Will Alphabet’s earnings tempt investors to buy more of its stock? – Stock Markets

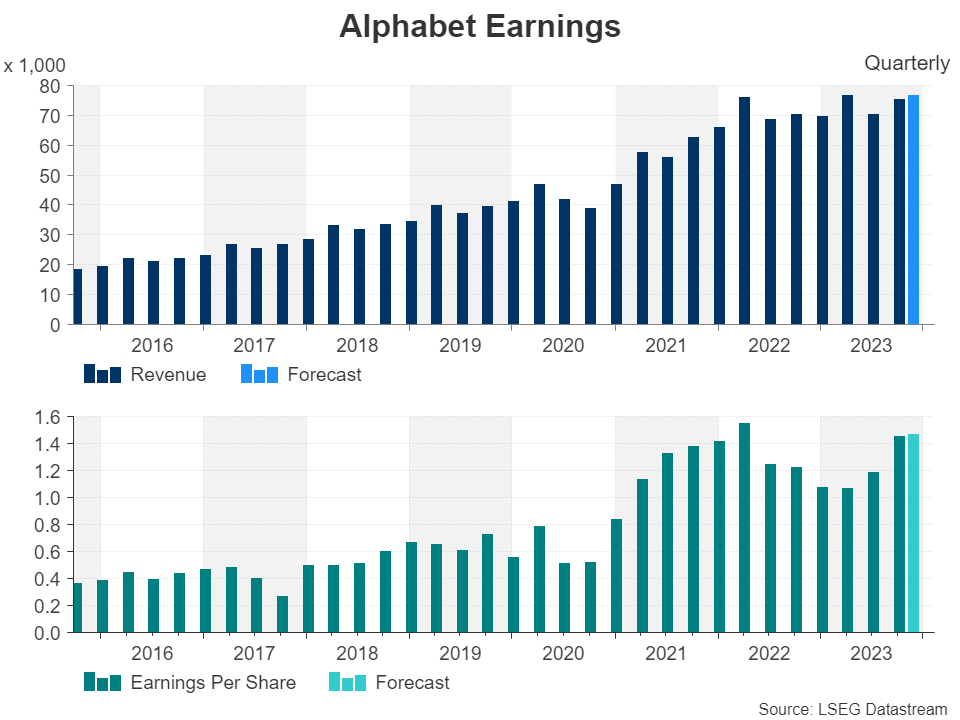

Alphabet is expected to report a nearly 10% increase in revenue

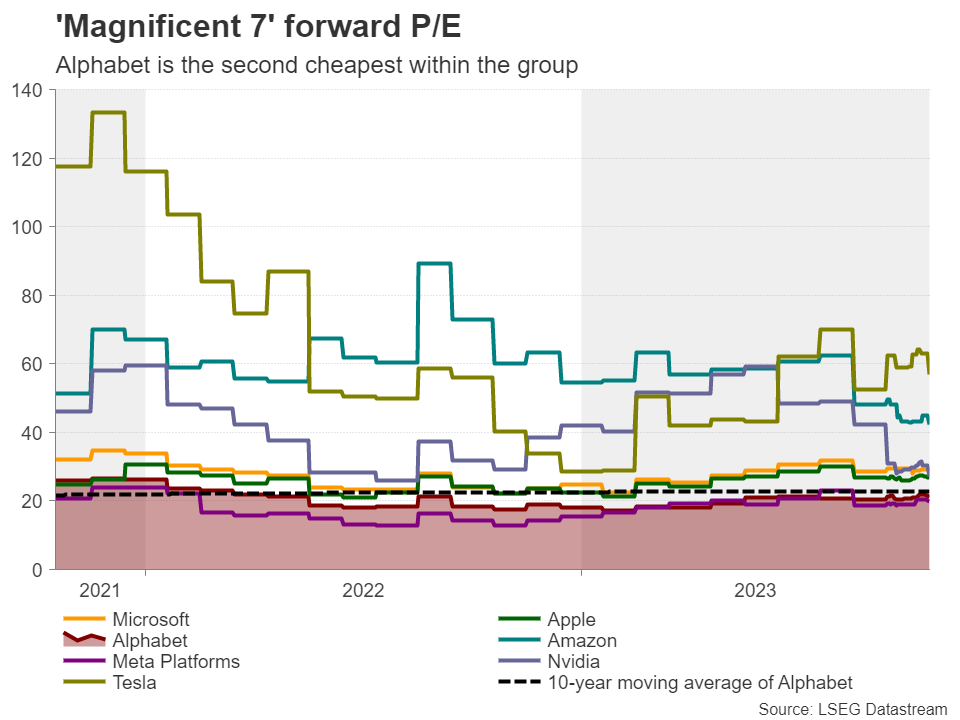

Despite latest rally, it remains relatively cheap compared to its peers

Results are scheduled to be released on October 24, after closing bell

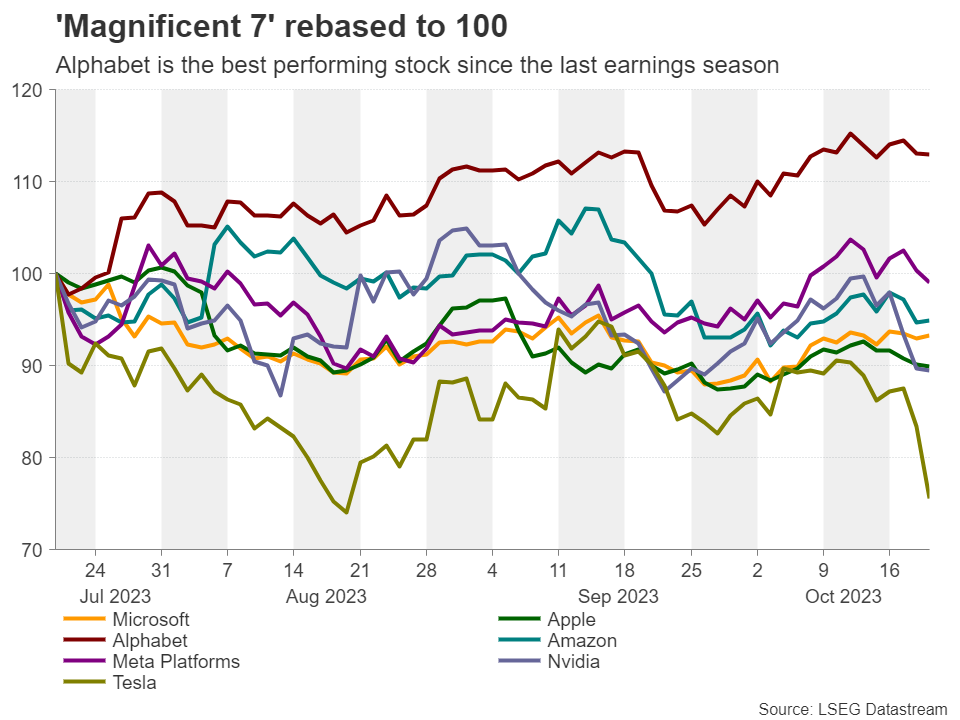

Since the prior earnings season, when Alphabet reported better-than-expected results for Q2, the firm’s shares rose more than 10%, outperforming all the other US mega-cap tech companies of the ‘Magnificent 7’ group.

On Tuesday, Google’s parent is forecast to announce earnings per share (EPS) of $1.45 during Q3, which would mark an impressive jump of 36.61% from the same period last year, while revenue is seen growing 9.91% to $75.94bn, which will mark the biggest y/y increase since Q2 2022. It is also worth mentioning that EPS returned to growth only in Q2 this year after six quarters of deterioration.

Back then, the highlights were Google Cloud and YouTube ads, which were the two biggest contributors to the overall revenue growth. Therefore, it would be interesting to see whether momentum continued in Q3.

Advertisement to take center stageWith the Google advertising segment accounting for around 78% of the firm’s revenue, YouTube ads as well as ads on Google’s search engine may play a determinant role on where the stock may be headed next, even if the initial reaction is triggered by any deviations from the EPS and overall revenue projections.

Google search is estimated to have around a 90% share of the search-engine market, and it is not a surprise that the antitrust case against its monopoly has attracted special attention. That said, even with the trials going on, investors expect the advertising sector’s revenue to grow by 6.44% y/y, nearly double the growth rate it posted in Q2.

On top of that, YouTube ads revenue received a boost in Q2 thanks to the offering of Shorts, a streaming service, and Primetime Channels, with the future looking more promising than the past. Yes, advertising may have been more cautious this year due to very high interest rates, and investors may have concerns that an economic slowdown could hinder a potential rebound even if interest rates begin to fall at some point, but the US Presidential elections and the Olympic games could very well offset this uncertainty, as these events have been historically proven to be major drivers in ad spend.

