Turkish lira falls apart, what can turn the tide?

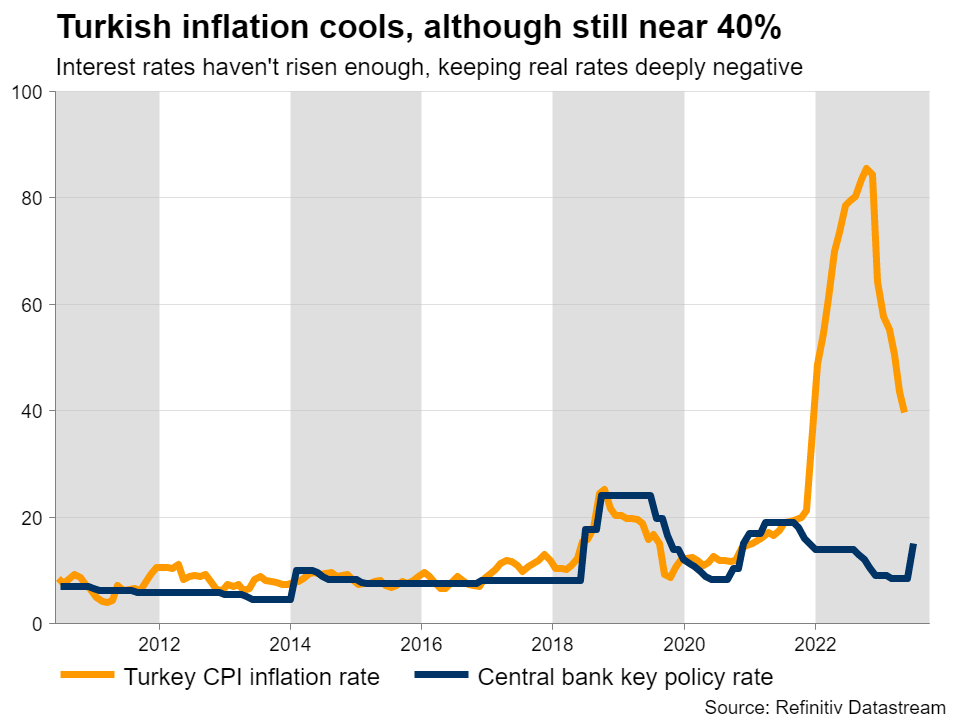

That’s only half the story, though. Another element that ravaged the lira was the central bank’s latest decision on interest rates. With a new governor coming in, there was rampant speculation about a massive increase in rates to fight runaway inflation. Some economists expected rates to be raised immediately to 25%, so when the central bank only lifted them to 15%, investors saw that as a huge disappointment. With inflation running around 40%, this move was seen as a ‘half measure’ that won’t be sufficient in cooling the economy down. Behind the downtrendTaking a step back, the lira’s downtrend is not a new phenomenon. The currency has been in decline for more than two decades, although the losses accelerated sharply after 2018 as inflation started to fire up and the nation’s deficits blew up. When inflation moves far higher but interest rates don’t follow suit, the result is that real interest rates fall deep into negative territory. That’s toxic for the lira because it discourages investors and consumers from holding it. Nobody wants to keep a currency that is constantly losing its value, if they are not compensated through high interest rates.

That’s only half the story, though. Another element that ravaged the lira was the central bank’s latest decision on interest rates. With a new governor coming in, there was rampant speculation about a massive increase in rates to fight runaway inflation. Some economists expected rates to be raised immediately to 25%, so when the central bank only lifted them to 15%, investors saw that as a huge disappointment. With inflation running around 40%, this move was seen as a ‘half measure’ that won’t be sufficient in cooling the economy down. Behind the downtrendTaking a step back, the lira’s downtrend is not a new phenomenon. The currency has been in decline for more than two decades, although the losses accelerated sharply after 2018 as inflation started to fire up and the nation’s deficits blew up. When inflation moves far higher but interest rates don’t follow suit, the result is that real interest rates fall deep into negative territory. That’s toxic for the lira because it discourages investors and consumers from holding it. Nobody wants to keep a currency that is constantly losing its value, if they are not compensated through high interest rates.  Many have attributed the central bank’s reluctance to raise rates to political pressure from President Erdogan, who has characterized high interest rates as “the mother and father of all evil”. The fact the central bank has changed its Governor four times over the last five years is a testament to this political arm-twisting, as Erdogan simply replaced any leaders that dared to raise rates much. Therefore, it can be argued the central bank has effectively lost its independence, leaving it unable to take the actions necessary to extinguish inflation. Even the new governor - who has a background as a Wall Street banker - could not break this spell. Making matters worse for the lira, Turkey runs a chronic current account deficit, which has swelled in recent years. That means the nation is a net-borrower, importing more than it exports and relying on capital flows from abroad to finance the difference. Over time, these deficits can exert massive downward pressure on a currency, especially if they keep widening.

