Daily Comment – Tensions remain high in equities

- Strong US data is not welcomed by equities

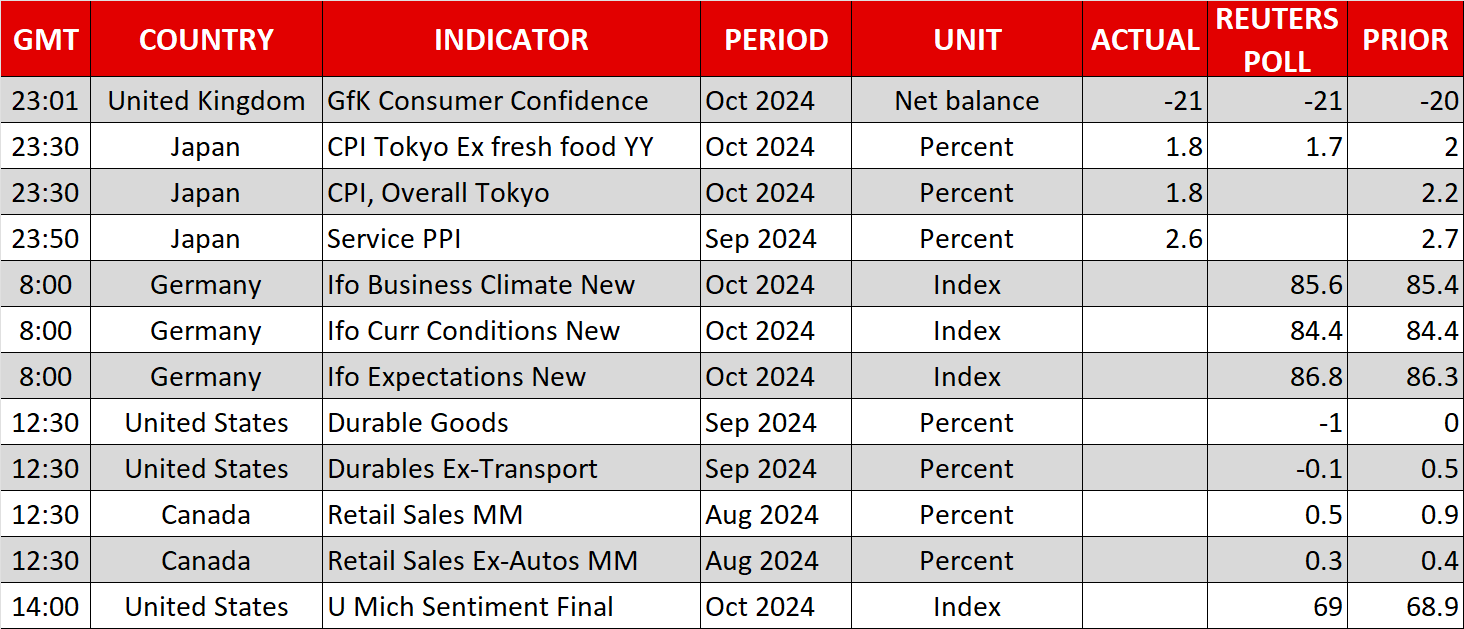

- Busy calendar today but markets are already focusing on next week

- Japan holds election on Sunday; the outcome could surprise

- BoJ and yen could suffer from a hung parliament

Data reconfirm the strength of the US economy

Yesterday’s PMI surveys release was a stark reminder that the US presidential election is not the sole market-moving factor. The next Fed meeting will be held two days after the election date and, assuming an eventless election process occurs, Chairman Powell et al will evaluate the progress made since the September aggressive rate cut.

The message from yesterday’s preliminary PMI surveys, the jobless claims figures and the new home sales data was that the US economy is still growing at a respectable rate, far above the growth achieved by most developed countries. The Fed hawks are not 100% on board for another rate cut, but the market will have to wait for November 7 for further comments on monetary policy, as Fedspeak will gradually diminish due to the usual blackout period that occurs before FOMC meetings, commencing shortly. The market, though, remains confident that a 25bps rate cut will be announced in a fortnight.

