Market Comment – Powell pushes back on March rate cut, BoE on tap

Fed’s Powell says March rate cut not the “base case”

Dollar gains, but Treasury yields slide

BoE to stand pat, focus to fall on guidance

Wall Street tumbles, awaits more earnings results

Dollar gains on less-dovish-than-expected Fed

Dollar gains on less-dovish-than-expected FedThe US dollar gained against all but two of its major counterparts yesterday, losing ground only against the yen and ending the day virtually unchanged against the franc. The main losers were the aussie and the loonie.

What added fuel to the greenback’s engines may have been the less-dovish-than-expected Fed yesterday. The Committee decided to keep interest rates untouched and dropped a longstanding reference to the possibility of further hikes. However, policymakers noted that it may not be appropriate to lower rates until they gain greater confidence that inflation is moving sustainably towards their 2% objective. At the press conference, Fed Chair Powell was more specific, noting that a March rate cut was not the Fed’s “base case.”

This prompted market participants to lower the probability of a rate reduction in March to around 35% from 50% ahead of the decision. Now, a 25bps cut is more than fully priced in for May. That said, the total amount of basis points worth of rate reductions by the end of the year was not affected much. The market still anticipates around 144bps cuts by December, which combined with the fact that there are still participants betting on a March cut suggests that there is room for further upside adjustment to the market’s implied path, and thereby room for further advances in the US dollar.

That upside adjustment and thereby further dollar strength may come on Friday if the US employment report comes in stronger than expected.

Yen stands tall, BoE takes the central bank torchThe dollar could have gained even more after the Fed if it wasn’t for the slide in Treasury yields ahead of the decision, perhaps as investors have already begun reducing their risk exposure by selling stocks and seeking shelter in bonds.

The rush in bonds may have been exacerbated by a 38% selloff in New York Community Bancorp shares after the lender cut its dividends and posted a surprise loss, reviving fears about the health of regional lenders. This allowed the yen to outperform its US counterpart, with dollar/yen briefly falling below 146.00, before rebounding somewhat on Powell’s remarks.