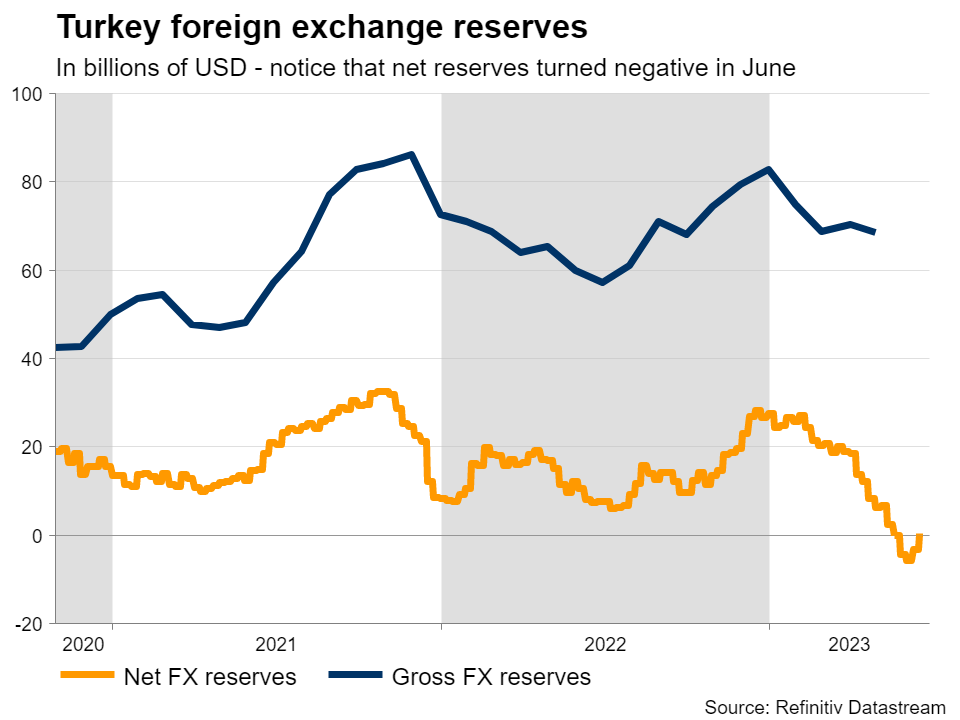

Many have attributed the central bank’s reluctance to raise rates to political pressure from President Erdogan, who has characterized high interest rates as “the mother and father of all evil”. The fact the central bank has changed its Governor four times over the last five years is a testament to this political arm-twisting, as Erdogan simply replaced any leaders that dared to raise rates much. Therefore, it can be argued the central bank has effectively lost its independence, leaving it unable to take the actions necessary to extinguish inflation. Even the new governor - who has a background as a Wall Street banker - could not break this spell. Making matters worse for the lira, Turkey runs a chronic current account deficit, which has swelled in recent years. That means the nation is a net-borrower, importing more than it exports and relying on capital flows from abroad to finance the difference. Over time, these deficits can exert massive downward pressure on a currency, especially if they keep widening.  The government has tried all sorts of unconventional tactics to stop the lira’s bleeding, such as making it more difficult to short the currency, introducing special savings accounts that compensate consumers if the lira falls sharply, and de facto confiscating foreign currencies from private banks to boost its FX reserves. These moves helped slow down the pace of depreciation for some time, alongside regular FX interventions, albeit at the cost of draining reserves. What’s next Looking ahead, there isn’t much that can turn the tides in the lira. What the currency desperately needs are higher interest rates, to slow down nominal growth and eradicate inflationary pressures, a painful process that will most likely involve a recession. Yet, President Erdogan seems determined not to let that happen. Slashing government spending could help to lower inflation, although this strategy might still be bearish for the lira initially, given its negative implications for economic growth. Plus, fiscal austerity would be a wildly unpopular move politically, making it seem even less likely.

