British Pound: A silent power among the majors

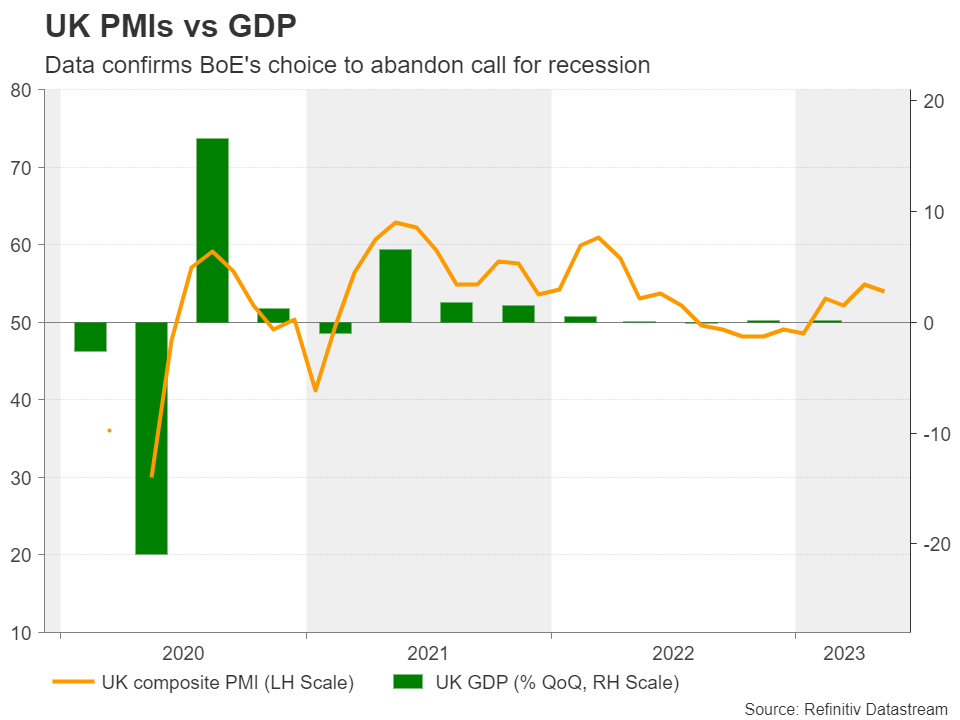

With the BoE abandoning its recession call and signaling that they will not hesitate to raise rates further should inflation pressures persist, market participants remained convinced that officials could deliver two more quarter-point increases by the end of the year.

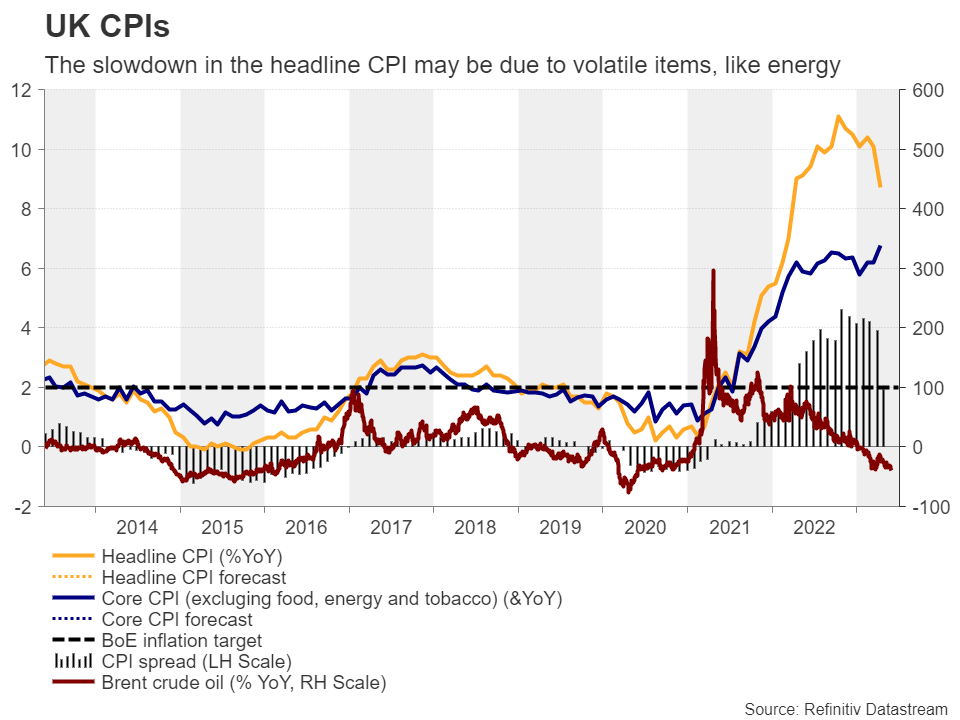

However, that was the case before May 24, the day when the inflation numbers for April were released. The data revealed that the headline CPI slowed by less than expected, to 8.7% year-on-year from 10.1%, but what was much more worrisome was the unexpected acceleration in underlying inflation to 6.8% y/y from 6.2%. This suggested that price pressures are becoming more embedded in the broader economy, and that the decline in the headline rate was just the result of a slowdown in the prices of volatile items like energy.

