Daily Comment – Will the dollar or stocks smile after the non-farm payrolls print?

- Spotlight falls on the key US labour market data

- Non-farm payrolls to rise by 140k, but could surprise to the upside

- Dollar to enjoy a strong set of data, equities prefer weaker prints

- Euro suffering continues, while both gold and oil advance

Could the US labour market data produce a surprise?

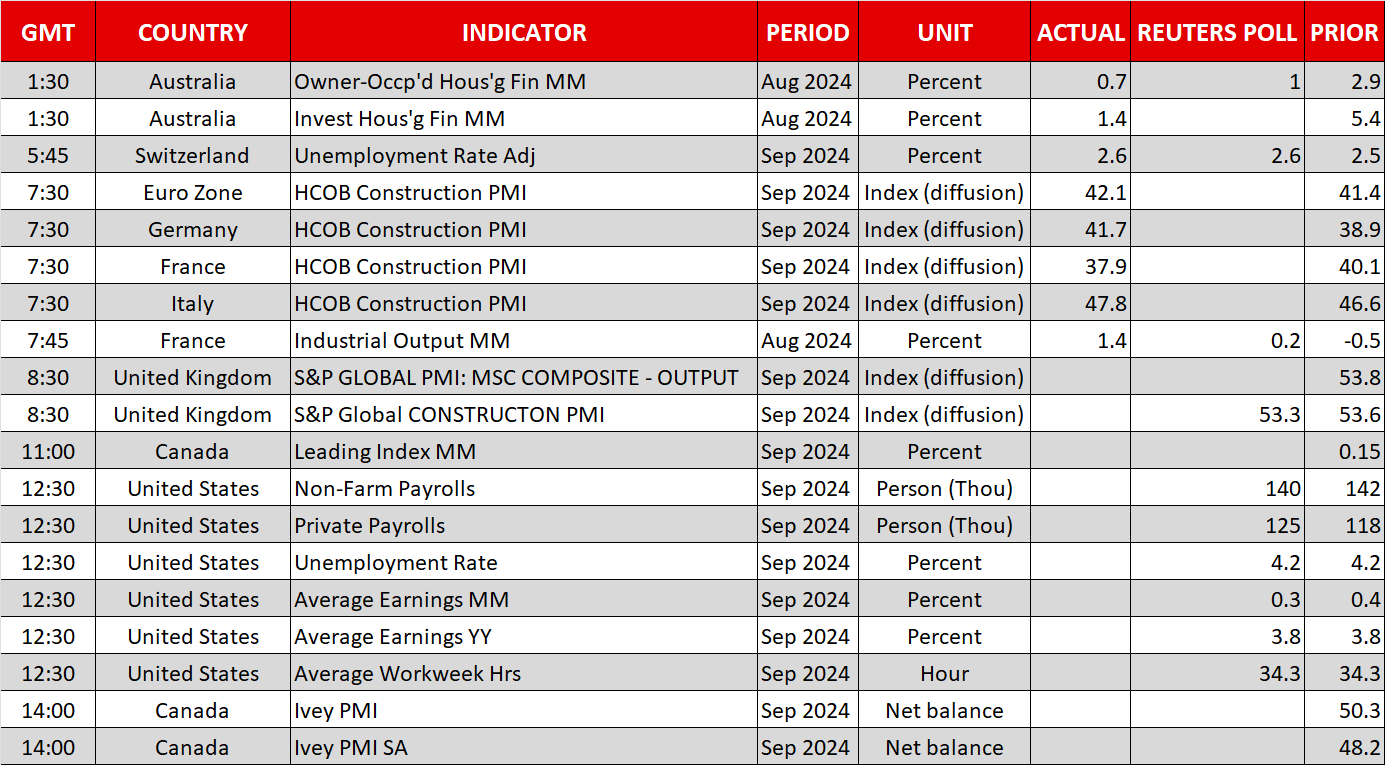

The countdown to the most crucial set of US data during October is nearly over. At 12.30 GMT the non-farm payrolls figure is expected to show a 140k increase, with forecasts ranging from 70k to 220k. Both the unemployment rate and the average hourly earnings growth will probably remain unchanged at 4.2% and 3.8%, respectively.

At 12.30 GMT the non-farm payrolls figure is expected to show an 140k increase

Up to now, data prints have been mixed, with the ISM manufacturing survey disappointing but both the weekly jobless claims and the ISM services survey raising the probability of an upside surprise today. A stronger set of prints later today, especially if the non-payrolls figure surpasses the 200k level, could force the most dovish Fed members to tone down their rhetoric for the November 7 meeting.

