Daily Comment – Will the dollar or stocks smile after the non-farm payrolls print?

- Spotlight falls on the key US labour market data

- Non-farm payrolls to rise by 140k, but could surprise to the upside

- Dollar to enjoy a strong set of data, equities prefer weaker prints

- Euro suffering continues, while both gold and oil advance

Could the US labour market data produce a surprise?

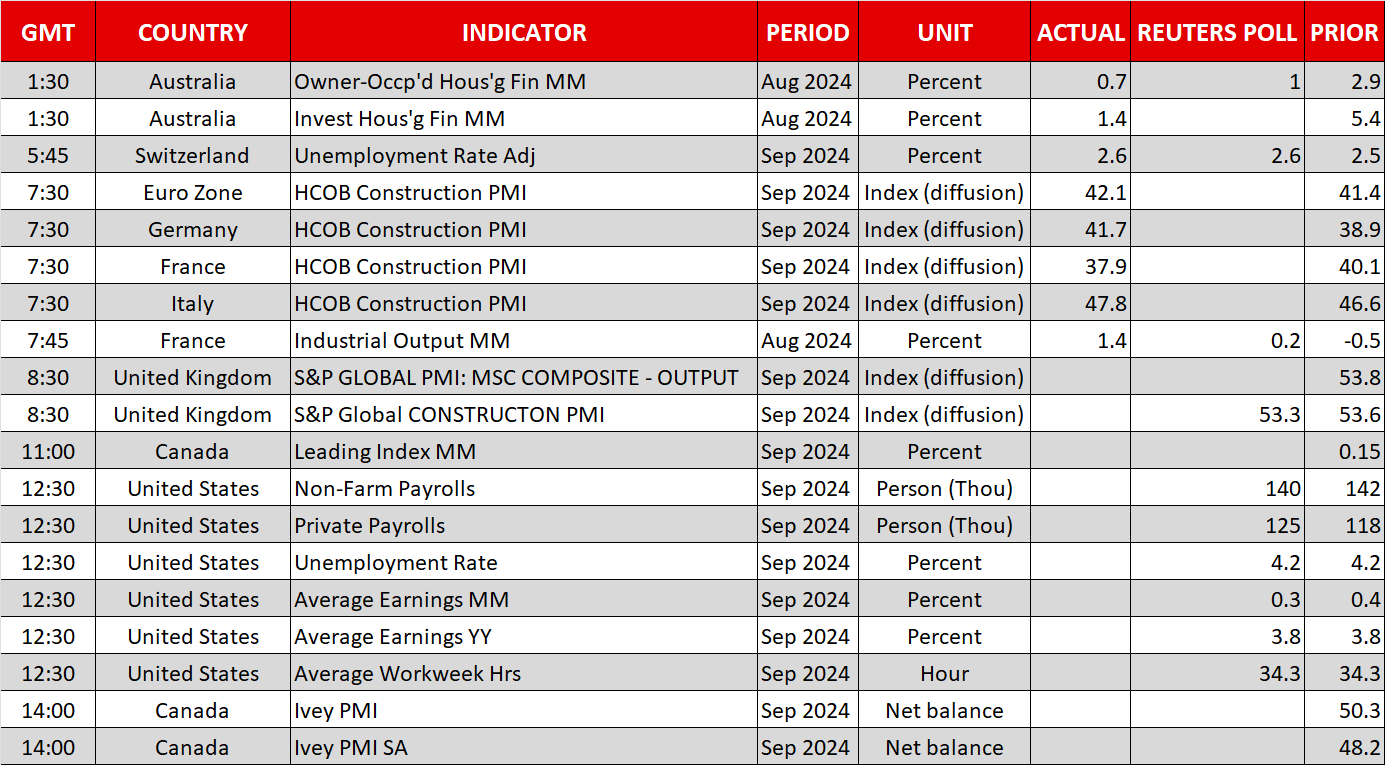

The countdown to the most crucial set of US data during October is nearly over. At 12.30 GMT the non-farm payrolls figure is expected to show a 140k increase, with forecasts ranging from 70k to 220k. Both the unemployment rate and the average hourly earnings growth will probably remain unchanged at 4.2% and 3.8%, respectively.

At 12.30 GMT the non-farm payrolls figure is expected to show an 140k increase

Up to now, data prints have been mixed, with the ISM manufacturing survey disappointing but both the weekly jobless claims and the ISM services survey raising the probability of an upside surprise today. A stronger set of prints later today, especially if the non-payrolls figure surpasses the 200k level, could force the most dovish Fed members to tone down their rhetoric for the November 7 meeting.