With no recession calls, investors double their BoE hike bets

With no recession calls, investors double their BoE hike betsWith that in mind, investors have doubled their bets, now almost 100bps worth of additional rate increments by December, with a first quarter-point cut being nearly fully priced in for May 2024. And all this even after preliminary PMIs for May disappointed last week. Perhaps investors are content with the fact that the composite index is still pointing to expansion, which enhances the view that the UK economy may have avoided a recession.

After November, when the BoE predicted the longest recession in the UK economy’s history, the financial community viewed the Bank’s slow and cautious tightening as a wise choice, but with all the economic engines performing better than feared then and inflation remaining out of control, market participants are now hoping for, or even demanding, more aggressive action by the Bank.

Will Bailey and co rise to the occasion?Bailey and his fellow policymakers may have no other choice than to signal that more tightening is needed. Although the PMIs came in weaker than expected, they revealed that output charges continued to rise, and although they eased to the slowest in three months, they remained elevated by the survey’s historical standards. What’s more, average weekly earnings accelerated in March, which means that consumer demand could stay strong in the months to come and thereby keep inflation elevated.

Consequently, a 25bps hike at the BoE’s upcoming gathering may not constitute an adequate reason for celebration. Pound traders may feel satisfied and willing to add to their long positions if the Bank appears willing to keep raising rates as forcefully as needed to tame the inflation beast.

The pound may benefit heading into the June meeting by the fact that investors are taking a leap of faith and trust that the BoE may continue raising interest rates more aggressively than any other major central bank, while the currency may strengthen even more if policymakers appear determined to do whatever it takes to bring inflation to heel.

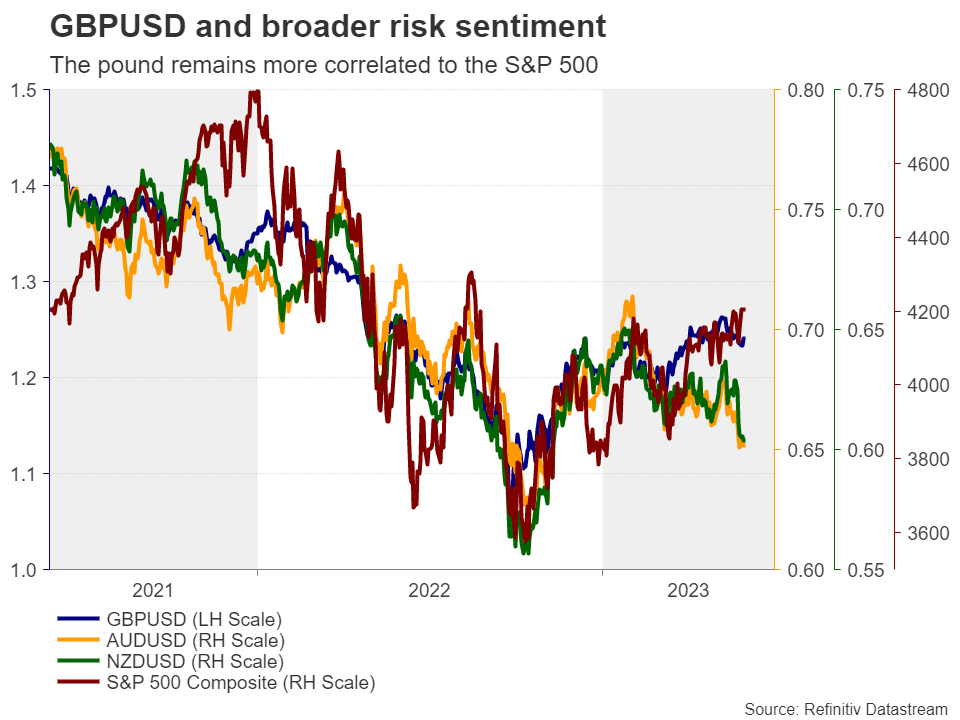

Pound remains the best performing major currency year-to-dateAlthough it pulled back against its US counterpart recently, the British currency remains the top performer among the majors since the beginning of the year, and monetary policy may have not been the only source of fuel. Due to the UK’s twin deficit, sterling has turned into a risk-linked currency the last few years, strengthening when equities rise and vice versa.

With Wall Street in an uptrend mode, it seems that the pound may have indeed benefited from investors’ willingness to keep increasing their risk exposure. But why didn’t the other traditional risk-linked currencies aussie and kiwi follow suit? Perhaps due to Chinese data suggesting that after the post-reopening boost, Australia’s and New Zealand’s main trading partner is losing momentum.

Currently, equity traders seem to be indifferent, or less interested, to Chinese data, preferring to ride the artificial intelligence (AI) trend as optimism and better forecasts of tech firms are probably on top of their lists.

Putting everything together, with the dollar staging a decent comeback lately due to the market reevaluating its implied Fed rate path, pound/dollar may not be the best choice for exploiting further gains in the pound, at least in the short run. The yen and the kiwi may be more appropriate candidates as the BoJ is sticking to its ultra-loose monetary policy and the RBNZ seems to be over with this tightening cycle.

