Market Comment – Dollar at 10-month high as yields keep surging

US 10-year yield hits 16-year high amid no letup in hawkish Fed rhetoric

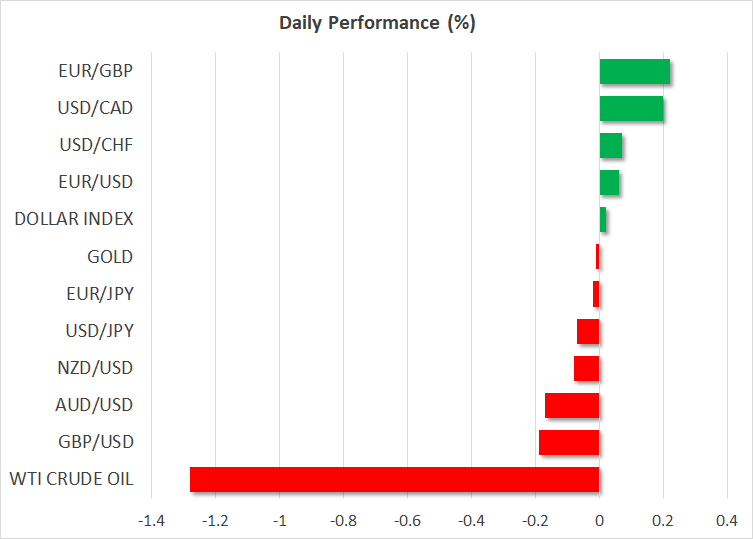

Dollar powers ahead, euro and pound crumble, yen in danger zone

Stocks resume decline after late rebound on Wall Street

Bond market rout deepens

Bond market rout deepensThe selloff in bond markets is showing no sign of easing as investors are dumping government securities in favour of cash amid expectations that interest rates in the US may yet rise further. Despite the tightening cycle nearing its end, the hawkish drumbeat from the Fed has only gotten louder, unnerving investors who were betting on rate cuts as early as in the spring of 2024.

The yield on 10-year Treasury notes broke above 4.50% on Monday for the first time since November 2007 and continues to climb to fresh highs today. The 30-year yield, meanwhile, has surged to 12½-year highs as long-term rates adjust to the Fed’s “higher for longer” mantra.

Minneapolis Fed President Neel Kashkari hinted on Monday that “rates probably have to go a little bit higher” if the US economy stays fundamentally resilient, while Chicago Fed chief Austan Goolsbee reiterated that rates will have to stay high for longer than what markers had anticipated.

The odds of one final 25-basis-point hike now stand at 50%, up from 40% prior to last week’s FOMC decision. However, there’s been no notable scaling back of rate cut expectations over the past week, suggesting that there’s room for further repricing should inflation remain stubbornly high.

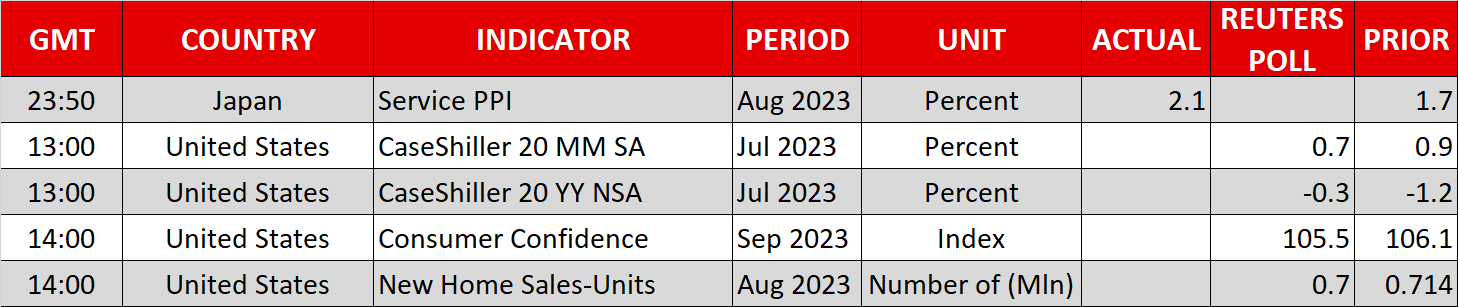

There’s no stopping the dollarThe next update on the inflation front will be Friday’s core PCE price index, which had edged up in July. If the Fed’s favourite price gauge falls to 3.9% in August as forecast, the rally in bond yields might pause for breath, halting the US dollar’s advance.