The government has tried all sorts of unconventional tactics to stop the lira’s bleeding, such as making it more difficult to short the currency, introducing special savings accounts that compensate consumers if the lira falls sharply, and de facto confiscating foreign currencies from private banks to boost its FX reserves. These moves helped slow down the pace of depreciation for some time, alongside regular FX interventions, albeit at the cost of draining reserves. What’s next Looking ahead, there isn’t much that can turn the tides in the lira. What the currency desperately needs are higher interest rates, to slow down nominal growth and eradicate inflationary pressures, a painful process that will most likely involve a recession. Yet, President Erdogan seems determined not to let that happen. Slashing government spending could help to lower inflation, although this strategy might still be bearish for the lira initially, given its negative implications for economic growth. Plus, fiscal austerity would be a wildly unpopular move politically, making it seem even less likely.  That leaves structural reforms and regulatory changes, but admittedly, it’s highly doubtful any such policies would be powerful enough to rescue the currency. If there were easy solutions from a legislative perspective, they would have been implemented already. As such, it’s difficult to see a path towards a sustainable FX recovery, at least under the current political leadership. While a near-term correction seems plausible after such a dramatic downfall, it is unlikely to go very far, with real rates so deep in negative territory and FX reserves exhausted.

That leaves structural reforms and regulatory changes, but admittedly, it’s highly doubtful any such policies would be powerful enough to rescue the currency. If there were easy solutions from a legislative perspective, they would have been implemented already. As such, it’s difficult to see a path towards a sustainable FX recovery, at least under the current political leadership. While a near-term correction seems plausible after such a dramatic downfall, it is unlikely to go very far, with real rates so deep in negative territory and FX reserves exhausted. Activos relacionados

Últimas noticias

Descargo de responsabilidades: Cada una de las entidades de XM Group proporciona un servicio de solo ejecución y acceso a nuestra plataforma de trading online, permitiendo a una persona ver o usar el contenido disponible en o a través del sitio web, sin intención de cambiarlo ni ampliarlo. Dicho acceso y uso están sujetos en todo momento a: (i) Términos y Condiciones; (ii) Advertencias de riesgo; y (iii) Descargo completo de responsabilidades. Por lo tanto, dicho contenido se proporciona exclusivamente como información general. En particular, por favor tenga en cuenta que, los contenidos de nuestra plataforma de trading online no son ni solicitud ni una oferta para entrar a realizar transacciones en los mercados financieros. Operar en cualquier mercado financiero implica un nivel de riesgo significativo para su capital.

Todo el material publicado en nuestra plataforma de trading online tiene únicamente fines educativos/informativos y no contiene –y no debe considerarse que contenga– asesoramiento ni recomendaciones financieras, tributarias o de inversión, ni un registro de nuestros precios de trading, ni una oferta ni solicitud de transacción con instrumentos financieros ni promociones financieras no solicitadas.

Cualquier contenido de terceros, así como el contenido preparado por XM, como por ejemplo opiniones, noticias, investigaciones, análisis, precios, otras informaciones o enlaces a sitios de terceros que figuran en este sitio web se proporcionan “tal cual”, como comentarios generales del mercado y no constituyen un asesoramiento en materia de inversión. En la medida en que cualquier contenido se interprete como investigación de inversión, usted debe tener en cuenta y aceptar que dicho contenido no fue concebido ni elaborado de acuerdo con los requisitos legales diseñados para promover la independencia en materia de investigación de inversiones y, por tanto, se considera como una comunicación comercial en virtud de las leyes y regulaciones pertinentes. Por favor, asegúrese de haber leído y comprendido nuestro Aviso sobre investigación de inversión no independiente y advertencia de riesgo en relación con la información anterior, al que se puede acceder aquí.