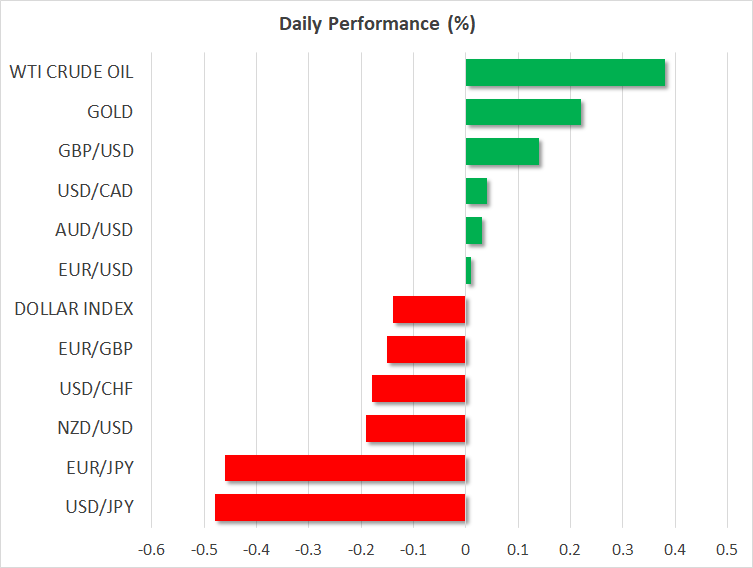

Such an outcome could really dent the current sizeable 35% probability for a 50bps rate move in November and further boost the US dollar. It has been a rather strong week for the greenback on the back of the reduced Fed rate cut expectations and the developments in the Middle East, with the dollar index being on course for its best week since mid-March.

Stock indices are not really sharing the dollar’s excitement, as they remain in negative territory on a weekly basis, led by the weakness seen in European stock markets. The risk-off reaction induced by Tuesday’s Iranian attack on Israel was further fueled yesterday after US president Biden’s comments that Israel has the green light to hit Iran’s oil installations.

Stock indices are not really sharing the dollar’s excitement, as they remain in negative territory on a weekly basis

Weak US data prints today, especially a sub-100k print in the non-payrolls figure and an abrupt increase in the unemployment rate, could temporarily reverse the current negative sentiment in equity markets. Interestingly, earnings announcements for the third quarter of 2024 will gradually take centre stage with the main US banking institutes publishing their results from October 11.

Euro remains on the back foot, pound tries to recover

The euro remains on the back foot, as the debate about the October ECB rate cut continues with most members appearing to be on board for such a move, despite the lack of staff projections and the fact that the meeting will take place far from the Frankfurt headquarters. There is a plethora of ECB speakers again today, but the message is unlikely to diverge much from the recent rhetoric.

The pound was the negative surprise of Thursday’s session, as Governor Bailey’s comments about a more aggressive stance in cutting rates came out of the blue and prompted a quick sell off. While the November rate cut is probably a done deal, the UK data releases point to another 25bps rate move. Maybe the BoE believes that the planned fiscal adjustment by the new government and a more dovish Fed warrant more aggressive easing.

Oil and gold are rising

With a barrage of attacks carried out by both Israel and Iran’s proxies on a daily basis, and the chances of a ceasefire remaining quite low at this stage, the current oil upleg could continue. WTI oil futures are hovering at a one-month high, quickly recovering from a 16-month low.

On the flip side, gold remains a tad below its recent all-time high, benefiting from equities’ weakness and undaunted by the dollar’s strength. The sell-off in bitcoin, and the remaining cryptocurrencies, could also support the current gold pricing as more traditional investors are not yet convinced of bitcoin’s ability to act as a safe haven asset in crisis periods.

Gold remains a tad below its recent all-time high, benefiting from the equities’ weakness and undaunted by the dollar’s strength

Activos relacionados

Últimas noticias

Descargo de responsabilidades: Cada una de las entidades de XM Group proporciona un servicio de solo ejecución y acceso a nuestra plataforma de trading online, permitiendo a una persona ver o usar el contenido disponible en o a través del sitio web, sin intención de cambiarlo ni ampliarlo. Dicho acceso y uso están sujetos en todo momento a: (i) Términos y Condiciones; (ii) Advertencias de riesgo; y (iii) Descargo completo de responsabilidades. Por lo tanto, dicho contenido se proporciona exclusivamente como información general. En particular, por favor tenga en cuenta que, los contenidos de nuestra plataforma de trading online no son ni solicitud ni una oferta para entrar a realizar transacciones en los mercados financieros. Operar en cualquier mercado financiero implica un nivel de riesgo significativo para su capital.

Todo el material publicado en nuestra plataforma de trading online tiene únicamente fines educativos/informativos y no contiene –y no debe considerarse que contenga– asesoramiento ni recomendaciones financieras, tributarias o de inversión, ni un registro de nuestros precios de trading, ni una oferta ni solicitud de transacción con instrumentos financieros ni promociones financieras no solicitadas.

Cualquier contenido de terceros, así como el contenido preparado por XM, como por ejemplo opiniones, noticias, investigaciones, análisis, precios, otras informaciones o enlaces a sitios de terceros que figuran en este sitio web se proporcionan “tal cual”, como comentarios generales del mercado y no constituyen un asesoramiento en materia de inversión. En la medida en que cualquier contenido se interprete como investigación de inversión, usted debe tener en cuenta y aceptar que dicho contenido no fue concebido ni elaborado de acuerdo con los requisitos legales diseñados para promover la independencia en materia de investigación de inversiones y, por tanto, se considera como una comunicación comercial en virtud de las leyes y regulaciones pertinentes. Por favor, asegúrese de haber leído y comprendido nuestro Aviso sobre investigación de inversión no independiente y advertencia de riesgo en relación con la información anterior, al que se puede acceder aquí.