The message from yesterday’s preliminary PMI surveys was that the US economy is still growing at a respectable rate

Today’s durable goods report could prove the main event of the session, ahead of next week’s very busy calendar. The combination of the October jobs report and the first release of the third quarter GDP has the potential to further increase divisions in the Fed ranks and dent the US dollar’s recent strength.

Data releases confuse equity investors

In the meantime, US equity indices are caught up in the middle. Investors are trying to navigate through this pre-election period, as the rhetoric is gradually becoming more aggressive, US economic data is producing further surprises, and third quarter earnings are picking up speed.

US indices remain in the red this week, with the Dow Jones index suffering from yesterday’s weak earnings result from IBM. The Nasdaq 100 index is doing slightly better but that might change dramatically if next week’s barrage of earnings from Alphabet, Microsoft, Meta and Amazon fail to appease investors.

The Nasdaq 100 index is doing slightly better but that might change dramatically if next week’s barrage of earnings fail to appease investors.

Japanese elections on October 27

Following a weak set of inflation figures from Tokyo, which are usually a very strong predictor of national CPI, the market is preparing for Sunday’s general election in Japan. The LDP party is expected to earn the highest number of votes, but the latest polls increase the possibility of the LDP failing to achieve the necessary majority in the lower house, even with the help of its junior partner. In that case, the leading party would have to look elsewhere for the necessary support to form a new coalition, making generous compromises.

In the meantime, the yen remains under pressure, having quickly lost almost 60% of its July-September outperformance against the dollar. The BoJ is meeting next week, but the market has turned its focus to the December gathering. Political uncertainty along with weaker data prints could potentially force Governor Ueda et al to postpone any December decisions and thus remove the strongest tailwind for the yen.

Political uncertainty along with weaker data prints could potentially force Governor Ueda et al to postpone any December decisions

Actifs liés

Dernières actualités

Avertissement : Les entités de XM Group proposent à notre plateforme de trading en ligne un service d'exécution uniquement, autorisant une personne à consulter et/ou à utiliser le contenu disponible sur ou via le site internet, qui n'a pas pour but de modifier ou d'élargir cette situation. De tels accès et utilisation sont toujours soumis aux : (i) Conditions générales ; (ii) Avertissements sur les risques et (iii) Avertissement complet. Un tel contenu n'est par conséquent fourni que pour information générale. En particulier, sachez que les contenus de notre plateforme de trading en ligne ne sont ni une sollicitation ni une offre de participation à toute transaction sur les marchés financiers. Le trading sur les marchés financiers implique un niveau significatif de risques pour votre capital.

Tout le matériel publié dans notre Centre de trading en ligne est destiné à des fins de formation / d'information uniquement et ne contient pas – et ne doit pas être considéré comme contenant – des conseils et recommandations en matière de finance, de fiscalité des investissements ou de trading, ou un enregistrement de nos prix de trading ou une offre, une sollicitation, une transaction à propos de tout instrument financier ou bien des promotions financières non sollicitées à votre égard.

Tout contenu tiers, de même que le contenu préparé par XM, tels que les opinions, actualités, études, analyses, prix, autres informations ou liens vers des sites tiers contenus sur ce site internet sont fournis "tels quels", comme commentaires généraux sur le marché et ne constituent pas des conseils en investissement. Dans la mesure où tout contenu est considéré comme de la recherche en investissement, vous devez noter et accepter que le contenu n'a pas été conçu ni préparé conformément aux exigences légales visant à promouvoir l'indépendance de la recherche en investissement et, en tant que tel, il serait considéré comme une communication marketing selon les lois et réglementations applicables. Veuillez vous assurer que vous avez lu et compris notre Avis sur la recherche en investissement non indépendante et notre avertissement sur les risques concernant les informations susdites, qui peuvent consultés ici.