Meta Q3 earnings next on the agenda – Stock Markets

Meta to report strong earnings after market closes

Focus remains on AI & Metaverse outlook

Meta platforms, the parent company of Facebook and Instagram, will announce third-quarter earnings on Wednesday after the market closes. Forecasts point to notable growth, with the consensus recommendation from analysts polled by Refinitiv being a buy.

Total revenue is expected to show an annual growth of 21% to $33.5bln in the three months to September – double the 11% growth in the second quarter. The family of apps (Facebook, Messenger, Instagram, WhatsApp) has probably experienced a similar whopping expansion, with the advertising segment also rebounding by an equivalent solid percentage.

In other important financial metrics, earnings per share (EPS) are forecast to jump to $3.63 compared to $2.98 in the previous quarter and $1.64 in the same period a year ago. As regards its profitability, net income is expected to grow at the fastest pace in a couple of years – by more than 100%.

Having beat estimates over the past two quarters and with several institutional investors and hedge funds raising their Meta shareholdings and revising their target prices higher recently, the bar is set high for the social networking company.

Is Meta an attractive stock?The negative reaction to Tesla and Netflix as well as Alphabet's mixed results shows that investors are more sensitive to data misses this time, and is unable to repeat July's rally. Despite current uncertain market conditions and ongoing lawsuits, Meta platforms could still shine in the tech world and attract investors even if the stock price declines.

Engagement is a powerful tool for the giant social media company, making it hard for anyone to find any easy alternative to connect with friends and family and get updated on local and global news. It’s even more impressive to know that the planet has a population of nearly 7.9 billion and almost half of it is actively using its Facebook account on a monthly basis. That’s definitely a plus for developing its Metaverse world and incorporating its AI tools in everyone’s life at a faster pace than its peers.

The lack of alternative social media platforms could make charges difficult to avoid for those who don’t want to share their digital activity with the company. Note that Meta is planning to charge its European audience $14 monthly for ad-free Facebook and Instagram or $17 for both and on desktop. While this might cause some discomfort among members it could be a new source of revenue diversification for the company besides the monetization of Reels and advertising. On that front, it would be interesting to learn whether the company plans to expand its charges to other regions too.

Expenses could growOn the other hand, the ongoing transition to Metaverse and the expansion of AI will not come at a cheap cost as competition gets more intense. Meta aims to start training a new AI model, which will be a more advanced version than its open-source AI language model Llama 2 and be a serious competitor to chatGPT, as soon as in early 2024. Other exciting AI projects are also in the pipeline, including chatbots based on celebrities and features connected to Ray-ban glasses, while improvements on the virtual reality front are also on the way following the release of the new Quest 3 headset.

During its previous earnings release, Zuckerberg’s group of companies said that total expenses could increase to $88-91 billion by the end of 2023 and further grow in 2024 providing no specific number for the latter. Any guidance of expenses growing below $100bln or at least below revenue growth could be market positive amid elevated interest rates and wages and heightened geopolitical risks.

