Could a strong inflation print reignite hawkish RBA expectations? – Forex News Preview

The RBA holds its monthly meeting on June 6 with the market expecting no change at the current 3.85% cash target rate. A total of 20 bps of rate hikes are priced in by the September 2023 meeting, implying an 80% chance of a full 25 bps rate hike. While we don’t exclude a surprise at next week’s meeting, the overall environment appears to be less supportive of hawkish surprises. Especially as the neighbouring RBNZ has probably announced its last hike in the current cycle and the Fed is almost ready to keep rates unchanged in its upcoming meeting for the first time since March 2022.

However, as seen in early May, the RBA could pull another rate hike out of the hat. The bar though appears to be higher now, especially as the preliminary PMIs were not a pleasant reading, unemployment is edging higher again and retail sales surprised on the downside. But the key data print remains inflation.

Monthly CPI is not really “monthly CPI”The monthly CPI figure will be released on Wednesday, and it is expected to remain comfortably above 6% and very close to April's 6.3% year-on-year change. Confirmation of the consensus forecast, or an even lower print, would probably cement the very low market expectations for the June meeting. On the other hand, a stronger print, especially if it climbs above 7%, would hesitantly bring back to the table the possibility of another rate hike, giving the aussie a much-needed boost.

The market is very keen on the monthly inflation updates, but here lies a critical issue for the RBA. The official inflation figures for Australia are published on a quarterly basis. In October 2022 the Bureau of Statistics started to publish a monthly figure which is only two-thirds representative of the quarterly CPI basket. This means that revisions take place and could be significant.

Housing sector still under pressureAnother sector that continues to get significant airtime, mostly for negative reasons, is the housing sector. With the building approvals moving again in negative territory, the focus now turns to home loans. This tends to be a leading indicator of demand in the housing sector with the March figure finally showing a positive change after 9 straight months of negative growth. The year-on-year figures remain almost 25% lower, but another positive monthly change would be seen as a positive signal despite the aggressive rate hikes.

