 50.2 – barely holding in expansionary territory. The Eurozone’s composite PMI is projected to decline from 51.9 to 51.6.

Investors will be able to have another glimpse into the progress of the recovery from Germany’s Ifo business survey on Thursday.

Any disappointment from the PMI data could prove to be the final nail in the coffin for the euro rally. The single currency has been moving sideways during September as investors scale back some of their more optimistic forecasts for the Eurozone economy. If the data fail to provide clear signals, the euro is likely to extend its consolidation. However, strong surprises, whether positive or negative, have the potential to break this trading range as a clearer picture would emerge about where growth is headed in Q4.

SNB: fighting a battle it cannot winThe euro’s next direction will certainly be watched very closely by the Swiss National Bank, which effectively views the euro/franc exchange rate as its main policy tool given its reluctance to cut rates below -0.75%. The SNB’s predicament means it is almost certain to keep policy unchanged on Thursday. But Chairman Thomas Jordan may step up his warnings of forex intervention as the Swiss franc has not gone where the Bank would have liked it to since the last meeting.

The positive sentiment for Europe’s recovery prospects that’s been in play since late May has been anathema for the SNB as it seems to have infected the franc too, constraining the euro’s advances versus the franc, while franc/dollar has been taking its cues from euro/dollar. In reality, it’s unlikely that Jordan will have more success than in the past in talking down the safe-haven franc.

All steady at the Riksbank, Norges Bank

All steady at the Riksbank, Norges Bank The SNB will not be the only central bank event in Europe over the coming week as the Riksbank and Norges Bank also meet, on Tuesday and Thursday, respectively. Both central banks are expected to hold interest rates at current levels, but the Riksbank is more likely to take a more cautious stance than the somewhat more optimistic Norges Bank. However, after the surprise expansion of its quantitative easing programme in July, which will now include corporate bonds, and the steady improvement in economic data, the Riksbank may hold off from flagging further easing measures for now.

Nevertheless, both the Swedish krona and the Norwegian crown will be sensitive to any changes in their central banks’ language, though only in the short term. Their broader outlooks are expected to stay bullish as there’s little chance of neither the Riksbank nor the Norges Bank outpacing the European Central Bank or the Fed with their respective stimulus.

RBNZ could move closer to negative ratesBut it will probably be the Reserve Bank of New Zealand policy decision that steals all the limelight. The RBNZ meets on Wednesday (local time) and is expected to stand pat. New Zealand’s economy took a slightly smaller hit than anticipated in the second quarter. However, with the country being forced into a second nationwide lockdown in August, the recovery is already on very shaky grounds.

This makes it all the more likely that negative interest rates are at the forefront of the options being mulled by the RBNZ in terms of new weapons to add to its pandemic arsenal. Governor Orr recently indicated the Bank was “actively preparing” a package of additional policy tools and may use the September meeting to hint at a possible timeline.

Still, considering that globally, the recovery has been generally stronger than many had initially predicted, the RBNZ may not be ready to deploy new firepower just yet and traders may have to wait a while longer for more precise signals. If this turns out to be the case, the New Zealand dollar’s uptrend should stay intact, at least for as long as the risk rally lasts, that is.

Flash PMIs may ease pound’s Brexit painOver in the United Kingdom, it’s all about Brexit again, though investors should be able to make some room for the latest PMI prints. Unlike in the euro area where the recovery appears to be weakening, the UK’s climb out of the virus slump so far bears a closer resemblance to a V-shape. However, the rebound probably lost some steam in September as the government’s Eat Out voucher scheme came to an end and social distancing rules were toughened amid a jump in new virus cases across the UK.

The flash PMI numbers are out on Wednesday and could provide the pound with a bit of a boost if they beat the forecasts. Sterling has undergone a sharp reality check in September as tensions with the European Union flared after Boris Johnson’s latest act of brinksmanship in the post-Brexit trade negotiations.

Those negotiations are ongoing and Brexit headlines could jolt the pound at any time. But despite the worryingly hostile rhetoric from London, the EU has remained at the negotiating table and there even seems to be some progress in breaking the deadlock over fisheries. Hence, the upside and downside risks for the pound are more or less even right now and traders should get used to seeing more big spikes in either direction as the October 15 deadline approaches.