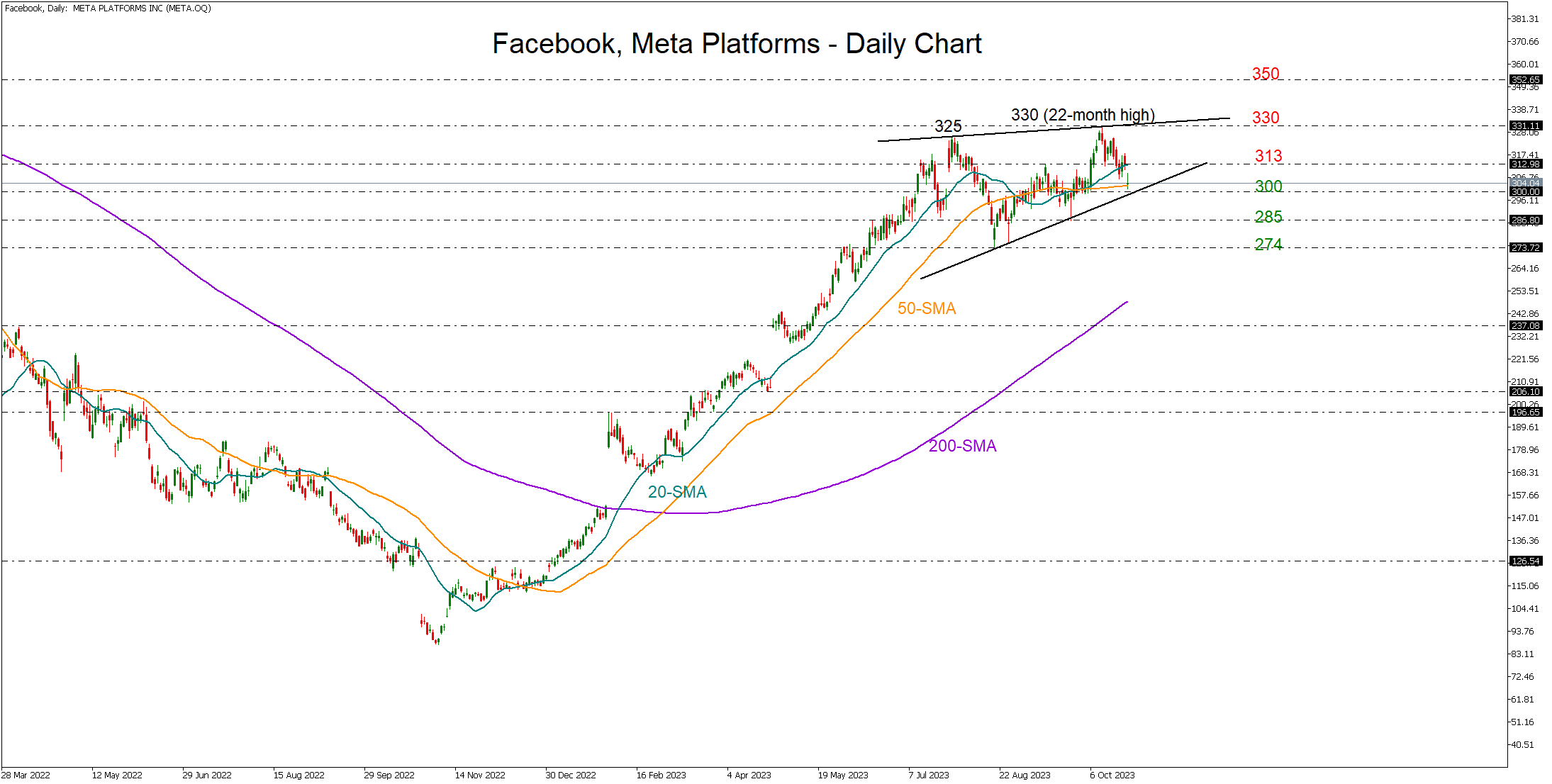

Levels to watchTurning to stock markets, Meta’s stock has been the second-best performer after NVIDIA in the S&P 500 space during 2023, trading 159% higher year-to-date compared to the index’s gain of 10%. Stronger-than-expected advertising revenues and a brighter outlook for the final quarter of 2023 could be good news for the stock as recession fears and geopolitical risks weigh on sentiment. Should the price bounce back above the 20-day simple moving average (SMA) at 312, the door would open again for the 2023 peak of 330. The 2021 resistance of 350 could be the next obstacle.

Alternatively, a miss in earnings and signals of more challenging years ahead could squeeze the stock below the 50-day SMA and the 300 level, shifting the attention to the 285 constraining zone and then to the August trough of 274.

Mga Kaugnay na Asset

Pinakabagong Balita

Disclaimer: Ang mga kabilang sa XM Group ay nagbibigay lang ng serbisyo sa pagpapatupad at pag-access sa aming Online Trading Facility, kung saan pinapahintulutan nito ang pagtingin at/o paggamit sa nilalaman na makikita sa website o sa pamamagitan nito, at walang layuning palitan o palawigin ito, at hindi din ito papalitan o papalawigin. Ang naturang pag-access at paggamit ay palaging alinsunod sa: (i) Mga Tuntunin at Kundisyon; (ii) Mga Babala sa Risk; at (iii) Kabuuang Disclaimer. Kaya naman ang naturang nilalaman ay ituturing na pangkalahatang impormasyon lamang. Mangyaring isaalang-alang na ang mga nilalaman ng aming Online Trading Facility ay hindi paglikom, o alok, para magsagawa ng anumang transaksyon sa mga pinansyal na market. Ang pag-trade sa alinmang pinansyal na market ay nagtataglay ng mataas na lebel ng risk sa iyong kapital.

Lahat ng materyales na nakalathala sa aming Online Trading Facility ay nakalaan para sa layuning edukasyonal/pang-impormasyon lamang at hindi naglalaman – at hindi dapat ituring bilang naglalaman – ng payo at rekomendasyon na pangpinansyal, tungkol sa buwis sa pag-i-invest, o pang-trade, o tala ng aming presyo sa pag-trade, o alok para sa, o paglikom ng, transaksyon sa alinmang pinansyal na instrument o hindi ginustong pinansyal na promosyon.

Sa anumang nilalaman na galing sa ikatlong partido, pati na ang mga nilalaman na inihanda ng XM, ang mga naturang opinyon, balita, pananaliksik, pag-analisa, presyo, ibang impormasyon o link sa ibang mga site na makikita sa website na ito ay ibibigay tulad ng nandoon, bilang pangkalahatang komentaryo sa market at hindi ito nagtataglay ng payo sa pag-i-invest. Kung ang alinmang nilalaman nito ay itinuring bilang pananaliksik sa pag-i-invest, kailangan mong isaalang-alang at tanggapin na hindi ito inilaan at inihanda alinsunod sa mga legal na pangangailangan na idinisenyo para maisulong ang pagsasarili ng pananaliksik sa pag-i-invest, at dahil dito ituturing ito na komunikasyon sa marketing sa ilalim ng mga kaugnay na batas at regulasyon. Mangyaring siguruhin na nabasa at naintindihan mo ang aming Notipikasyon sa Hindi Independyenteng Pananaliksik sa Pag-i-invest at Babala sa Risk na may kinalaman sa impormasyong nakalagay sa itaas, na maa-access dito.