Cloud and AI business also in focusGoogle’s Cloud business grew around 28% in each of the prior quarters of the year, but it is now expected to have slowed to around 26%. Maybe the slowdown was due to higher interest rates weighing on consumption growth. With that in mind, it will be interesting to see whether expectations of rate cuts by the Fed next year will positively impact the firm’s projections of revenue from this service.

Regarding the artificial intelligence (AI) business, Microsoft’s ChatGPT initially appeared to be a major threat to Google’s Search, but Alphabet introduced its own chatbot, named Bard, which appears to be a more personalized service than ChatGPT that is more of a writing content-generating machine. As Bard is able to make personal suggestions, like creating vacation plans or recommending a diet, it could very well help the firm grow its advertising revenue even more.

Valuation adds to attractivenessAlthough Alphabet is the best performing stock within the ‘Magnificent 7’ group since the last earnings season, it holds only the fourth place year-to-date, while from a multiples’ perspective, it appears to be the second cheapest, with a forward price-to-earnings ratio (P/E) of 21.4x. This multiple is slightly above the forward P/E ratio of the S&P 500 of 18.3x, but below its own 10-year moving average.

All this adds to the stock’s attractiveness, and even if the EPS or revenue results disappoint, a slide in the share price may be seen by investors as an opportunity to enter the market at more favorable levels.

Will the uptrend continue?From a technical standpoint, Alphabet’s stock entered a consolidation phase after hitting a one-and-a-half year high near the 141.00 zone on October 12. However, it remains in a broader uptrend, as the price structure remains of higher highs and higher lows above the uptrend line drawn from the low of April 26. Thus, even if it corrects lower in the near future, as long as it remains above that line, investors could well jump back into the action and drive the price up for another test near the 141.00 zone, or near 144.00, which is marked by the peak of March 29, 2022.

For the outlook to turn bearish, the stock may need to dive all the way below the 127.50 territory, which provided strong support in August and September, and acted as key resistance in June.

For the outlook to turn bearish, the stock may need to dive all the way below the 127.50 territory, which provided strong support in August and September, and acted as key resistance in June.Gerelateerde activa

Laatste nieuws

Disclaimer: De entiteiten van de XM Group bieden diensten en toegang tot ons online handelsplatform op basis van uitsluitend-uitvoering, waardoor een persoon de beschikbare content op of via de website kan bekijken en/of gebruiken, zonder dat dit is bedoeld voor wijziging of uitbreiding. Dergelijk(e) toegang en gebruik vallen onder: (i) de algemene voorwaarden; (ii) risicowaarschuwingen; en de (iii) volledige disclaimer. Dergelijke content wordt daarom alleen aangeboden als algemene informatie. Wees u er daarnaast vooral van bewust dat de inhoud op ons online handelsplatform geen verzoek of aanbieding omvat om transacties op de financiële markten uit te voeren. Het beleggen op welke financiële markt dan ook vormt een aanzienlijk risico voor uw vermogen.

Alle materialen die op ons online handelsplatform worden gepubliceerd zijn bedoeld voor educatieve/informatieve doeleinden en omvatten geen – en moeten niet worden beschouwd als het bevatten van – financieel, vermogensbelastings- of handelsadvies en aanbevelingen, of een overzicht van onze handelsprijzen, of een aanbod of aanvraag van een transactie in financiële instrumenten of ongevraagde financiële promoties voor u.

Alle content van derden, alsmede content die is voorbereid door XM, zoals opinies, nieuws, onderzoeken, analyses, prijzen en andere informatie of koppelingen naar externe websites op deze website worden aangeboden op een 'zoals-ze-zijn'-basis, als algemene marktcommentaren, en vormen geen beleggingsadvies. Voor zover dat content wordt beschouwd als beleggingsonderzoek, moet u zich ervan bewust zijn en accepteren dat de content niet bedoeld was en niet is voorbereid in overeenstemming met de wettelijke vereisten die zijn opgesteld om de onafhankelijkheid van beleggingsonderzoek te bevorderen en als zodanig onder de geldende wetgeving en richtlijnen moet worden beschouwd als marketingcommunicatie. Zorg ervoor dat u onze Mededeling over niet-onafhankelijk beleggingsonderzoek en risicowaarschuwing in verband met de voorgaande informatie doorneemt en begrijpt; die kunt u hier lezen.