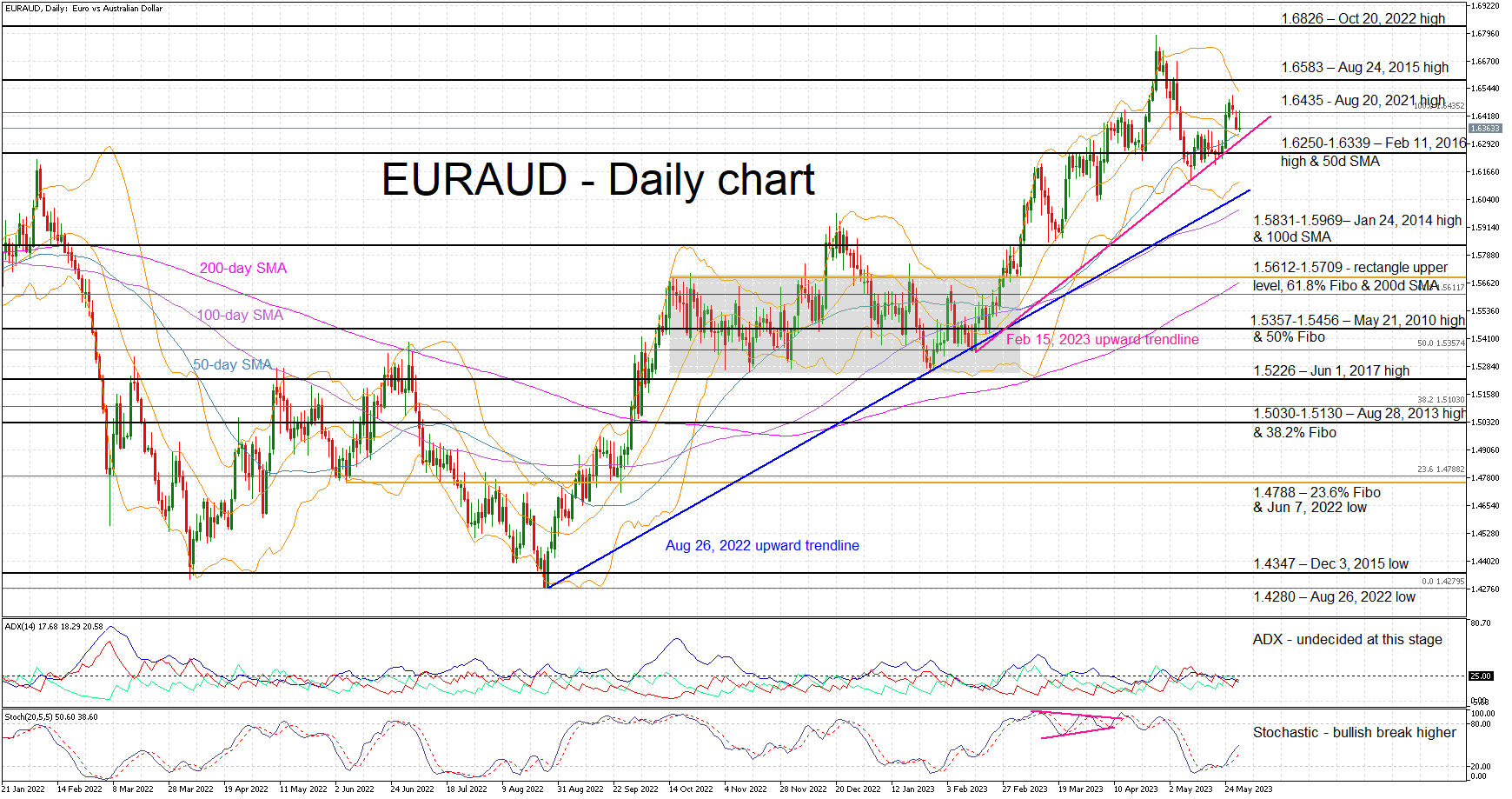

Euro/aussie experiencing bullish pressureThe aussie has been on the back foot since August 2022, underperforming the euro by around 15%. Recently, it has been trying to recover part of these losses, especially following the recent streak of weak euro area data. However, any attempt for a significant correction at the euro/aussie pair has halted at the February 15, 2023 upward sloping trendline. In addition, with the stochastic edging almost vertically higher, the onus is on aussie bulls to stop this pair from recording higher highs.

A positive set of data this week, and particularly an upside inflation surprise, would help the aussie bulls retest and potentially break the aforementioned trendline and the busy 1.6250-1.6339 area. On the other hand, weak data figures, which would essentially negate any change for a surprise rate hike at the next week’s meeting, would open the door for a break of the 1.6583 level and a retest of the October 20, 2022 high at 1.6826.

Gerelateerde activa

Laatste nieuws

Disclaimer: De entiteiten van de XM Group bieden diensten en toegang tot ons online handelsplatform op basis van uitsluitend-uitvoering, waardoor een persoon de beschikbare content op of via de website kan bekijken en/of gebruiken, zonder dat dit is bedoeld voor wijziging of uitbreiding. Dergelijk(e) toegang en gebruik vallen onder: (i) de algemene voorwaarden; (ii) risicowaarschuwingen; en de (iii) volledige disclaimer. Dergelijke content wordt daarom alleen aangeboden als algemene informatie. Wees u er daarnaast vooral van bewust dat de inhoud op ons online handelsplatform geen verzoek of aanbieding omvat om transacties op de financiële markten uit te voeren. Het beleggen op welke financiële markt dan ook vormt een aanzienlijk risico voor uw vermogen.

Alle materialen die op ons online handelsplatform worden gepubliceerd zijn bedoeld voor educatieve/informatieve doeleinden en omvatten geen – en moeten niet worden beschouwd als het bevatten van – financieel, vermogensbelastings- of handelsadvies en aanbevelingen, of een overzicht van onze handelsprijzen, of een aanbod of aanvraag van een transactie in financiële instrumenten of ongevraagde financiële promoties voor u.

Alle content van derden, alsmede content die is voorbereid door XM, zoals opinies, nieuws, onderzoeken, analyses, prijzen en andere informatie of koppelingen naar externe websites op deze website worden aangeboden op een 'zoals-ze-zijn'-basis, als algemene marktcommentaren, en vormen geen beleggingsadvies. Voor zover dat content wordt beschouwd als beleggingsonderzoek, moet u zich ervan bewust zijn en accepteren dat de content niet bedoeld was en niet is voorbereid in overeenstemming met de wettelijke vereisten die zijn opgesteld om de onafhankelijkheid van beleggingsonderzoek te bevorderen en als zodanig onder de geldende wetgeving en richtlijnen moet worden beschouwd als marketingcommunicatie. Zorg ervoor dat u onze Mededeling over niet-onafhankelijk beleggingsonderzoek en risicowaarschuwing in verband met de voorgaande informatie doorneemt en begrijpt; die kunt u hier lezen.