Dollar eyes political risks as Fed boost fadesThere’s not a whole lot on the US calendar that could set alight the US dollar next week and unless there are some major developments on the vaccine, election or fiscal stimulus fronts, further consolidation may be the order of the day. The greenback did get quite a lift from the Federal Reserve, which stopped short of announcing additional stimulus at its meeting last week, but has since been drifting lower against a basket of currencies even though risk appetite has been in short supply lately.

Wednesday’s flash PMI reports may be the best hope to inject some life into a ranging market in the coming days. The US PMIs are released a few hours after the European ones and should they again show that the American economy outperformed the Eurozone’s, the dollar could find itself back on the front foot.

Housing data will also be watched as the boom in the interest-rate sensitive property sector has been one of the few bright spots in the economy during the pandemic. Existing home sales are due on Tuesday, followed by new home sales on Thursday. Friday’s durable goods orders for August will be important too.

Autumn risksOverall, though, with Election Day nearing, markets are increasingly in a wait-and-see mode and the data may only trigger knee-jerk reactions at best.

But the vote for electing a new American president on November 3 is not the only reason why the next 2-3 months will be a decisive time for the markets. Congress has yet to reach a compromise on a new fiscal stimulus package and there is a slim chance a deal can be made in the next week or two. Otherwise, it will most likely have to wait until after the election.

In addition, announcements on a coronavirus vaccine could be imminent, which are potentially the dollar’s biggest threat (though a much-needed lifeline for the stock market rally). All of these things could determine whether a fresh round of monetary stimulus will be necessary before the year-end. The question is, until one or more of these stories begin to unfold, will markets stay calm or will they have a panic attack?Pinakabagong Balita

Disclaimer: Ang mga kabilang sa XM Group ay nagbibigay lang ng serbisyo sa pagpapatupad at pag-access sa aming Online Trading Facility, kung saan pinapahintulutan nito ang pagtingin at/o paggamit sa nilalaman na makikita sa website o sa pamamagitan nito, at walang layuning palitan o palawigin ito, at hindi din ito papalitan o papalawigin. Ang naturang pag-access at paggamit ay palaging alinsunod sa: (i) Mga Tuntunin at Kundisyon; (ii) Mga Babala sa Risk; at (iii) Kabuuang Disclaimer. Kaya naman ang naturang nilalaman ay ituturing na pangkalahatang impormasyon lamang. Mangyaring isaalang-alang na ang mga nilalaman ng aming Online Trading Facility ay hindi paglikom, o alok, para magsagawa ng anumang transaksyon sa mga pinansyal na market. Ang pag-trade sa alinmang pinansyal na market ay nagtataglay ng mataas na lebel ng risk sa iyong kapital.

Lahat ng materyales na nakalathala sa aming Online Trading Facility ay nakalaan para sa layuning edukasyonal/pang-impormasyon lamang at hindi naglalaman – at hindi dapat ituring bilang naglalaman – ng payo at rekomendasyon na pangpinansyal, tungkol sa buwis sa pag-i-invest, o pang-trade, o tala ng aming presyo sa pag-trade, o alok para sa, o paglikom ng, transaksyon sa alinmang pinansyal na instrument o hindi ginustong pinansyal na promosyon.

Sa anumang nilalaman na galing sa ikatlong partido, pati na ang mga nilalaman na inihanda ng XM, ang mga naturang opinyon, balita, pananaliksik, pag-analisa, presyo, ibang impormasyon o link sa ibang mga site na makikita sa website na ito ay ibibigay tulad ng nandoon, bilang pangkalahatang komentaryo sa market at hindi ito nagtataglay ng payo sa pag-i-invest. Kung ang alinmang nilalaman nito ay itinuring bilang pananaliksik sa pag-i-invest, kailangan mong isaalang-alang at tanggapin na hindi ito inilaan at inihanda alinsunod sa mga legal na pangangailangan na idinisenyo para maisulong ang pagsasarili ng pananaliksik sa pag-i-invest, at dahil dito ituturing ito na komunikasyon sa marketing sa ilalim ng mga kaugnay na batas at regulasyon. Mangyaring siguruhin na nabasa at naintindihan mo ang aming Notipikasyon sa Hindi Independyenteng Pananaliksik sa Pag-i-invest at Babala sa Risk na may kinalaman sa impormasyong nakalagay sa itaas, na maa-access dito.