Pound may continue to benefit the most against the kiwiHaving said that, choosing the yen carries more risks as the BoJ may eventually proceed with more normalizing steps, while an unexpected turbulent market episode will not only weigh on the pound, but also benefit the safe-haven yen. So, ultimately, the best option could be the pound/kiwi pair as the risk-on characteristics of both currencies are somewhat offsetting each other and thus, the probability of violent swings when sentiment changes may be smaller. Even if the sentiment-related forces are not equal, the current market landscape suggests that the pound has an advantage either way. It gains more in risk-on episodes and loses less in risk-off.

Indeed, since last Wednesday, when the RBNZ hinted that it is probably done raising interest rates, pound/kiwi has been in a fly mode, breaking above the high of April 26 just this Tuesday and signaling the continuation of the prevailing uptrend.

The pair now looks to be headed towards the 2.0700 territory, marked by the highs of May 2020, the break of which could carry extensions towards the 2.1000 zone, which acted as a ceiling between mid-March and mid-April of that same year.

For the outlook to turn bearish, the bears may have to drive the action all the way down and below the 1.9800 area, which offered strong support this month and coincided with the 38.2% Fibonacci retracement level of the February 3 – April 26 upleg.

Σχετιζόμενα σύμβολα

Τελευταία νέα

Δήλωση αποποίησης ευθύνης: Οι οντότητες του ομίλου XM Group παρέχουν υπηρεσίες σε βάση εκτέλεσης μόνο και η πρόσβαση στην ηλεκτρονική πλατφόρμα συναλλαγών μας που επιτρέπει στον ενδιαφερόμενο να δει ή/και να χρησιμοποιήσει το περιεχόμενο που είναι διαθέσιμο στην ιστοσελίδα μας ή μέσω αυτής, δε διαφοροποιεί ούτε επεκτείνει αυτές τις υπηρεσίες πέραν αυτού ούτε προορίζεται για κάτι τέτοιο. Η εν λόγω πρόσβαση και χρήση υπόκεινται σε: (i) Όρους και προϋποθέσεις, (ii) Προειδοποιήσεις κινδύνου και (iii) Πλήρη δήλωση αποποίησης ευθύνης. Ως εκ τούτου, το περιεχόμενο αυτό παρέχεται μόνο ως γενική πληροφόρηση. Λάβετε ιδιαιτέρως υπόψη σας ότι τα περιεχόμενα της ηλεκτρονικής πλατφόρμας συναλλαγών μας δεν αποτελούν παρότρυνση, ούτε προσφορά για να προβείτε σε οποιεσδήποτε συναλλαγές στις χρηματοπιστωτικές αγορές. Η πραγματοποίηση συναλλαγών στις χρηματοπιστωτικές αγορές ενέχει σημαντικό κίνδυνο για το κεφάλαιό σας.

Όλο το υλικό που δημοσιεύεται στην ηλεκτρονική πλατφόρμα συναλλαγών μας προορίζεται για εκπαιδευτικούς/ενημερωτικούς σκοπούς μόνο και δεν περιέχει, ούτε θα πρέπει να θεωρηθεί ότι περιέχει συμβουλές και συστάσεις χρηματοοικονομικές ή σε σχέση με φόρο επενδύσεων και την πραγματοποίηση συναλλαγών, ούτε αρχείο των τιμών διαπραγμάτευσής μας ούτε και προσφορά ή παρότρυνση για συναλλαγή οποιωνδήποτε χρηματοπιστωτικών μέσων ή ανεπιθύμητες προς εσάς προωθητικές ενέργειες.

Οποιοδήποτε περιεχόμενο τρίτων, καθώς και περιεχόμενο που εκπονείται από την ΧΜ, όπως απόψεις, ειδήσεις, έρευνα, αναλύσεις, τιμές, άλλες πληροφορίες ή σύνδεσμοι προς ιστότοπους τρίτων το οποίο περιέχεται σε αυτήν την ιστοσελίδα παρέχεται «ως έχει», ως γενικός σχολιασμός της αγοράς και δεν αποτελεί επενδυτική συμβουλή. Στον βαθμό που οποιοδήποτε περιεχόμενο ερμηνεύεται ως επενδυτική έρευνα, πρέπει να λάβετε υπόψη και να αποδεχτείτε ότι το περιεχόμενο δεν προοριζόταν και δεν έχει προετοιμαστεί σύμφωνα με τις νομικές απαιτήσεις που αποσκοπούν στην προώθηση της ανεξαρτησίας της επενδυτικής έρευνας και ως εκ τούτου, θα πρέπει να θεωρηθεί ως επικοινωνία μάρκετινγκ σύμφωνα με τους σχετικούς νόμους και κανονισμούς. Παρακαλούμε εξασφαλίστε ότι έχετε διαβάσει και κατανοήσει τη Γνωστοποίησή μας περί Μη ανεξάρτητης επενδυτικής έρευνας και την Προειδοποίηση κινδύνου όσον αφορά τις παραπάνω πληροφορίες, τις οποίες μπορείτε να βρείτε εδώ.