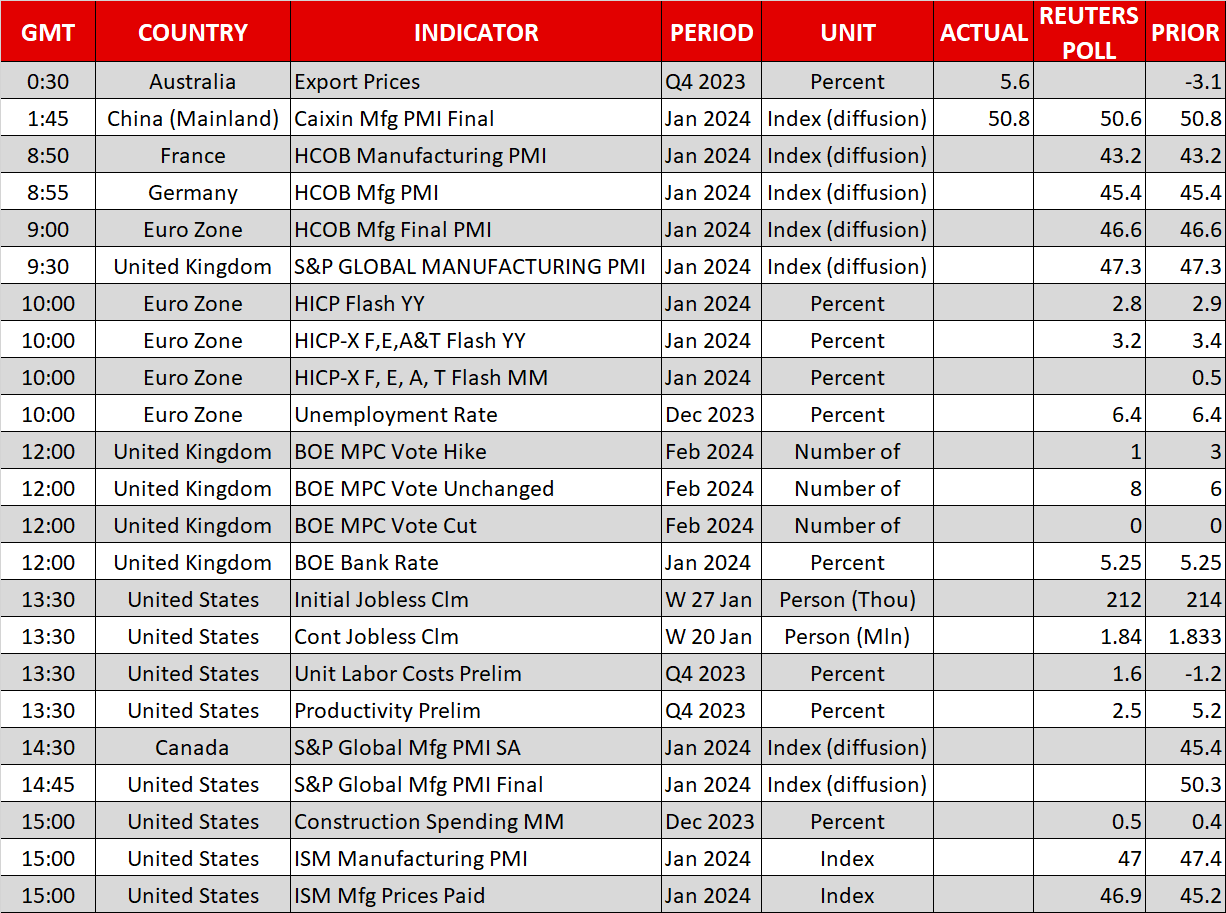

Recent UK data showed that inflation was hotter than expected in December, while the January PMIs pointed to improvement in business activity. Still, investors are penciling in around 107bps worth of rate reductions by the end of the year, with a first quarter-point cut anticipated in June.

As with the market’s implied Fed path, there is room for upside adjustment in the BoE’s path as well should UK officials continue to push back against rate cut speculation, and this might be the case today even if the latest rebound in inflation was the result of base effects. Despite sluggish economic growth in the UK, the improvement in the latest PMIs combined with still-elevated wage growth may allow policymakers to wait for a while longer before shifting to a more dovish stance.

Therefore, should the Bank reiterate the view that it is too early to examine rate reductions, this could help the pound gain some ground, especially if there are once again members opting for a rate increase.

In the Eurozone, the preliminary CPI data for January revealed that the bloc’s inflation slowed by less than expected. However, the euro did not react to the release as traders remained largely convinced that the ECB will deliver its first 25bps cut in April.

Equity traders await more ‘Magnificent 7’ resultsOn Wall Street, all three of its main indices closed in the red, with the Nasdaq falling more than 2%. Stocks were already falling ahead of the Fed decision, driven by mega-cap tech firms following the disappointing results by Alphabet. The Fed decision served as the icing on the cake. Today, equity investors will digest earnings results by Apple, Amazon and Meta, all of which report after the closing bell.

Gold also pulled back after the Fed poured cold water on March rate cut expectations, but managed to close the day in the green as the early slide in Treasury yields helped the precious metal climb higher in advance.

Asset collegati

Ultime news

Disclaimer: le entità di XM Group forniscono servizi di sola esecuzione e accesso al nostro servizio di trading online, che permette all'individuo di visualizzare e/o utilizzare i contenuti disponibili sul sito o attraverso di esso; non ha il proposito di modificare o espandere le proprie funzioni, né le modifica o espande. L'accesso e l'utilizzo sono sempre soggetti a: (i) Termini e condizioni; (ii) Avvertenza sui rischi e (iii) Disclaimer completo. Tali contenuti sono perciò forniti a scopo puramente informativo. Nello specifico, ti preghiamo di considerare che i contenuti del nostro servizio di trading online non rappresentano un sollecito né un'offerta ad operare sui mercati finanziari. Il trading su qualsiasi mercato finanziario comporta un notevole livello di rischio per il tuo capitale.

Tutto il materiale pubblicato sul nostro servizio di trading online è unicamente a scopo educativo e informativo, e non contiene (e non dovrebbe essere considerato come contenente) consigli e raccomandazioni di carattere finanziario, di trading o fiscale, né informazioni riguardanti i nostri prezzi di trading, offerte o solleciti riguardanti transazioni che possano coinvolgere strumenti finanziari, oppure promozioni finanziarie da te non richieste.

Tutti i contenuti di terze parti, oltre ai contenuti offerti da XM, siano essi opinioni, news, ricerca, analisi, prezzi, altre informazioni o link a siti di terzi presenti su questo sito, sono forniti "così com'è", e vanno considerati come commenti generali sui mercati; per questo motivo, non possono essere visti come consigli di investimento. Dato che tutti i contenuti sono intesi come ricerche di investimento, devi considerare e accettare che non sono stati preparati né creati seguendo i requisiti normativi pensati per promuovere l'indipendenza delle ricerche di investimento; per questo motivo, questi contenuti devono essere considerati come comunicazioni di marketing in base alle leggi e normative vigenti. Assicurati di avere letto e compreso pienamente la nostra Notifica sulla ricerca di investimento non indipendente e la nostra Informativa sul rischio riguardante le informazioni sopra citate; tali documenti sono consultabili qui.