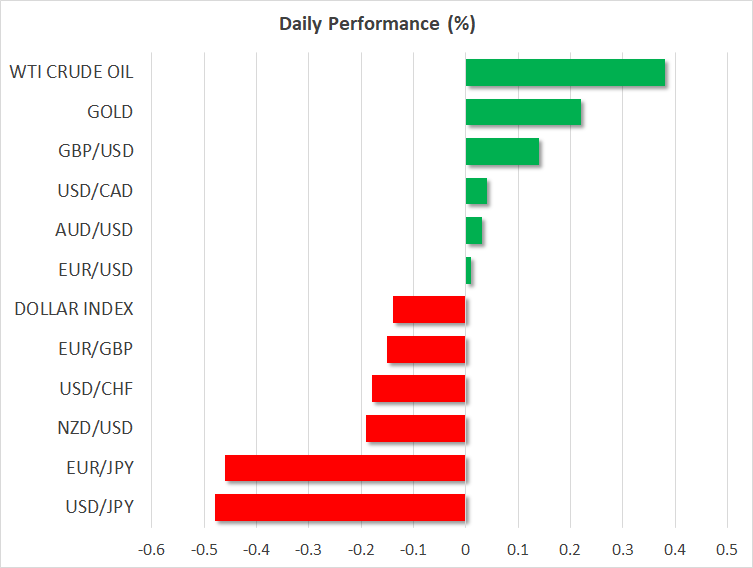

Such an outcome could really dent the current sizeable 35% probability for a 50bps rate move in November and further boost the US dollar. It has been a rather strong week for the greenback on the back of the reduced Fed rate cut expectations and the developments in the Middle East, with the dollar index being on course for its best week since mid-March.

Stock indices are not really sharing the dollar’s excitement, as they remain in negative territory on a weekly basis, led by the weakness seen in European stock markets. The risk-off reaction induced by Tuesday’s Iranian attack on Israel was further fueled yesterday after US president Biden’s comments that Israel has the green light to hit Iran’s oil installations.

Stock indices are not really sharing the dollar’s excitement, as they remain in negative territory on a weekly basis

Weak US data prints today, especially a sub-100k print in the non-payrolls figure and an abrupt increase in the unemployment rate, could temporarily reverse the current negative sentiment in equity markets. Interestingly, earnings announcements for the third quarter of 2024 will gradually take centre stage with the main US banking institutes publishing their results from October 11.

Euro remains on the back foot, pound tries to recover

The euro remains on the back foot, as the debate about the October ECB rate cut continues with most members appearing to be on board for such a move, despite the lack of staff projections and the fact that the meeting will take place far from the Frankfurt headquarters. There is a plethora of ECB speakers again today, but the message is unlikely to diverge much from the recent rhetoric.

The pound was the negative surprise of Thursday’s session, as Governor Bailey’s comments about a more aggressive stance in cutting rates came out of the blue and prompted a quick sell off. While the November rate cut is probably a done deal, the UK data releases point to another 25bps rate move. Maybe the BoE believes that the planned fiscal adjustment by the new government and a more dovish Fed warrant more aggressive easing.

Oil and gold are rising

With a barrage of attacks carried out by both Israel and Iran’s proxies on a daily basis, and the chances of a ceasefire remaining quite low at this stage, the current oil upleg could continue. WTI oil futures are hovering at a one-month high, quickly recovering from a 16-month low.

On the flip side, gold remains a tad below its recent all-time high, benefiting from equities’ weakness and undaunted by the dollar’s strength. The sell-off in bitcoin, and the remaining cryptocurrencies, could also support the current gold pricing as more traditional investors are not yet convinced of bitcoin’s ability to act as a safe haven asset in crisis periods.

Gold remains a tad below its recent all-time high, benefiting from the equities’ weakness and undaunted by the dollar’s strength

Asset collegati

Ultime news

Disclaimer: le entità di XM Group forniscono servizi di sola esecuzione e accesso al nostro servizio di trading online, che permette all'individuo di visualizzare e/o utilizzare i contenuti disponibili sul sito o attraverso di esso; non ha il proposito di modificare o espandere le proprie funzioni, né le modifica o espande. L'accesso e l'utilizzo sono sempre soggetti a: (i) Termini e condizioni; (ii) Avvertenza sui rischi e (iii) Disclaimer completo. Tali contenuti sono perciò forniti a scopo puramente informativo. Nello specifico, ti preghiamo di considerare che i contenuti del nostro servizio di trading online non rappresentano un sollecito né un'offerta ad operare sui mercati finanziari. Il trading su qualsiasi mercato finanziario comporta un notevole livello di rischio per il tuo capitale.

Tutto il materiale pubblicato sul nostro servizio di trading online è unicamente a scopo educativo e informativo, e non contiene (e non dovrebbe essere considerato come contenente) consigli e raccomandazioni di carattere finanziario, di trading o fiscale, né informazioni riguardanti i nostri prezzi di trading, offerte o solleciti riguardanti transazioni che possano coinvolgere strumenti finanziari, oppure promozioni finanziarie da te non richieste.

Tutti i contenuti di terze parti, oltre ai contenuti offerti da XM, siano essi opinioni, news, ricerca, analisi, prezzi, altre informazioni o link a siti di terzi presenti su questo sito, sono forniti "così com'è", e vanno considerati come commenti generali sui mercati; per questo motivo, non possono essere visti come consigli di investimento. Dato che tutti i contenuti sono intesi come ricerche di investimento, devi considerare e accettare che non sono stati preparati né creati seguendo i requisiti normativi pensati per promuovere l'indipendenza delle ricerche di investimento; per questo motivo, questi contenuti devono essere considerati come comunicazioni di marketing in base alle leggi e normative vigenti. Assicurati di avere letto e compreso pienamente la nostra Notifica sulla ricerca di investimento non indipendente e la nostra Informativa sul rischio riguardante le informazioni sopra citate; tali documenti sono consultabili qui.