In the meantime, though, there’s no stopping the greenback as the dollar index is back above 106.0, reaching the highest since late November. What’s striking is that long-term bond yields have jumped across the board, with the exception of UK gilt yields, yet only the dollar stands tall.

The worsening economic data in Europe, China’s never-ending property crisis and the surprise rally in oil prices has dampened the prospects for most other major currencies. Even if the likes of the ECB and Bank of England are not about to cut rates anytime soon, the US economic outlook is far stronger at the moment. Moreover, a gloomy picture globally tends to draw safe haven bids for the dollar, thus there could be more gains in store in the near-to-medium term.

This can only be bad news for the euro and pound, which have slipped below the key levels of $1.06 and $1.22, respectively, over the past day.

Yen dangerously close to intervention levelThe yen is also under increasing strain as the Bank of Japan has set the bar high for warranting an exit from ultra-accommodative policy. There had been some hopes that the BoJ would soon begin laying the groundwork for an eventual exit but Governor Ueda’s dovish remarks in recent days suggest the timing remains a long way off.

That has left the yen extremely vulnerable in a landscape where there is renewed dollar upside. The greenback briefly spiked above 149 yen earlier today before easing back. The last time the yen approached the 150 level a year ago, Japanese officials had stepped up their verbal warnings before going ahead and intervening in the FX market to shore up the currency. But verbal intervention has been unusually scarce this time around, which may be an indication that the threshold has shifted somewhat.

Stocks continue to struggle despite Wall Street bounceHigher yields are weighing on European and Asian equities for a second day. Adding to the risk-off mood is news that China’s property giant, Evergrande, missed a bond payment, and a warning by ratings agency Moody’s that it may downgrade its rating on US debt if there is a government shutdown.

A credit downgrade could exacerbate the selloff in US Treasuries, which, apart from Fed tightening, are under pressure from the massive issuance in new debt.

Nevertheless, US stocks managed to stage a late rebound on Monday, with the S&P 500 adding 0.4% and the Nasdaq Composite gaining 0.5%.

The bounce back came about after Amazon said it will invest $4 billion in an AI startup, reviving the AI mania. Wall Street futures are in the red today, but a small relief rally is possible as Senate Republicans and Democrats are close to agreeing on a deal on a temporary spending measure to extend funding to the US government for six weeks. Although there’s a risk that the bill might not get through the House, it does represent a step in the right direction.

관련 자산

최신 뉴스

면책조항: XM Group 회사는 체결 전용 서비스와 온라인 거래 플랫폼에 대한 접근을 제공하여, 개인이 웹사이트에서 또는 웹사이트를 통해 이용 가능한 콘텐츠를 보거나 사용할 수 있도록 허용합니다. 이에 대해 변경하거나 확장할 의도는 없습니다. 이러한 접근 및 사용에는 다음 사항이 항상 적용됩니다: (i) 이용 약관, (ii) 위험 경고, (iii) 완전 면책조항. 따라서, 이러한 콘텐츠는 일반적인 정보에 불과합니다. 특히, 온라인 거래 플랫폼의 콘텐츠는 금융 시장에서의 거래에 대한 권유나 제안이 아닙니다. 금융 시장에서의 거래는 자본에 상당한 위험을 수반합니다.

온라인 거래 플랫폼에 공개된 모든 자료는 교육/정보 목적으로만 제공되며, 금융, 투자세 또는 거래 조언 및 권고, 거래 가격 기록, 금융 상품 또는 원치 않는 금융 프로모션의 거래 제안 또는 권유를 포함하지 않으며, 포함해서도 안됩니다.

이 웹사이트에 포함된 모든 의견, 뉴스, 리서치, 분석, 가격, 기타 정보 또는 제3자 사이트에 대한 링크와 같이 XM이 준비하는 콘텐츠 뿐만 아니라, 제3자 콘텐츠는 일반 시장 논평으로서 "현재" 기준으로 제공되며, 투자 조언으로 여겨지지 않습니다. 모든 콘텐츠가 투자 리서치로 해석되는 경우, 투자 리서치의 독립성을 촉진하기 위해 고안된 법적 요건에 따라 콘텐츠가 의도되지 않았으며, 준비되지 않았다는 점을 인지하고 동의해야 합니다. 따라서, 관련 법률 및 규정에 따른 마케팅 커뮤니케이션이라고 간주됩니다. 여기에서 접근할 수 있는 앞서 언급한 정보에 대한 비독립 투자 리서치 및 위험 경고 알림을 읽고, 이해하시기 바랍니다.